Introduction

Welcome to our guide on prime lending rates – an essential component of the financial world. Whether you’re a homeowner, business owner, or simply interested in the intricacies of the lending industry, understanding the prime lending rate is crucial. In this article, we will delve into the definition, determination, importance, effects, and pros and cons of the prime lending rate.

The prime lending rate serves as a benchmark interest rate utilized by financial institutions when granting loans to individuals and businesses. It directly affects the interest rates on various loans, including mortgages, personal loans, and business loans. The prime lending rate is generally set by financial institutions and is influenced by several external factors.

As a borrower, being well-informed about the prime lending rate empowers you to make informed decisions regarding your loans and financial obligations. Knowing how changes in the prime lending rate can impact your monthly repayments and overall borrowing costs can be advantageous when considering loan options.

In this comprehensive guide, we aim to demystify the world of prime lending rates by explaining how they are determined and their significance in the financial landscape. Additionally, we will discuss the potential effects of changes in the prime lending rate, as well as the advantages and disadvantages associated with loans tied to the prime lending rate.

By the end of this guide, you will have a solid understanding of the prime lending rate and its role in the lending industry. Armed with this knowledge, you can confidently navigate the borrowing process and make informed decisions about your loan options. So, let’s dive in and explore the intricacies of the prime lending rate!

