What Is a Beneficiary in Banking?

A beneficiary in banking refers to an individual or entity who is designated to receive the benefits or proceeds of a financial account or transaction. This designation is commonly used in various banking products such as life insurance policies, retirement accounts, investment accounts, and payable-on-death bank accounts.

When you designate a beneficiary, you are essentially specifying who will inherit or receive the funds or assets in the account upon your death. The beneficiary can be anyone you choose, such as a family member, friend, or charitable organization.

The role of a beneficiary is crucial in banking as it ensures the smooth transfer of assets and avoids complications or disputes after the account holder passes away. By clearly designating a beneficiary, you have control over who will benefit from your financial assets, rather than leaving it to legal processes or the default rules of your financial institution.

It’s worth noting that the concept of a beneficiary extends beyond banking and is commonly used in other areas such as in legal documents like wills and trusts. However, in the context of banking, it specifically refers to the recipient of financial assets or benefits.

Beyond the basic definition, it’s important to understand the different types of beneficiaries and the significance of designating one, as well as the implications of not designating a beneficiary in your banking accounts.

Definition of a Beneficiary

A beneficiary is an individual or entity who is entitled to receive the benefits or assets from a financial account or transaction. In the context of banking, a beneficiary is typically designated by the account holder to inherit or receive the funds in their account upon their death. This designation ensures that the intended person or organization will receive the assets smoothly and according to the account holder’s wishes.

The designation of a beneficiary is an important aspect of financial planning as it allows individuals to have control over the distribution of their assets. By clearly specifying a beneficiary, account holders can ensure that their loved ones or preferred organizations will benefit from their financial resources.

When designating a beneficiary, it is essential to provide accurate and up-to-date information, including the full legal name, contact details, and any specific instructions or conditions for the distribution of assets. This ensures that there is no ambiguity or confusion regarding the recipient of the funds.

The role of a beneficiary extends beyond bank accounts and can also be relevant in other financial arrangements, such as life insurance policies, retirement accounts, and investment accounts. In each case, the beneficiary plays a crucial role in determining where the assets will go upon the account holder’s death.

It is important to note that the designation of a beneficiary is not permanent and can be changed or updated by the account holder at any time, as long as they are of sound mind and have the legal capacity to make such changes. Life events such as births, deaths, marriages, or divorces can prompt updates or changes to the designated beneficiaries.

Having a clear and valid beneficiary designation helps ensure that your assets are distributed according to your wishes and can prevent complications or disputes among family members or other potential claimants. Therefore, it is crucial to review and update your beneficiaries regularly to ensure they accurately reflect your current intentions and circumstances.

Different Types of Beneficiaries

When designating a beneficiary in banking, it’s important to understand that there are different types of beneficiaries, each serving a specific purpose and having certain considerations. Here are some common types of beneficiaries:

Primary beneficiary: The primary beneficiary is the first in line to receive the assets or benefits from the account or policy. This designation takes precedence over any other beneficiary designations.

Contingent beneficiary: Also known as a secondary or alternate beneficiary, the contingent beneficiary is designated to receive the assets or benefits if the primary beneficiary is unable or unwilling to do so. They come into play when the primary beneficiary predeceases the account holder or is otherwise unable to claim the assets.

Revocable beneficiary: A revocable beneficiary is one whose designation can be changed or revoked at any time by the account holder. This provides flexibility and allows for adjustments to reflect changes in circumstances or relationships.

Irrevocable beneficiary: In contrast to a revocable beneficiary, an irrevocable beneficiary designation cannot be changed or revoked without the consent of all parties involved. This type of designation is often used in certain trust arrangements or legal situations where a permanent beneficiary designation is desired.

Multiple beneficiaries: It is also possible to designate multiple beneficiaries to an account or policy. In such cases, the assets or benefits are typically divided according to the specified percentages or proportions among the beneficiaries. It is important to clearly state the allocation to ensure a smooth distribution.

