Definition of Risk in Banking

Risk in banking refers to the probability of loss or negative consequences arising from various factors that can impact a bank’s financial stability, operations, and reputation. It is an inherent part of the banking industry, as banks engage in a range of financial activities that involve uncertainties and potential hazards.

Banks face a multitude of risks due to the complexities of their operations and the dynamic nature of financial markets. These risks can arise from both internal and external factors, and their impact can vary in terms of severity and duration.

One of the fundamental risks in banking is credit risk, which occurs when borrowers are unable to repay their loans or meet their financial obligations. Another crucial risk is market risk, which includes fluctuations in interest rates, exchange rates, and asset prices that can result in losses for the bank.

Operational risk is another significant risk that banks face, arising from internal processes, systems, human errors, or external events. It encompasses risks related to technology failures, fraud, legal and compliance issues, and disruptions in business operations.

Liquidity risk refers to the risk of insufficient funds or assets to meet the bank’s financial obligations, while interest rate risk arises from changes in interest rates that can affect the profitability of a bank’s operations.

Foreign exchange risk pertains to the potential losses arising from changes in exchange rates when dealing with foreign currencies, while regulatory risk involves risks associated with compliance with legal and regulatory requirements imposed by governing bodies.

Reputational risk, though intangible, is crucial for banks as a loss of reputation can lead to a decline in customer trust, loss of business, and erosion of market value.

Emerging risks in banking also pose new challenges for banks, including cybersecurity risks, climate-related risks, and geopolitical risks that can impact both financial stability and profitability.

Overall, the understanding and management of various risks in banking are essential to ensure the stability, sustainability, and profitability of financial institutions. By identifying, assessing, and implementing appropriate risk management measures, banks can navigate the complex landscape of risks and safeguard their financial health.

Types of Risks in Banking

When it comes to banking, there are several types of risks that institutions need to be aware of and manage effectively. Understanding these risks is crucial for banks to maintain financial stability and protect their interests. The following are some of the main types of risks in banking:

- Credit Risk: This risk arises from borrowers’ inability to repay their loans or meet their financial obligations. It is one of the most significant risks for banks and can result in loan defaults, non-performing assets, and financial losses.

- Market Risk: Market risk refers to the potential losses that a bank may incur due to fluctuations in interest rates, exchange rates, and asset prices. The value of a bank’s investments and securities can be significantly affected by changes in the financial markets.

- Operational Risk: Operational risk stems from internal processes, human errors, technological failures, or external events. It includes risks related to fraud, disruptions in business operations, legal and compliance issues, and inadequate internal controls.

- Liquidity Risk: Liquidity risk arises when a bank does not have sufficient funds or liquid assets to meet its financial obligations. It can occur due to unforeseen withdrawals by depositors or difficulties in accessing funding sources when needed.

- Interest Rate Risk: Interest rate risk refers to the potential impact of changes in interest rates on a bank’s profitability and financial position. Banks with a significant amount of fixed-rate assets and liabilities are particularly vulnerable to this risk.

- Foreign Exchange Risk: This risk relates to potential losses resulting from changes in exchange rates when dealing with foreign currencies. Banks engaged in international transactions and currency conversions are exposed to foreign exchange risk.

- Regulatory Risk: Regulatory risk involves challenges and uncertainties associated with complying with legal and regulatory requirements. Changes in regulations, policies, and compliance standards can have a significant impact on a bank’s operations and profitability.

- Reputational Risk: Reputational risk is the risk of damage to a bank’s reputation or brand image, which can occur due to negative public perception, customer dissatisfaction, or involvement in controversial activities. A loss of reputation can lead to a decline in customer trust and result in financial losses.

It is essential for banks to identify these risks and implement effective risk management strategies and controls. Through ongoing monitoring, assessment, and mitigation of these risks, banks can minimize potential losses and enhance their overall financial resilience.

Credit Risk

Credit risk, also known as default risk or counterparty risk, is one of the primary risks in banking. It refers to the potential loss stemming from borrowers’ inability to repay their loans or meet their financial obligations. Banks extend credit to customers in various forms, including loans, mortgages, credit cards, and lines of credit. However, there is always a chance that borrowers may default on their payments, which can lead to financial losses for the bank.

This risk arises due to several factors, including the financial condition of the borrower, their creditworthiness, and the overall economic environment. Banks assess the creditworthiness of borrowers before extending credit by analyzing factors such as credit history, income stability, and debt-to-income ratio. This evaluation helps determine the probability of a borrower defaulting on their payments.

One of the key tools banks use to manage credit risk is credit scoring, which involves assigning a numerical value to borrowers based on their creditworthiness. This enables banks to make informed decisions about whether to extend credit and at what terms. Additionally, banks may require collateral or guarantees to mitigate the risk of credit defaults.

It is important for banks to have robust credit risk management practices in place to control and mitigate potential losses. Some common strategies include diversifying the loan portfolio across different sectors and industries, setting appropriate credit limits, and closely monitoring the repayment behavior of borrowers.

Moreover, effective loan underwriting practices, such as thorough due diligence and rigorous assessment of borrowers’ financial information, can help identify potential credit risks early on. Ongoing monitoring of the loan portfolio is also crucial to identify any deteriorating credit quality and take appropriate actions to mitigate the risk.

In scenarios where borrowers do default on payments, banks may employ various measures to recover the outstanding amounts, such as legal action, debt restructuring, or loan write-offs. However, it is essential for banks to strike a balance between managing credit risk and supporting economic growth by extending credit to individuals and businesses.