Definition of Prime Lending Rate

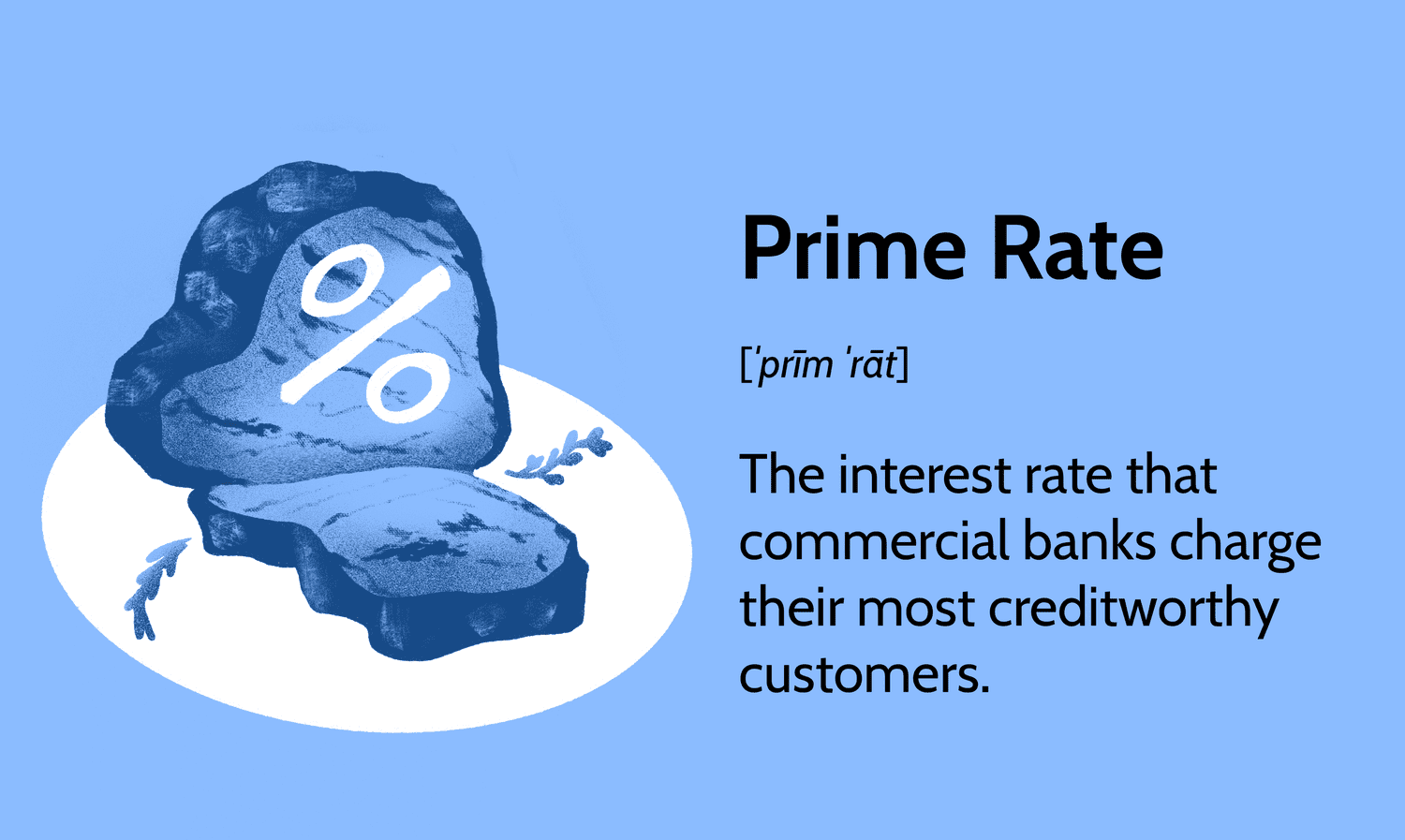

The prime lending rate is the interest rate at which banks and other financial institutions lend money to their most creditworthy customers. It serves as a benchmark rate, setting the foundation for the interest rates charged on various loans offered by these financial institutions. The prime lending rate is typically determined by the financial institution itself, but it may also be influenced by external factors such as the central bank’s monetary policy and prevailing economic conditions.

Financial institutions use the prime lending rate as a reference point when setting interest rates for mortgages, personal loans, business loans, and other forms of credit. The rate is usually expressed as a percentage above or below the prevailing prime rate. For example, a mortgage might be advertised as “prime rate plus 1%,” meaning the interest rate on the loan would be 1% higher than the current prime lending rate.

An important distinction to note is that the prime lending rate is not exclusive to one specific rate applicable worldwide. Different countries and regions may have their own prime lending rates, as they are influenced by factors unique to their economies. As a result, the prime lending rate can vary from one country to another and may fluctuate over time in response to changes in economic conditions.

It is crucial to understand that the prime lending rate is reserved for the most creditworthy borrowers. These individuals or businesses demonstrate a strong credit history and are less likely to default on their loan payments. Financial institutions generally reserve their most favorable interest rates for borrowers with excellent credit scores and a low risk of default. Consequently, borrowers with less favorable credit profiles might be offered loans at higher interest rates, often referred to as subprime rates.

Overall, the prime lending rate provides a standard reference point for interest rates in the lending industry. By understanding this concept, borrowers can better evaluate loan offers and negotiate favorable terms based on prevailing prime rates.

How Is the Prime Lending Rate Determined?

The determination of the prime lending rate is influenced by various factors, both internal and external to financial institutions. While the specific method of calculation may vary among different institutions, the following elements commonly play a role in determining the prime lending rate:

1. Central Bank’s Monetary Policy: Central banks, such as the Federal Reserve in the United States or the Bank of England in the United Kingdom, can have a direct impact on the prime lending rate. These institutions set the prevailing interest rates for a nation’s economy, often referred to as the benchmark interest rate. Financial institutions use the central bank’s interest rate as a baseline when determining their own prime lending rate. Changes in the central bank’s interest rate can lead to corresponding adjustments in the prime lending rate.

2. Economic Conditions: The overall economic health of a country or region can influence the prime lending rate. Factors such as inflation, GDP growth, employment rates, and consumer spending patterns are carefully considered by financial institutions. In times of economic growth and stability, financial institutions may be more inclined to lower their prime lending rates. Conversely, during times of economic volatility or recession, institutions may increase prime lending rates to mitigate risk.

3. Cost of Funds: Financial institutions borrow money to lend to their customers. The cost at which they can borrow funds directly impacts the prime lending rate. If the cost of borrowing for financial institutions increases, they may adjust their prime lending rate accordingly to maintain profitability. Conversely, if the cost of borrowing decreases, institutions may lower their prime lending rates to attract borrowers and stimulate lending activities.

4. Competitors’ Rates: The rates offered by competitors in the lending industry can also influence the prime lending rate. Financial institutions monitor market trends and adjust their rates to remain competitive. If a competitor lowers its prime lending rate to attract borrowers, other institutions may feel compelled to follow suit to avoid losing customers.