Per stirpes beneficiary: This term is commonly used when designating beneficiaries who are descendants of a deceased individual. If a primary beneficiary is no longer alive, their share will be passed down to their children or other descendants, rather than being equally divided among the remaining living beneficiaries.

These are just a few examples of the different types of beneficiaries that can be designated in banking and financial accounts. It’s important to consider your specific needs and goals when choosing the appropriate beneficiary type for your account or policy.

Importance of Designating a Beneficiary

Designating a beneficiary for your financial accounts is a crucial step in ensuring that your assets are distributed according to your wishes. Here are some key reasons why it is important to designate a beneficiary:

Control and Peace of Mind: By designating a beneficiary, you have control over who will receive your assets after your passing. This provides peace of mind, knowing that your hard-earned money and other financial resources will go to your chosen beneficiaries.

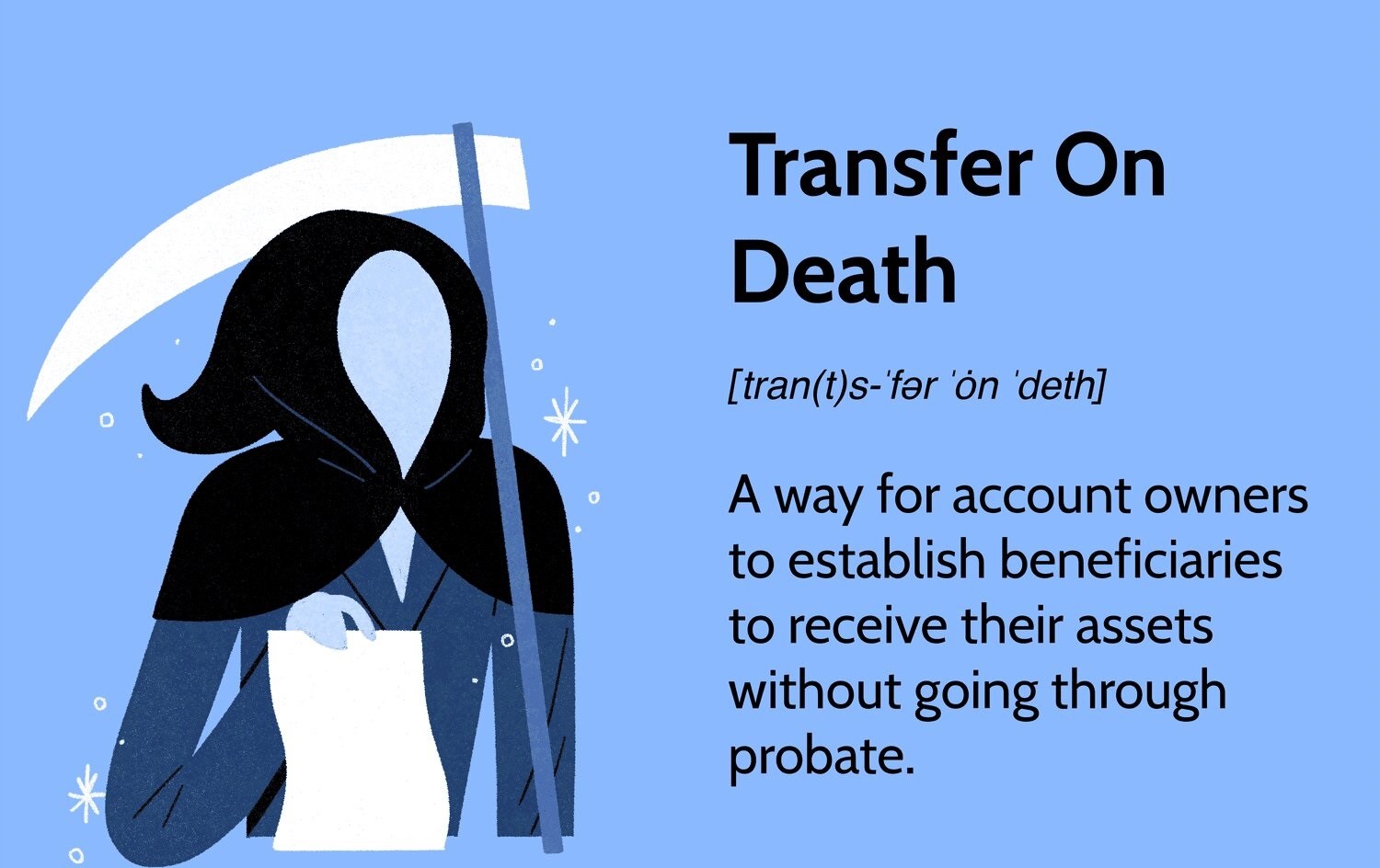

Efficient Asset Distribution: Designating a beneficiary helps to streamline the distribution process. When you pass away, your assets can be transferred directly to the designated beneficiary without going through probate, which can be a lengthy and costly legal process.

Avoidance of Potential Conflicts: Naming a beneficiary can prevent potential conflicts or disputes among family members or other potential claimants. Without a clear designation, there may be disagreements over who should receive the assets, leading to legal battles and strained relationships.

Privacy: When assets pass through probate, the details become a matter of public record. By designating a beneficiary, you can maintain privacy, as the distribution and details of the assets remain confidential.

Continuity and Financial Stability: Designating a beneficiary ensures that there is a seamless transition of assets, allowing your beneficiaries to access funds and maintain financial stability during a potentially difficult time.

Updated Distribution of Assets: Life circumstances may change over time. Designating a beneficiary allows you to easily update your beneficiaries to reflect any changes in your relationships, such as marriages, divorces, births, or deaths.

Protecting Loved Ones: Designating a beneficiary is particularly essential if you have dependents who rely on your financial support. It ensures that they receive the necessary resources to sustain their livelihoods and achieve their goals.

Charitable Giving: If you have a philanthropic goal, designating a charitable organization as a beneficiary allows you to continue supporting causes that are important to you even after your passing.