Overall, credit risk is an inherent part of the banking industry, and banks must have robust processes and systems in place to assess, manage, and mitigate this risk. By employing sound credit risk management practices, banks can minimize potential losses and maintain a healthy loan portfolio.

Market Risk

Market risk is a significant risk faced by banks and refers to the potential losses that can arise from fluctuations in interest rates, exchange rates, and asset prices. Banks engage in a range of activities and have various investments that are subject to market movements, making them susceptible to market risk.

Interest rate risk is a key component of market risk, which arises from changes in interest rates. Banks are exposed to interest rate risk in their lending and borrowing activities, as well as in their investment portfolios. Fluctuations in interest rates can impact a bank’s profitability and net interest margin, as well as the value of its fixed-rate assets and liabilities.

Exchange rate risk is another aspect of market risk that banks face when dealing with foreign currencies. Banks that engage in international transactions or have overseas operations are exposed to the risk of currency fluctuations. Changes in exchange rates can affect the profitability of these transactions and can result in gains or losses for the bank.

Asset price risk is also a significant component of market risk. Banks hold various financial assets, such as stocks, bonds, and derivatives, whose values can fluctuate in response to market conditions. Changes in asset prices can have a direct impact on a bank’s financial position and capital adequacy.

To manage market risk, banks employ various risk management techniques. They may use derivatives, such as futures, options, and swaps, to hedge against adverse market movements. Derivatives allow banks to protect themselves against potential losses by offsetting the risk associated with their existing positions.

Additionally, banks monitor market indicators and economic data to anticipate changes in interest rates, exchange rates, and asset prices. By staying informed about market trends, banks can make informed decisions about their investment strategies and positions.

To mitigate market risk, banks may diversify their investment portfolios across different asset classes and markets. Diversification helps spread the risk and reduces the potential impact of adverse market events on the overall portfolio. It is important for banks to balance risk and return when making investment decisions.

Regular stress testing and scenario analysis are also crucial tools for managing market risk. By simulating various adverse market scenarios, banks can assess the potential impact on their portfolios and determine whether they have sufficient capital and liquidity to withstand those scenarios.

In summary, market risk is a key risk faced by banks due to their exposure to fluctuations in interest rates, exchange rates, and asset prices. Effective risk management practices, such as hedging, diversification, and stress testing, can help banks mitigate potential losses and maintain financial stability in the face of market volatility.

Operational Risk

Operational risk is a significant risk faced by banks that arises from internal processes, human errors, technological failures, or external events. It encompasses a broad range of risks associated with bank operations and can have a significant impact on a bank’s financial health and reputation.

One of the main sources of operational risk is human error. Mistakes made by bank employees, whether in data entry, transaction processing, or judgment errors, can result in financial losses. Banks have to rely on robust internal controls and procedures to minimize the likelihood of human error and mitigate its potential impact.

Technological failures pose another significant operational risk to banks. This includes disruptions in information systems, cybersecurity breaches, and technology infrastructure failures. Banks heavily rely on technology for their daily operations, and any failure can result in business interruptions, unauthorized access to sensitive data, and financial losses.

External events, such as natural disasters, pandemics, or regulatory changes, can also lead to operational risks for banks. These events may disrupt a bank’s operations and cause financial losses if proper contingency plans and risk management procedures are not in place.

Fraud and misconduct are additional operational risks that banks face. This can include insider trading, money laundering, or unethical behavior by employees or third parties. Banks need to have strict compliance measures, internal audit processes, and whistleblower mechanisms to detect and prevent fraudulent activities.

Compliance risk is another aspect of operational risk, referring to the risk arising from non-compliance with laws, regulations, and industry standards. Banks need to stay updated on evolving regulations and ensure that their operations and procedures are in line with the applicable requirements.

To manage operational risk, banks implement various measures. This includes implementing robust internal controls, segregation of duties, and ensuring proper risk assessment and monitoring mechanisms are in place. Banks also invest heavily in cybersecurity systems and training to protect against technology-related risks.

Regular internal audits are conducted to identify any weaknesses or gaps in operational processes, allowing banks to take necessary corrective actions. Additionally, banks often have disaster recovery plans and business continuity plans to mitigate operational disruptions due to external events.

Overall, operational risk is a significant concern for banks, as it can have far-reaching consequences for financial stability and reputation. By implementing effective risk management practices, investing in technology and cybersecurity, and maintaining a strong culture of compliance, banks can mitigate operational risks and safeguard their operations.

Liquidity Risk

Liquidity risk is a critical risk faced by banks and refers to the potential inability of a bank to meet its financial obligations due to a shortage of funds or liquid assets. It is essential for banks to have sufficient liquidity to support their day-to-day operations, meet withdrawal requests from depositors, and fulfill other financial commitments.

Liquidity risk can arise due to several factors, including unexpected deposit withdrawals, the inability to access funding sources, or a disruption in the financial markets. If a bank does not have adequate liquidity, it may be forced to sell assets at unfavorable prices or raise funds at higher costs, leading to financial losses and a decline in confidence among depositors and investors.

Managing liquidity risk involves maintaining a balance between liquidity needs and profitability. Banks need to ensure that they have enough liquid assets, such as cash, government securities, and highly marketable securities, to meet their short-term funding requirements. They must also consider the repayment terms and potential variability in cash flows associated with their loan portfolio.

One common measure banks use to manage liquidity risk is maintaining a liquidity reserve. This involves setting aside a portion of funds in highly liquid assets that can be readily available in case of emergencies or unexpected liquidity needs. Banks also establish contingency funding plans to address potential liquidity shortfalls in adverse scenarios.

