Introduction

Welcome to the world of virtual banking accounts, where convenience and flexibility meet the demands of today’s digital and mobile-based economy. Virtual accounts have emerged as a popular alternative to traditional banking, providing users with a host of benefits and streamlining financial transactions.

Unlike traditional bank accounts that are tied to physical branches, virtual accounts exist solely in the digital realm. They allow users to manage their finances online, making payments, receiving funds, and monitoring their balance all with a few clicks or taps on their device of choice.

Virtual accounts have gained popularity in recent years due to their ease of use, accessibility, and the range of features they offer. Whether you’re an individual looking for a convenient way to manage your personal finances or a business owner seeking efficient cash management solutions, virtual accounts can be a game-changer for you.

In this article, we will explore the world of virtual accounts, discussing what they are, how they work, and the benefits they bring. We’ll also look at various use cases and compare virtual accounts to traditional bank accounts.

So, if you’re ready to dive into the world of virtual banking, let’s get started!

Definition of a Virtual Account

A virtual account, also known as a digital account or online account, is a type of bank account that exists solely in a digital format. It is accessed and managed through online banking platforms or mobile banking applications, eliminating the need for physical branch visits or paper-based transactions.

Unlike traditional bank accounts, virtual accounts are not associated with a specific physical location or a physical card. Instead, they are linked to the user’s digital identity, often tied to their email address or mobile phone number.

Virtual accounts offer a range of features and functionalities that allow users to perform various financial activities, such as making payments, receiving deposits, transferring funds, and monitoring account balances. These accounts can be used for both personal and business purposes, providing a convenient and efficient way to manage finances in the digital age.

One of the key characteristics of virtual accounts is their flexibility. Users can access their accounts anytime, anywhere, as long as they have an internet connection. This makes virtual accounts especially appealing for individuals or businesses with a nomadic lifestyle or those who prefer the convenience of online banking.

Moreover, virtual accounts often come with advanced security measures to safeguard users’ financial information. These include encryption protocols, two-factor authentication, and real-time fraud monitoring. As a result, users can have peace of mind knowing that their virtual accounts are protected from unauthorized access or fraudulent activities.

With the rise of fintech innovations, virtual accounts have become increasingly popular, offering an alternative to traditional banking that aligns with the evolving needs and expectations of consumers. They provide a digital-first approach to managing finances, offering convenience, flexibility, and enhanced accessibility.

In the next section, we will explore how virtual accounts work and delve into the underlying mechanisms that enable seamless digital banking experiences.

How Virtual Accounts Work

Virtual accounts operate through digital banking platforms or mobile applications provided by financial institutions or virtual account service providers. The process typically involves the following steps:

- Account Creation: To open a virtual account, users need to sign up through the online platform or mobile app. They may be required to provide personal information, such as their name, email address, and contact details. Some virtual account providers also perform identity verification to ensure compliance with regulatory requirements.

- Account Activation: Once the account creation process is complete, users receive an activation link or code to verify their email or mobile number. This step confirms their ownership and grants access to the virtual account.

- Linking with Existing Accounts: Users often have the option to link their virtual accounts with their existing traditional bank accounts. This allows easy fund transfers between the two accounts, providing added convenience.