Overall, the importance of designating a beneficiary in banking cannot be overstated. It provides peace of mind, ensures efficient asset distribution, minimizes conflicts and disputes, protects privacy, and allows for updated and tailored distribution of your assets to loved ones or charitable organizations.

What Happens if You Don’t Designate a Beneficiary?

Failure to designate a beneficiary for your financial accounts can have significant consequences upon your passing. Here’s what may happen if you don’t designate a beneficiary:

Assets Follow Default Rules: When you don’t specify a beneficiary, your assets may be subject to the default rules set by the financial institution or applicable laws. These rules vary depending on the type of account and jurisdiction, but they typically prioritize your legal heirs, such as your spouse, children, or parents.

Probate and Court Involvement: Without a beneficiary designation, your assets may need to go through the probate process. Probate involves having a court validate your will, paying any outstanding debts or taxes, and distributing the remaining assets according to state laws. This can be time-consuming, costly, and may lead to delays in asset distribution, often resulting in additional stress for your loved ones.

Loss of Control: Failing to designate a beneficiary means relinquishing control over who receives your assets. The default rules may not align with your wishes or the specific individuals or organizations you intended to benefit from your assets.

Potential Conflict and Family Disputes: The absence of a clear beneficiary designation can create conflicts and disputes among your surviving family members or potential claimants. Without your guidance, disagreements may arise regarding who should receive the assets, causing strain within the family and potentially leading to costly legal battles.

Delays and Uncertainty: In the absence of a designated beneficiary, financial institutions may require additional documentation or verification to determine the rightful heirs or beneficiaries. This can result in delays and uncertainty regarding the distribution of your assets, leaving your loved ones waiting for access to the funds they may urgently need.

Loss of Privacy: Without a designated beneficiary, the distribution of assets may become a public matter during the probate process. This means that details about your estate, including the value of assets and the beneficiaries, become part of the public record, potentially compromising the privacy of your financial affairs.

It is important to understand the implications of not designating a beneficiary and take proactive steps to avoid these potential pitfalls. By designating a beneficiary, you can maintain control over the distribution of your assets, ensure a smoother and more efficient transfer, and minimize the risk of conflicts or disputes among your loved ones.