Banks also assess their cash flow projections and stress test their liquidity positions to evaluate their resilience under different liquidity scenarios. By conducting these stress tests, banks can identify potential vulnerabilities and take proactive measures to mitigate liquidity risks.

Central banks play a vital role in managing liquidity risk in the banking system. They act as lenders of last resort by providing emergency liquidity assistance to troubled banks during times of financial stress. Central banks also monitor banks’ liquidity positions and set regulatory standards to ensure that banks maintain sufficient liquidity buffers.

Moreover, banks need to maintain a diversified funding base to mitigate liquidity risk. Relying heavily on one source of funding can make a bank vulnerable to sudden changes in market conditions or disruptions in funding markets. Hence, banks explore multiple funding sources, such as deposits, interbank borrowing, and capital market financing.

Overall, effective liquidity risk management is essential for the financial stability and sustainability of banks. By maintaining an appropriate liquidity position, conducting regular stress tests, diversifying funding sources, and following regulatory guidelines, banks can mitigate liquidity risk and ensure their ability to meet financial obligations.

Interest Rate Risk

Interest rate risk is a significant risk faced by banks and refers to the potential impact of changes in interest rates on a bank’s profitability and financial position. Banks are heavily exposed to interest rate risk as they engage in various activities that involve interest rate-sensitive assets and liabilities.

When interest rates change, it can affect a bank’s earnings and the value of its assets and liabilities. For example, an increase in interest rates can lead to higher borrowing costs for banks and reduce the demand for loans, resulting in lower interest income. On the other hand, a decrease in interest rates can lower the income generated from interest-earning assets.

Banks with a significant amount of fixed-rate loans or long-term assets are particularly vulnerable to interest rate risk. This is because the income generated from these assets remains fixed, even if market interest rates rise. Conversely, banks with variable-rate assets and liabilities may experience fluctuations in their interest income and expenses, depending on the changes in interest rates.

To manage interest rate risk, banks employ various hedging techniques. This includes using interest rate derivatives, such as interest rate swaps, futures, and options, to hedge against adverse interest rate movements. These derivatives help banks offset the risks associated with changes in interest rates and protect their profitability.

Another strategy to mitigate interest rate risk is asset-liability management (ALM). Banks carefully match the maturities and repricing characteristics of their assets and liabilities to reduce exposure to interest rate fluctuations. This involves actively managing the duration and repricing gaps to minimize the impact of interest rate movements on the bank’s net interest income.

Stress testing and scenario analysis are also crucial tools in managing interest rate risk. Banks model different interest rate scenarios and assess the potential impact on their earnings, net asset values, and capital adequacy. By simulating adverse interest rate movements, banks can evaluate their resilience and take appropriate risk management actions.

Furthermore, central banks play a role in managing interest rate risk by setting and adjusting benchmark interest rates. Changes in these rates can have a direct impact on banks’ lending and borrowing costs, as well as the overall interest rate environment.

Overall, effective management of interest rate risk is essential for banks to maintain financial stability and profitability. By employing hedging strategies, conducting ALM practices, performing stress tests, and staying informed about developments in interest rates, banks can mitigate the potential adverse effects of interest rate fluctuations on their operations.

Foreign Exchange Risk

Foreign exchange risk, also known as currency risk, is a significant risk faced by banks when dealing with foreign currencies. It refers to the potential losses that can arise from changes in exchange rates between different currencies. Banks engaged in international transactions or currency conversions are exposed to foreign exchange risk.

When a bank holds assets, liabilities, or conducts transactions in foreign currencies, fluctuations in exchange rates can affect its financial position and profitability. If the value of a bank’s assets denominated in a foreign currency decreases relative to its liabilities, it can result in financial losses.

For example, if a bank grants a loan denominated in a foreign currency, and the exchange rate of that currency depreciates against the bank’s home currency, the value of the loan will decrease when converted back to the home currency. This can lead to a reduction in the bank’s profitability.

To manage foreign exchange risk, banks utilize various risk management techniques. One common practice is hedging, where banks use currency derivatives, such as forward contracts, options, and swaps, to offset the potential losses resulting from adverse exchange rate movements. These derivatives provide banks with the ability to lock in exchange rates and protect against currency fluctuations.

Another strategy is maintaining a diversified currency portfolio. Banks may hold a mix of assets and liabilities denominated in different currencies, which can help mitigate the impact of fluctuations in a particular currency. By diversifying their currency exposure, banks reduce their vulnerability to the performance of a single currency.

Banks also closely monitor exchange rate movements and stay informed about economic and geopolitical developments that can impact currency exchange rates. They may conduct currency risk analysis and stress testing to evaluate their resilience to potential adverse exchange rate movements.

Regulatory frameworks, such as capital adequacy standards, also play a role in mitigating foreign exchange risk. Banks are required to maintain adequate capital levels to absorb potential losses arising from foreign exchange fluctuations and other risks.

Additionally, central banks often influence exchange rates through their monetary policies. By adjusting interest rates and implementing currency intervention measures, central banks can influence the exchange rate movements to maintain stability in the foreign exchange market.

In summary, foreign exchange risk is an important consideration for banks engaged in international transactions and currency conversions. Through hedging, diversification, monitoring, and compliance with regulatory requirements, banks can manage foreign exchange risk and protect their financial position from adverse exchange rate movements.