5. Creditworthiness of Borrowers: While financial institutions use the prime lending rate as a benchmark, individual borrowers’ creditworthiness can also impact the interest rate offered to them. Borrowers with strong credit histories and high credit scores are more likely to receive favorable interest rates, often lower than the prime lending rate. On the other hand, borrowers with less favorable credit profiles or higher perceived risk may be offered loans at higher interest rates.

It is important to note that financial institutions have the discretion to set their own prime lending rate within certain boundaries. While they are influenced by external factors as mentioned above, they also consider their own internal costs and profit objectives when determining the prime lending rate.

Importance of the Prime Lending Rate

The prime lending rate plays a crucial role in the financial landscape and holds significant importance for both borrowers and financial institutions. Here are some key reasons why the prime lending rate is important:

1. Setting Benchmark Interest Rates: The prime lending rate serves as a benchmark for determining interest rates on various loans offered by financial institutions. It provides a standard reference point against which lenders can calculate the interest rates they offer to borrowers. This benchmark ensures consistency and transparency in the lending industry, enabling borrowers to compare loan offers from different institutions and make informed decisions.

2. Impact on Borrowing Costs: Changes in the prime lending rate directly affect borrowing costs for individuals and businesses. When the prime lending rate increases, interest rates on loans tied to this rate also rise. This leads to higher monthly loan repayments and increased borrowing costs for borrowers. Conversely, when the prime lending rate decreases, borrowers may benefit from lower interest rates and reduced borrowing costs, making loans more affordable.

3. Economic Indicator: The prime lending rate is closely monitored by economists, policymakers, and financial analysts as an indicator of the overall economic health of a country or region. Changes in the prime lending rate reflect changes in the cost of borrowing, which can impact consumer spending, business investments, and overall economic growth. Consequently, fluctuations in the prime lending rate can be used as a gauge for assessing the current state of the economy.

4. Influencing Monetary Policy: Central banks and monetary authorities closely monitor the prime lending rate to guide their monetary policy decisions. By adjusting the benchmark interest rate, central banks can influence borrowing costs and stimulate or constrain economic activity. They may increase the prime lending rate to control inflation or slow down an overheating economy, or lower the rate to encourage borrowing and stimulate economic growth. The prime lending rate, therefore, acts as a lever for policymakers to manage monetary policy effectively.

5. Flexibility for Financial Institutions: Financial institutions use the prime lending rate to make adjustments to their interest rates based on their own business objectives and risk assessment. While the prime lending rate provides a reference point, financial institutions have the flexibility to offer interest rates above or below the prime rate, depending on factors such as creditworthiness and the perceived risk of the borrower. This flexibility allows lenders to tailor loan offers to specific market segments and manage their risk exposure effectively.

Overall, the prime lending rate holds considerable importance in the lending industry. It serves as a benchmark for interest rates, influences borrowing costs, provides insights into the economic climate, guides monetary policy decisions, and offers flexibility for financial institutions. Understanding the significance of the prime lending rate empowers borrowers to make informed decisions about loan options and helps financial institutions navigate the complex dynamics of the lending landscape.

Effects of Changes in the Prime Lending Rate

Changes in the prime lending rate can have far-reaching effects on various stakeholders in the financial system. These effects can impact borrowers, lenders, the overall economy, and even investment markets. Let’s explore some of the key effects that changes in the prime lending rate can have:

1. Borrowing Costs: One of the most direct and immediate effects of changes in the prime lending rate is on borrowing costs. When the prime lending rate increases, it leads to higher interest rates on loans tied to this rate. This means that borrowers will have to pay more in interest, resulting in increased monthly loan payments and potentially higher overall borrowing costs. Conversely, when the prime lending rate decreases, borrowers may enjoy lower interest rates, making loans more affordable.

2. Consumer Spending and Borrowing: Changes in the prime lending rate can significantly impact consumer spending and borrowing patterns. When the prime lending rate decreases, consumers may be more inclined to take on new loans, such as mortgages or personal loans, as the cost of borrowing decreases. This can stimulate consumer spending and boost economic activity. On the other hand, an increase in the prime lending rate may discourage borrowing and lead to reduced consumer spending, potentially slowing down economic growth.