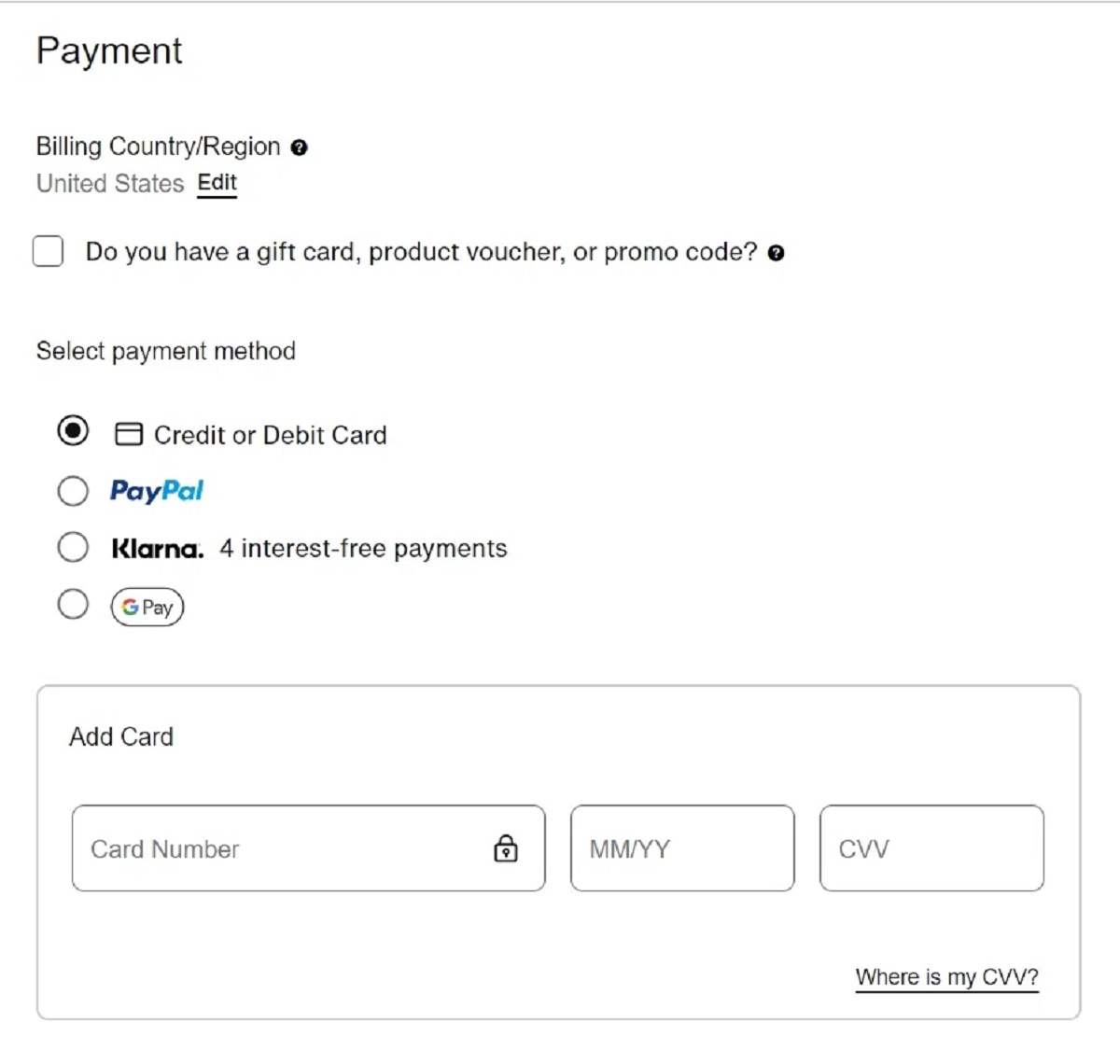

- Deposits and Payments: Once the virtual account is set up and linked to other accounts, users can start making deposits into their virtual account. This can typically be done through various methods, including bank transfers, electronic wallets, or online payment systems. Users can also make payments directly from their virtual accounts for online purchases, bill payments, or any other transactions.

- Transaction Monitoring: Virtual account platforms provide tools to monitor transactions and account balance in real-time. Users can view their transaction history, track spending patterns, and set up alerts for specific activities, such as low balance or large transactions.

- Security Measures: Virtual account providers implement robust security measures to protect users’ financial information. These may include encrypted connections, multi-factor authentication, and biometric authentication for added security.

Virtual accounts offer a seamless and user-friendly banking experience, allowing users to perform various financial activities with just a few clicks or taps. The availability of mobile apps further enhances the convenience, enabling users to manage their accounts on the go.

Next, let’s explore the benefits that virtual accounts bring to individuals and businesses alike.

Benefits of Virtual Accounts

Virtual accounts offer numerous benefits to individuals and businesses, revolutionizing the way we manage our finances. Here are some key advantages of using virtual accounts:

- Convenience: Virtual accounts provide unparalleled convenience, allowing users to access and manage their finances anytime, anywhere. Users can make transactions, receive payments, and monitor their account balances on-the-go through online banking platforms or mobile apps.

- Cost Savings: Virtual accounts often come with lower fees and transaction costs compared to traditional bank accounts. They eliminate the need for physical branch visits and paper-based transactions, resulting in cost savings for both individuals and businesses.