Regulatory Risk

Regulatory risk is a type of risk faced by banks and refers to the potential challenges and uncertainties associated with complying with laws, regulations, and industry standards. Banks operate in a highly regulated environment, and changes in regulations and compliance requirements can significantly impact their operations and profitability.

Regulatory risk can arise from various sources, including changes in legislation, new regulatory requirements, and stricter enforcement actions by regulatory authorities. Banks need to stay updated on evolving regulations and ensure that their operations and procedures are in line with the applicable requirements.

Complying with regulations often involves investing in additional resources, implementing new systems and processes, and training employees to ensure adherence to regulatory standards. This can result in increased costs for banks as they allocate resources to maintain compliance.

Regulatory risk also includes the potential for non-compliance penalties, fines, or reputational damage due to violations of regulatory requirements. Regulatory authorities have the power to take enforcement actions against banks that fail to meet their obligations and can impose financial penalties or other sanctions.

Banks mitigate regulatory risks by establishing robust compliance frameworks and internal controls. This includes implementing policies and procedures to ensure adherence to regulations, conducting regular compliance audits, and maintaining open lines of communication with regulatory authorities.

Engaging in collaboration and information sharing with industry peers and participating in industry associations can also help banks stay informed about regulatory developments and best practices.

Regulatory risk management is not only important for compliance but also for maintaining the trust and confidence of customers, investors, and the public. Banks with a strong reputation for regulatory compliance are more likely to attract and retain customers and investors.

Additionally, regulatory risk is closely tied to other types of risks, such as operational risk and liquidity risk. Non-compliance with regulations can lead to operational disruptions, financial losses, and liquidity challenges, further highlighting the importance of effective risk management.

Regulatory risk is influenced by both domestic and international regulatory frameworks. Banks operating across jurisdictions need to navigate the regulatory requirements of different countries, taking into account the varying legal and regulatory environments.

Overall, managing regulatory risk is a critical aspect of banking operations. As regulations continue to evolve and become more complex, banks must remain vigilant, adapt to changes, and maintain a strong compliance culture to effectively manage regulatory risk.

Reputational Risk

Reputational risk is a critical risk faced by banks and refers to the potential damage to a bank’s reputation or brand image. It is an intangible risk that arises from negative public perception, customer dissatisfaction, ethical breaches, or involvement in controversial activities.

A strong reputation is a valuable asset for banks, as it builds trust, attracts and retains customers, and contributes to the long-term success of the institution. Conversely, a damaged reputation can lead to a decline in customer trust, loss of business, and erosion of market value.

Reputational risk can stem from various sources. One common source is poor customer experiences, such as inadequate customer service, unfair business practices, or breaches of customer privacy. Negative experiences can quickly spread through word-of-mouth, social media, and online reviews, damaging the bank’s reputation.

Another source of reputational risk is unethical behavior or fraudulent activities within the bank. Any involvement in fraudulent schemes, money laundering, or insider trading can undermine the bank’s integrity and trustworthiness.

Reputational risk also includes risks associated with environmental, social, and governance (ESG) factors. Increasingly, banks are evaluated based on their commitment to sustainable practices, diversity and inclusion, and responsible lending. Any failure in meeting these standards can have a detrimental impact on reputation.

Managing reputational risk requires a proactive approach. Banks must develop a strong corporate culture that promotes ethical behavior, transparency, and responsible practices. This includes setting clear ethical standards, implementing robust compliance programs, and fostering a strong risk management culture throughout the organization.

Additionally, banks need to actively engage with stakeholders, including customers, investors, employees, regulators, and the public. By maintaining open lines of communication, actively addressing concerns, and demonstrating a commitment to ethical practices, banks can build and maintain a positive reputation.

Monitoring and analyzing social media and online platforms is also crucial for managing reputational risk. By closely monitoring discussions and sentiment online, banks can identify potential reputational threats, address negative perceptions, and rectify any misinformation promptly.

Furthermore, responding effectively to reputational crises is vital. Banks must have contingency plans in place to manage and mitigate the impact of negative events on their reputation. Swift action, transparency, and effective communication can help restore trust and mitigate potential harm to the bank’s reputation.

Overall, reputational risk is a significant concern for banks due to its potential long-term consequences. By prioritizing ethical practices, maintaining strong stakeholder relationships, and promptly addressing concerns, banks can safeguard their reputation and enhance their competitive advantage in the market.

Emerging Risks in Banking

As the banking industry continues to evolve, new risks are emerging that banks must be aware of and effectively manage. These emerging risks pose unique challenges and uncertainties for financial institutions. Understanding and proactively addressing these risks are crucial to maintaining financial stability and sustaining long-term success. Here are some of the emerging risks in banking:

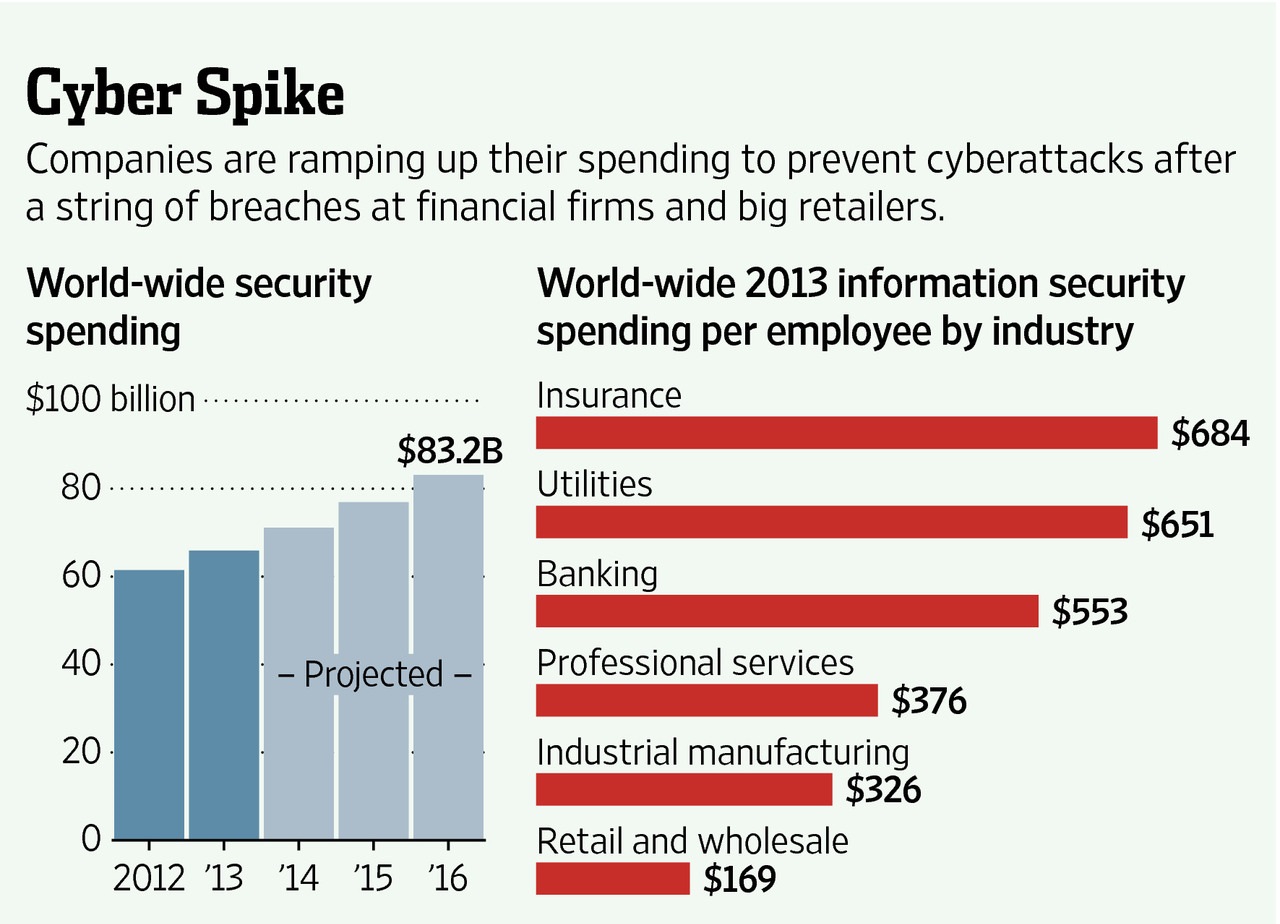

- Cybersecurity Risks: With the increasing reliance on technology, cyber threats have become a significant concern for banks. Cyberattacks, data breaches, and ransomware attacks can compromise sensitive customer information, disrupt operations, and result in financial losses. Banks need to invest in robust cybersecurity systems, implement strong data protection measures, and conduct regular testing and risk assessments to mitigate these risks.

- Climate-Related Risks: The impact of climate change presents new risks for banks. These include physical risks arising from extreme weather events, such as floods and storms, and transitional risks associated with shifts to a low-carbon economy. Banks need to assess the vulnerability of their loan portfolios to climate risks, adopt sustainable lending practices, and incorporate climate risk considerations into their risk management frameworks.

- Geopolitical Risks: Geopolitical events, such as trade disputes, political instability, and regulatory changes, can have a significant impact on the banking industry. Banks operating across borders need to stay updated on geopolitical developments, assess the potential risks to their operations and investments, and implement strategies to manage these risks effectively.

- Technology Risks: While technology advancements offer numerous benefits to the banking sector, they also introduce new risks. These include operational risks associated with technology failures, data privacy risks, and risks arising from the use of emerging technologies, such as artificial intelligence and blockchain. Banks need to adopt robust governance frameworks, implement adequate controls, and stay informed about technological advancements to navigate these risks.

- Compliance Risks: The regulatory landscape is continually evolving, and banks face challenges in keeping up with changing requirements. Non-compliance with regulations can result in financial penalties, reputational damage, and disruptions to operations. Banks need to have effective compliance programs, monitor regulatory developments, and invest in training and resources to ensure ongoing compliance.

These emerging risks require banks to enhance their risk management capabilities and embrace proactive risk mitigation strategies. By leveraging technological advancements, staying abreast of regulatory changes, adopting sustainable practices, and building strong risk cultures, banks can navigate the evolving risk landscape and seize opportunities while managing these emerging risks effectively.

Tools and Techniques for Managing Risks in Banking

Managing risks is a critical aspect of banking operations to ensure financial stability and protect the interests of banks and their stakeholders. While risks in banking are inherent, there are several tools and techniques that banks employ to identify, assess, and mitigate risks effectively. Here are some of the key tools and techniques for managing risks in banking:

- Risk Assessment and Identification: Banks conduct thorough risk assessments to identify and understand the various risks they face. This involves analyzing internal processes, market conditions, regulatory environments, and emerging risks to gain a comprehensive picture of the risks specific to the bank. Risk identification helps banks prioritize their risk management efforts and allocate resources effectively.