3. Business Investments: Businesses also feel the effects of changes in the prime lending rate. When borrowing costs are low due to a decrease in the prime lending rate, businesses may take advantage of this opportunity to borrow funds for investments, expansion, or other capital expenditures. This can contribute to increased business activity, job creation, and economic growth. Conversely, an increase in the prime lending rate can constrain business investments, as higher borrowing costs may make it less attractive for businesses to take on new debt.

4. Mortgage Markets: The prime lending rate plays a significant role in the mortgage market. Mortgage interest rates are often tied to the prime lending rate, so changes in the prime rate directly impact mortgage rates. When the prime lending rate decreases, mortgage rates tend to follow suit, making homeownership more affordable and potentially driving increased demand for homes. Conversely, an increase in the prime lending rate leads to higher mortgage rates, which can deter potential homebuyers and slow down the real estate market.

5. Investment Markets: Changes in the prime lending rate can have repercussions in the investment markets as well. When interest rates are low due to a decrease in the prime lending rate, investors may seek higher-yield investments such as stocks or real estate. This increased demand can potentially drive up asset prices. Conversely, an increase in the prime lending rate may make fixed-income investments more attractive, leading investors to shift their funds into bonds or other interest-bearing instruments.

It is important to note that the impact of changes in the prime lending rate may not be immediate or universal. Different industries and sectors of the economy may experience variations in the effects based on their sensitivity to borrowing costs. Additionally, the response of borrowers and lenders to changes in the prime lending rate can be influenced by other factors such as consumer confidence, prevailing economic conditions, and government policies.

In summary, changes in the prime lending rate have wide-ranging effects on borrowing costs, consumer spending, business investments, mortgage markets, and investment markets. Understanding these effects can help borrowers, lenders, and investors make informed decisions and navigate the dynamic economic landscape.

Pros and Cons of the Prime Lending Rate

Like any financial instrument or concept, the prime lending rate has both advantages and disadvantages. Let’s explore some of the pros and cons associated with the prime lending rate:

Pros:

1. Transparency: The prime lending rate provides transparency and standardization in the lending industry. It serves as a benchmark against which borrowers can compare loan offers from different financial institutions. This transparency allows borrowers to make informed decisions and understand the competitiveness of the interest rates they are offered.

2. Market-Driven Rates: The prime lending rate is influenced by market forces, including the central bank’s monetary policy and prevailing economic conditions. This ensures that interest rates are responsive to changes in the overall economic landscape. Market-driven rates help create a balance between the cost of borrowing and the potential for economic growth.

3. Flexibility: The prime lending rate provides flexibility for financial institutions to adjust their interest rates based on their own risk assessment and profit objectives. This flexibility enables lenders to tailor interest rates to match the creditworthiness of borrowers and the perceived risk associated with the loan. It allows lenders to manage their risk exposure effectively and offer competitive rates to borrowers.

4. Monetary Policy Tool: Changes in the prime lending rate play a crucial role in monetary policy. Central banks can adjust the benchmark interest rate to control inflation, stimulate economic growth, or manage other macroeconomic objectives. The prime lending rate acts as a channel through which monetary policy decisions are transmitted to borrowers and the broader economy.

Cons:

1. Limited Impact on Subprime Borrowers: The prime lending rate primarily benefits borrowers with strong credit histories and low risk profiles. However, borrowers with less favorable credit profiles or higher risk levels may not qualify for loans tied to the prime rate. These subprime borrowers may end up being charged higher interest rates, limiting their access to affordable credit.

2. Vulnerability to Economic Changes: The prime lending rate is influenced by economic conditions and market forces. In times of economic instability or recession, financial institutions may increase the prime lending rate to mitigate risk. This can lead to higher borrowing costs for consumers and businesses, potentially impacting consumer spending, business investments, and economic growth.

3. Limited Flexibility for Borrowers: While financial institutions have flexibility in setting interest rates, borrowers may have limited leverage in negotiating the terms of loans tied to the prime lending rate. When the prime lending rate increases, borrowers may have little control over the resulting higher interest rates. This lack of flexibility can restrict borrowers’ ability to manage their monthly loan repayments and overall borrowing costs.

4. Dependency on Market Conditions: The prime lending rate is influenced by market conditions, including the central bank’s monetary policy and changes in economic indicators. As a result, borrowers may face uncertainty regarding future changes in the prime lending rate and the resulting impact on their loan repayments. This market dependency can make it challenging for borrowers to plan their financial commitments with certainty.