- Flexibility: With virtual accounts, users have the freedom to choose from a range of financial services and products that suit their needs. They can customize their accounts with features like automatic bill payments, recurring transfers, and budgeting tools.

- Enhanced Security: Virtual accounts prioritize security, implementing advanced encryption protocols, multi-factor authentication, and real-time fraud monitoring. Users can have peace of mind knowing that their financial information is protected from unauthorized access.

- Streamlined Cash Management: For businesses, virtual accounts offer efficient cash management solutions. Companies can have multiple virtual accounts for different purposes, such as segregating funds for payroll, suppliers, or specific projects. This simplifies financial tracking and improves accountability.

- Global Accessibility: Virtual accounts are not bound by geographical limitations, allowing users to send and receive funds internationally with ease. This is especially beneficial for businesses operating in global markets or individuals sending money to family or friends abroad.

- Scalability: Virtual accounts can easily adapt to the growing needs of businesses. With the ability to create multiple sub-accounts, businesses can efficiently manage funds for different departments, branches, or clients. This scalability contributes to improved financial control and decision-making.

These benefits make virtual accounts an attractive alternative to traditional banking, empowering users with greater control over their finances and simplifying financial processes for individuals and businesses alike.

Now that we’ve explored the benefits of virtual accounts, let’s delve into some use cases where virtual accounts prove to be particularly advantageous.

Use Cases for Virtual Accounts

Virtual accounts have a wide range of use cases that cater to the diverse needs of individuals and businesses. Here are some prominent examples:

- Online Shopping: Virtual accounts are ideal for online shopping, allowing users to make secure payments without the need for physical cards. Users can link their virtual accounts to e-commerce platforms, enabling seamless and hassle-free transactions.

- Freelancers and Gig Economy Workers: Virtual accounts provide freelancers and gig economy workers with a dedicated platform to receive payments for their services. Clients can directly transfer funds to the virtual account, streamlining the payment process and eliminating the need for paper checks or cash transactions.

- Travel and International Payments: Virtual accounts facilitate convenient and cost-effective international payments. Users can receive funds from abroad and make currency conversions within the virtual account, avoiding expensive fees associated with traditional international wire transfers.

- Business Expense Management: Virtual accounts enable businesses to efficiently manage their expenses. They can assign virtual accounts to employees for company-related expenses, track spending in real-time, and generate detailed expense reports.

- Subscription Services: Virtual accounts are useful for managing subscription services. Users can link their virtual accounts to recurring payment platforms, ensuring seamless and uninterrupted access to subscription-based products or services.

- Online Marketplaces and Platforms: Virtual accounts are often integrated with online marketplaces and platforms. Sellers can receive payments directly into their virtual accounts, providing a secure and streamlined payment process for e-commerce transactions.

- Event and Fundraising Management: Virtual accounts offer efficient solutions for event organization and fundraising efforts. Organizers can set up virtual accounts to collect ticket sales or donations, track contributions, and easily manage funds associated with the event or fundraising campaign.

These use cases illustrate the versatility and practicality of virtual accounts in various aspects of personal and business finance. They provide tailored solutions to meet specific needs, simplifying financial management and enhancing overall efficiency.

Now, let’s compare virtual accounts to traditional bank accounts to understand their key differences.

Virtual Accounts vs. Traditional Bank Accounts

Virtual accounts and traditional bank accounts offer distinct features and cater to different preferences. Here are some points of comparison between the two:

- Accessibility: Virtual accounts provide greater accessibility compared to traditional bank accounts. Users can access their virtual accounts 24/7 through online platforms or mobile apps, while traditional bank accounts often require in-person visits during specific branch hours.

- Transaction Speed: Virtual accounts offer faster transaction processing compared to traditional bank accounts. Payments and transfers through virtual accounts are typically processed in real-time, whereas traditional bank transactions may take longer due to manual processing and verification.

- Physical Presence: Traditional bank accounts require a physical presence, as users need to visit a bank branch to open an account, deposit or withdraw funds, and perform certain banking activities. Virtual accounts, on the other hand, operate entirely in the digital realm and do not require physical visits.