- Internal Controls and Risk Monitoring: Internal controls are crucial for managing risks in banking. Banks establish robust control frameworks to ensure compliance with regulations, mitigate operational risks, and safeguard assets. Regular risk monitoring and reporting mechanisms allow banks to track and assess risk exposure, identify trends, and take timely risk mitigation actions.

- Stress Testing and Scenario Analysis: Stress testing involves simulating adverse scenarios to evaluate the potential impact on a bank’s financial position and resilience. It helps banks assess their vulnerability to different risk factors and determine if they have sufficient capital, liquidity, and risk management measures in place to withstand severe shocks. Scenario analysis allows banks to test the impact of specific risk events on their portfolios and evaluate risk-reward trade-offs.

- Derivatives and Hedging: Banks use derivatives, such as futures, options, swaps, and forwards, to manage risks associated with interest rates, foreign exchange, and other market factors. These instruments provide banks with the ability to hedge against adverse movements in prices or rates, reducing the potential losses resulting from such risks.

- Risk Transfer and Insurance: Banks may transfer risks to external parties through insurance or by offloading certain assets or exposures. This helps diversify risk and protect the bank’s financial position. Insurance can be utilized to cover specific risks, such as credit default insurance or property insurance, to mitigate potential losses.

- Portfolio Diversification: Diversifying the bank’s portfolio is an effective risk management strategy. By spreading risk across different asset classes, sectors, and regions, banks can reduce concentration risk and minimize the impact of adverse events affecting a single investment. Diversification also allows banks to capture opportunities in different market segments.

- Governance and Risk Culture: Strong governance frameworks and risk cultures are essential for effective risk management. Banks need to establish clear roles and responsibilities, implement robust risk governance structures, and foster a risk-aware culture throughout the organization. This includes promoting risk awareness, providing training and education, and encouraging employees to identify and report risks.

These tools and techniques provide banks with the necessary means to manage risks effectively. Implementing these practices, in conjunction with comprehensive risk management frameworks and ongoing monitoring and assessment, allows banks to navigate the challenging and dynamic risk landscape in the banking industry.

Risk Management Framework in Banking

A robust risk management framework is essential for banks to effectively identify, assess, and mitigate risks. The risk management framework provides a structured approach for banks to manage risks at both the strategic and operational levels, ensuring the overall stability and resilience of the institution. Here are key components of a risk management framework in banking:

- Risk Governance: Risk governance sets the tone from the top and establishes the overall risk management culture within the bank. It involves defining the roles and responsibilities of the board of directors, senior management, risk committees, and other stakeholders in managing risks. Clear lines of accountability and effective communication channels are established to drive risk management decisions and actions.

- Risk Identification and Assessment: Banks systematically identify and assess risks through various means, including risk assessments, risk registers, and risk appetite frameworks. Risks are evaluated based on their potential impact, likelihood of occurrence, and correlation with other risks. This process helps banks prioritize risks and allocate resources accordingly.

- Risk Appetite and Tolerance: Defining risk appetite and tolerance levels is a critical component of the risk management framework. Risk appetite refers to the level of risk that a bank is willing to accept to achieve its business objectives. Risk tolerance sets the boundaries beyond which risks are deemed unacceptable. Establishing clear risk thresholds helps guide risk-taking decisions and aligns the bank’s risk exposures with its strategic goals.

- Risk Measurement and Monitoring: Banks employ quantitative and qualitative measures to assess and monitor risks on an ongoing basis. This involves the use of risk indicators, key risk metrics, and risk reporting mechanisms to provide timely and accurate risk information to key stakeholders. Regular monitoring and reporting enable banks to promptly identify and address emerging risks and ensure risk exposures remain within acceptable limits.

- Risk Mitigation and Control: Banks implement risk mitigation strategies and controls to reduce the impact of risks. This includes implementing internal controls, segregation of duties, and policies to manage risks effectively. Risk mitigation measures may include diversification of portfolios, hedging strategies, setting exposure limits, and adopting best practices in risk management.

- Risk Communication and Reporting: Effective communication of risks is crucial for informed decision-making and risk transparency. Banks communicate risk information to key stakeholders, including the board of directors, management, employees, regulators, and external parties. Risk reporting provides a comprehensive and concise overview of risks, their impact, and risk mitigation actions, facilitating risk-based decision-making throughout the organization.

A well-designed risk management framework ensures that risk management processes are embedded into the bank’s culture and operations. It helps banks identify potential risks, assess their impact, and take informed actions to manage and mitigate risks effectively. By continuously reviewing and improving the risk management framework, banks can enhance their risk management capabilities and adapt to evolving risk landscapes.

Key Players in Risk Management in Banking

Effective risk management in banking involves the collaboration and interaction of various key players who have specific roles and responsibilities. These key players work together to ensure that risks are properly identified, assessed, and managed. Here are the key players in risk management in banking:

- Board of Directors: The board of directors plays a crucial role in overseeing risk management in a bank. They set the risk appetite, establish risk management policies and frameworks, and ensure that adequate resources are allocated for risk management activities. The board is responsible for providing strategic direction, approving risk management strategies, and holding management accountable for risk management outcomes.

- Senior Management: Senior management, including the CEO and executive team, is responsible for implementing the board’s risk management directives and policies. They provide leadership and guidance in managing risks, ensure that risk management practices are integrated into the bank’s operations, and allocate resources for risk management activities. Senior management also sets the risk culture and tone from the top, promoting a strong risk-aware culture throughout the organization.