It is important to note that the pros and cons of the prime lending rate can differ based on individual circumstances and market conditions. Borrowers should carefully consider their own financial situation and risk tolerance when evaluating loan options tied to the prime lending rate. Understanding the advantages and disadvantages can help borrowers make informed decisions and choose the loan structure that aligns with their needs.

Factors to Consider When Choosing Loans with Prime Lending Rates

When considering loans tied to the prime lending rate, it is important to take into account various factors to ensure that you make an informed decision. Here are some key factors to consider when choosing loans with prime lending rates:

1. Creditworthiness: Your creditworthiness plays a significant role in the interest rates you will be offered. Lenders consider factors such as credit history, credit score, and debt-to-income ratio when determining the interest rate on your loan. Borrowers with strong credit profiles typically qualify for more favorable interest rates. Therefore, before applying for a loan, it is essential to check and improve your credit score if needed.

2. Loan Term: The loan term, or the duration of repayments, can affect the overall cost of the loan. A longer loan term typically results in lower monthly payments but may lead to higher total interest paid over the life of the loan. Conversely, a shorter term can mean higher monthly payments but lower overall interest costs. It is important to consider your financial situation and choose a loan term that aligns with your ability to make timely repayments.

3. Lock-In Period: Some loans with prime lending rates may offer a lock-in period, during which the interest rate remains fixed. This can provide stability and protect against interest rate fluctuations during the lock-in period. However, it is crucial to understand the terms and conditions of the lock-in period, including any potential penalties for early repayment or refinancing.

4. Loan Fees and Charges: When comparing loan options, it is important to consider not only the interest rate but also any associated fees and charges. These can include origination fees, application fees, appraisal fees, and prepayment penalties. Taking into account these additional costs allows for a more accurate assessment of the overall affordability of the loan.

5. Flexibility of Repayments: Evaluate the repayment options and flexibility offered by the lender. Some loans may allow for additional repayments or early repayments without incurring penalties. Others may offer flexible repayment schedules, such as bi-weekly or monthly options. Understanding the flexibility of repayment terms can help you better manage your loan and potentially save on interest costs.

6. Market Research: Conduct thorough market research to compare loans from different financial institutions. Look beyond the interest rate and consider other factors such as the reputation and reliability of the lender, customer service, and online banking capabilities. This research can help you find a trusted lender that offers competitive loan options tied to the prime lending rate.

7. Economic Outlook: Keep an eye on economic indicators and market trends that may influence the prime lending rate. Stay informed about changes in the central bank’s interest rates, inflation, GDP growth, and other factors that can impact the overall economy. This knowledge can help you anticipate potential changes in interest rates and make strategic decisions regarding your loan options.

By carefully considering these factors, you can make an informed decision when choosing loans with prime lending rates. Remember to thoroughly review the terms and conditions, seek advice if needed, and assess your financial capability before taking on any debt.

Conclusion

The prime lending rate is a critical component of the lending industry, serving as a benchmark for interest rates on loans offered by financial institutions. Understanding the definition, determination, and importance of the prime lending rate is crucial for borrowers and lenders alike.

By analyzing the effects of changes in the prime lending rate, borrowers can anticipate how these changes will impact their borrowing costs, consumer spending, and business investments. It is important to weigh the pros and cons associated with loans tied to the prime lending rate, considering factors such as creditworthiness, loan terms, fees, and market conditions.

Factors such as creditworthiness, loan terms, lock-in periods, loan fees, and flexibility of repayments should be carefully considered when choosing loans with prime lending rates. Conducting thorough market research and keeping an eye on the economic outlook can aid in making informed decisions regarding loan options.

Ultimately, understanding the intricacies of the prime lending rate empowers borrowers to make informed decisions about their loans and navigate the borrowing process effectively. It is essential for lenders to consider market conditions and risk factors when determining the prime lending rate, ensuring a balance between profitability and competitiveness.

With this comprehensive guide, you now have a solid understanding of the prime lending rate and its significance in the lending industry. Armed with this knowledge, you can confidently navigate the world of borrowing, evaluate loan options, and make informed decisions aligned with your financial goals and circumstances.