- Costs and Fees: Virtual accounts may have lower costs and fees compared to traditional bank accounts. Traditional banks often charge fees for various services, such as monthly account maintenance fees, ATM withdrawal fees, and checkbook fees. Virtual accounts, on the other hand, may have minimal or no fees associated with basic banking activities.

- Account Management: Virtual accounts provide user-friendly interfaces and advanced tools for account management. Users can easily track transactions, set up alerts, and generate reports within their virtual accounts. Traditional bank accounts may offer similar features but may require manual record-keeping and paperwork.

- Personalized Services: Traditional bank accounts often provide personalized services, such as dedicated relationship managers and in-person customer support. Virtual accounts, while offering customer support via online channels, may not provide the same level of face-to-face interaction for more complex banking needs.

- Deposit Insurance: Traditional bank accounts are typically protected by government-backed deposit insurance programs. Virtual accounts may also offer deposit insurance, but users should ensure that the virtual account provider is regulated and offers adequate protection for their funds.

It’s important to consider personal preferences, banking needs, and lifestyle when deciding between virtual accounts and traditional bank accounts. While traditional banks may provide a sense of familiarity and personalized services, virtual accounts offer convenience, accessibility, and cost savings in the digital era.

Now that we have explored the comparison between virtual accounts and traditional bank accounts, let’s move on to discussing some popular virtual account providers.

Virtual Account Providers

With the growing popularity of virtual accounts, several virtual account providers have emerged in the market, offering a range of services and features. Here are a few notable virtual account providers:

- PayPal: PayPal is one of the leading virtual account providers globally, offering a secure and convenient platform for online payments, money transfers, and business transactions. Users can link their bank accounts or credit cards to their PayPal accounts and make seamless transactions with millions of merchants worldwide.

- Revolut: Revolut is a digital banking platform that provides virtual accounts and a range of financial services. Users can open free multi-currency accounts, exchange currencies at competitive rates, and make global transfers with ease. Revolut also offers additional features like budgeting tools, analytics, and cryptocurrency trading.

- N26: N26 is a mobile banking platform that offers virtual accounts along with a powerful app for managing finances. Users can open free bank accounts, make payments, and track their expenses in real-time. N26 also provides additional features like insurance options and investment opportunities.

- TransferWise: TransferWise is renowned for its international money transfer services, allowing users to send and receive funds with low fees and competitive exchange rates. Users can open multi-currency accounts, hold and convert funds, and make global transfers at affordable rates.

- Stripe: Stripe is a popular payment processing platform used by businesses to accept online payments and manage transactions securely. It offers virtual account-like features, allowing businesses to receive payments from customers, manage subscriptions, and handle large-scale payments.

- Skrill: Skrill is an e-wallet service that provides virtual accounts for individuals and businesses. Users can securely send and receive money, make online payments, and access their funds through the Skrill prepaid Mastercard, giving them easy access to their digital wallet.

These are just a few examples of virtual account providers in the market. Each provider offers unique features, services, and pricing structures, so it’s essential to research and compare them to find the one that best suits your specific needs and requirements.

Now that we have explored virtual account providers, let’s summarize the key points discussed in this article.

Conclusion

Virtual accounts have revolutionized the world of banking, providing individuals and businesses with convenient, accessible, and flexible financial management solutions. These digital accounts offer a range of benefits, including 24/7 accessibility, faster transaction processing, cost savings, enhanced security, and streamlined cash management.

Virtual accounts operate entirely in the digital realm, accessible through online platforms or mobile apps. They offer features such as payments, fund transfers, transaction monitoring, and customizable account settings. These accounts are especially popular for online shopping, freelancers, international payments, subscription services, and event management.

When compared to traditional bank accounts, virtual accounts offer greater accessibility, faster transactions, lower costs, advanced account management tools, and the flexibility to adapt to the needs of today’s digital economy. However, traditional banks may still appeal to some individuals who prefer personalized services and face-to-face interactions.

Various virtual account providers have emerged in the market, each with its own set of features and services. PayPal, Revolut, N26, TransferWise, Stripe, and Skrill are just a few examples of virtual account providers offering unparalleled convenience and functionality.

In conclusion, virtual accounts have transformed the way we manage our finances in the digital era. With their convenience, flexibility, and advanced features, virtual accounts are a compelling alternative to traditional banking, empowering individuals and businesses alike to take control of their financial lives.