- Risk Management Committee: The risk management committee, often a subcommittee of the board, is responsible for overseeing and monitoring the bank’s risk management activities. This committee typically includes representatives from the board, senior management, and risk management experts. They review and provide guidance on risk management strategies, assess risk reports, and ensure that appropriate risk mitigation measures are in place.

- Chief Risk Officer (CRO): The Chief Risk Officer is a senior executive responsible for leading the risk management function within the bank. The CRO oversees the identification, measurement, and management of risks across the organization. They develop risk management policies and frameworks, ensure compliance with regulatory requirements, and provide risk-related insights and recommendations to the board and senior management.

- Business Line Managers: Business line managers are responsible for managing risks specific to their business units or divisions. They are accountable for effectively identifying, assessing, and mitigating risks within their respective areas of responsibility. Business line managers play a critical role in integrating risk management into day-to-day operations, adhering to risk policies, and reporting risk information to senior management and the risk management committee.

- Internal Audit: The internal audit function provides independent and objective evaluations of the bank’s risk management processes and controls. Internal auditors assess the effectiveness of risk management practices and provide assurance to the board and senior management that risks are being managed appropriately. They also make recommendations to improve risk management practices based on their audit findings.

- Compliance Officers: Compliance officers ensure that the bank adheres to relevant laws, regulations, and industry standards. They monitor compliance with regulatory requirements, assess the impact of changes in regulations on the bank’s operations, and implement compliance risk management strategies. Compliance officers work closely with the risk management function to ensure that compliance risks are identified, assessed, and addressed.

- External Auditors and Regulators: External auditors provide outside validation of the bank’s financial reporting and risk management activities. They assess the adequacy of the bank’s risk management practices during their annual audits. Regulatory bodies, such as central banks and financial supervisory authorities, play a crucial role in overseeing risk management in banking. They set regulatory standards, conduct examinations and assessments, and enforce compliance with regulatory requirements.

These key players in risk management collaborate and work together to create a strong risk management framework, ensure effective risk oversight, and maintain financial stability within the banking industry.

Role of Central Banks in Managing Risks in Banking

Central banks play a vital role in managing risks in the banking industry. As the primary regulatory and supervisory authorities, central banks are responsible for ensuring the stability and integrity of the banking system. They actively monitor and address risks that can impact the financial health of banks and the overall stability of the economy. Here are the key roles of central banks in managing risks in banking:

- Regulation and Supervision: Central banks establish and enforce regulatory frameworks to govern the activities of banks. They set prudential regulations and guidelines to ensure that banks maintain appropriate capital adequacy, liquidity, and risk management standards. Central banks conduct regular inspections, audits, and assessments to monitor compliance with these regulations and supervise the risk management practices of banks.

- Lender of Last Resort: Central banks act as lenders of last resort to provide emergency liquidity support to banks during times of financial stress. They ensure that banks have access to sufficient liquidity to meet their obligations and maintain their solvency. By providing this support, central banks help mitigate liquidity risk and prevent systemic disruptions in the banking sector.

- Monetary Policy and Interest Rate Management: Central banks manage monetary policy, including setting interest rates, to control inflation and stimulate economic growth. Changes in interest rates influence banks’ borrowing costs, lending rates, and profitability. Central banks’ effective management of interest rates helps banks manage interest rate risk and navigate the impacts of changing economic conditions.

- Macroprudential Policy: Central banks are responsible for implementing macroprudential policies that focus on managing systemic risks in the banking system. These policies aim to identify and address risks that can undermine financial stability, such as excessive credit growth, asset bubbles, or interconnectedness between institutions. By implementing measures like capital buffers, loan-to-value ratio limits, and stress testing, central banks promote the soundness and resilience of the banking sector.

- Crisis Management and Resolution: Central banks play a critical role in crisis management and resolution in the banking sector. They develop frameworks and procedures to address bank failures or financial crises effectively. Central banks work collaboratively with other government agencies, regulatory bodies, and international counterparts to ensure that appropriate measures are taken to safeguard financial stability and protect the interests of depositors and creditors.

- Research and Analysis: Central banks conduct research and analysis on various risks facing the banking sector. They assess systemic risks, monitor market trends, and analyze emerging risks to inform their regulatory decision-making. Central banks often publish reports and share insights on risk management practices, contributing to the overall knowledge and awareness of risk issues in the banking industry.

The role of central banks in managing risks extends beyond their direct oversight of individual banks. They have a broader mandate to preserve financial stability and promote the healthy functioning of the banking system. Through regulation, supervision, crisis management, and proactive risk mitigation measures, central banks play a crucial role in ensuring the resilience and soundness of the banking industry.

Importance of Risk Management in Banking

Risk management is of utmost importance in the banking industry due to the inherent nature of financial activities and the potential consequences of risks. Effective risk management practices are crucial for several reasons:

- Financial Stability: Risk management plays a vital role in maintaining the financial stability of banks. By identifying, assessing, and mitigating risks, banks are better equipped to withstand adverse events and disruptions. Proactive risk management helps banks maintain their solvency, liquidity, and overall financial health, safeguarding depositors’ funds and supporting a stable banking system.

- Protecting Stakeholder Interests: Banks have a fiduciary duty to protect the interests of their stakeholders, including customers, depositors, shareholders, and employees. Effective risk management helps banks fulfill this duty by minimizing the likelihood and impact of potential losses. It enhances transparency and builds trust with stakeholders, ensuring that their interests are safeguarded while providing access to reliable financial services.

- Compliance with Regulatory Requirements: The banking sector is highly regulated, and adherence to regulatory requirements is crucial. Effective risk management practices enable banks to comply with regulatory guidelines, laws, and industry best practices. It ensures that banks meet capital adequacy, liquidity, and risk management standards set by regulatory authorities, helping them avoid penalties and reputational damage.

- Optimal Allocation of Resources: Risk management allows banks to allocate resources effectively and manage risk-return trade-offs. By identifying and assessing risks, banks can make informed decisions regarding capital allocation, investment strategies, and loan underwriting. This helps optimize profitability, maintain a healthy risk profile, and reduce the likelihood of losses, ensuring long-term sustainability and growth.

- Enhanced Decision-Making: Risk management provides banks with comprehensive risk information, enabling informed decision-making at all levels of the organization. It supports strategic planning, capital allocation, and product development, allowing banks to seize opportunities while managing associated risks. Risk management also facilitates the evaluation of potential risks and rewards before making critical business decisions.

- Improved Operational Efficiency: Effective risk management practices contribute to operational efficiency within banks. By identifying and addressing operational risks, such as process inefficiencies, system failures, or human errors, banks can enhance their operational resilience, reduce costs, and improve customer service. Operational risk management also helps create a culture of continuous improvement and innovation.

- Protection of Reputational Capital: Reputational risk is a significant concern for banks, given the trust-based nature of the industry. Effective risk management helps mitigate reputational risks by identifying and addressing issues that can damage the bank’s reputation. Protecting reputational capital helps banks maintain customer trust, attract investors, and enhance their market standing.

Overall, risk management is vital for the stability, integrity, and profitability of banks. By implementing robust risk management practices, banks can navigate uncertainties, protect stakeholder interests, comply with regulations, and make informed decisions that contribute to their long-term success.

Case Studies on Risk Management in Banking

Examining real-world case studies provides valuable insights into the importance and impact of risk management in the banking industry. Here are a few examples:

- The Global Financial Crisis (2007-2008): The global financial crisis highlighted the significance of robust risk management practices. Banks that failed to properly manage risks associated with subprime mortgages, securitization, and complex financial instruments faced severe consequences. The crisis led to the collapse of several major financial institutions, highlighting the importance of risk identification, proper credit assessment, prudent lending practices, and effective liquidity management.

- JPMorgan Chase’s London Whale Incident (2012): In 2012, JPMorgan Chase faced significant losses resulting from a trading position taken by a trader referred to as the “London Whale.” The incident showcased the importance of risk governance, internal controls, and accurate risk reporting. It prompted JPMorgan Chase to improve its risk management practices, strengthen risk oversight, and enhance risk reporting mechanisms to prevent future occurrences.

- Barings Bank Collapse (1995): The collapse of Barings Bank demonstrated the severe consequences of inadequate risk management. Unauthorized and speculative trading by a single trader, Nick Leeson, resulted in enormous losses that eventually led to the bank’s bankruptcy. The incident highlighted the importance of effective risk controls, segregation of duties, and independent risk monitoring to mitigate the risk of fraudulent activities and unauthorized trading.

- Wells Fargo’s Account Fraud Scandal (2016): Wells Fargo faced a reputational crisis due to the revelation of widespread unauthorized account openings by its employees. The scandal showcased the criticality of risk culture, compliance, and ethical behavior within banks. It emphasized the need for robust risk governance, effective internal controls, and strong compliance mechanisms to detect and prevent fraudulent activities that can damage a bank’s reputation.

- HSBC Money Laundering Case (2012): HSBC was involved in a money laundering scandal where it failed to adequately manage risks associated with financial crime. The bank faced significant regulatory fines and reputational damage. The case highlighted the necessity of robust Anti-Money Laundering (AML) and Know Your Customer (KYC) processes, as well as effective risk controls and compliance procedures to mitigate the risks of money laundering and financial crime.

These case studies underscore the importance of risk identification, risk governance, compliance, internal controls, and effective risk culture in banks. They serve as reminders that proper risk management practices are essential for maintaining financial stability, protecting stakeholder interests, and upholding the reputation and integrity of banking institutions.

Conclusion

Risk management is a critical aspect of the banking industry that ensures financial stability, protects stakeholder interests, and maintains the integrity of the banking system. Banks face various risks, including credit risk, market risk, operational risk, liquidity risk, and more. Effectively managing these risks is essential for the long-term success and sustainability of banks.

Through the use of tools and techniques, such as risk assessments, internal controls, stress testing, derivatives, and diversification, banks can identify, assess, and mitigate risks. Central banks also play a crucial role in managing risks by enforcing regulations, providing liquidity support, and overseeing the stability of the banking system.

The importance of risk management in banking cannot be overstated. It protects stakeholders, including customers, depositors, and shareholders, and helps foster trust and confidence in the banking industry. Compliance with regulatory requirements is crucial for banks to avoid penalties and reputational damage.

Furthermore, effective risk management enhances decision-making capabilities, improves operational efficiency, and optimizes the allocation of resources within banks. It also safeguards reputational capital, given the significance of trust and confidence in the industry.

Real-world case studies, such as the global financial crisis, the collapse of Barings Bank, and various scandals, underscore the consequences of inadequate risk management and highlight the need for strong risk governance, internal controls, compliance, and risk culture within banks.

In conclusion, risk management is a fundamental and ongoing process that must be ingrained in the fabric of banking operations. By implementing robust risk management frameworks, banks can navigate uncertainties, protect stakeholders, comply with regulations, optimize resource allocation, and make informed decisions to ensure long-term success in an ever-evolving and challenging banking landscape.