How to Add or Change a Beneficiary

Adding or changing a beneficiary for your banking accounts is generally a straightforward process. Here are the general steps to follow:

1. Review Account Terms and Conditions: Start by reviewing the terms and conditions of the specific account or policy to understand the requirements and procedures for adding or changing beneficiaries. Each financial institution may have its own guidelines.

2. Obtain the Necessary Forms: Contact your financial institution, either online or through their customer service, to request the appropriate forms for adding or changing beneficiaries. They may provide you with paper forms to fill out or offer an online portal for this purpose.

3. Gather Required Information: Collect the necessary information about the intended beneficiary, such as their full legal name, contact information, and relationship to you. If you are adding multiple beneficiaries, determine the distribution percentages or proportions.

4. Complete the Forms: Fill out the forms provided by the financial institution accurately and legibly. Provide all required information and follow any instructions or guidelines provided. Ensure that the beneficiary information is correctly entered and double-check for any errors.

5. Submit the Forms: Once you have completed the forms, submit them according to the instructions provided by the financial institution. This could be by mail, fax, or electronically through their online portal. Keep copies of the forms for your records.

6. Confirm the Change: After submitting the forms, it is prudent to follow up with the financial institution to confirm that the changes have been processed and that the new beneficiary designation is in effect. This step will help ensure that your intentions have been properly recorded.

7. Update and Review Regularly: It is important to periodically review and update your beneficiary designations as your circumstances and relationships change. Life events such as marriage, divorce, births, or deaths may prompt the need for updates to reflect your current intentions.

8. Seek Professional Advice: If you have complex financial arrangements or specific legal considerations, it may be beneficial to consult with a financial planner, attorney, or estate planning professional. They can provide guidance on the appropriate steps to take and ensure that your beneficiary designations align with your overall estate planning goals.

Remember, the process of adding or changing beneficiaries may vary slightly depending on the financial institution and the specific account or policy. It is crucial to follow the instructions provided by your bank or financial institution and seek clarification if you have any questions or concerns.

Common Mistakes to Avoid when Designating a Beneficiary

Designating a beneficiary for your banking accounts is a critical step in estate planning. However, it’s important to be aware of common mistakes that people make when designating beneficiaries. By avoiding these mistakes, you can ensure that your assets are distributed according to your wishes. Here are some common mistakes to avoid:

1. Failing to Designate a Beneficiary: One of the most significant mistakes is simply not designating a beneficiary at all. Without a clear designation, your assets may be subject to default rules, potentially leading to delays, disputes, and unintended beneficiaries.

2. Outdated or Incomplete Information: Another common mistake is providing outdated or incomplete information for the designated beneficiary. Ensure that you have accurate and up-to-date contact details, legal names, and other relevant information to avoid any complications or difficulties in asset distribution.

3. Not Reviewing and Updating Beneficiaries: It is essential to periodically review and update your beneficiary designations to align with your current intentions. Failing to do so can result in outdated designations, leaving assets to individuals or organizations that you no longer wish to benefit.

4. Forgetting to Name Contingent Beneficiaries: It’s important to designate contingent beneficiaries, who will receive the assets if the primary beneficiary predeceases you or is unable to claim the assets. By including contingent beneficiaries, you ensure a clear succession plan for your assets.

5. Ignoring Legal and Tax Implications: Designating beneficiaries can have legal and tax implications. It is wise to consult with a financial advisor or estate planning professional to understand the potential implications and optimize your estate plan accordingly.

6. Overlooking Other Accounts and Policies: Many individuals focus solely on bank accounts, neglecting other accounts and policies that also require beneficiary designations, such as life insurance policies, retirement accounts, and investment accounts. Review all your accounts and policies to ensure that beneficiary designations are in place for each relevant one.

7. Assuming Beneficiary Designations Override Other Legal Documents: Keep in mind that beneficiary designations often supersede instructions in other legal documents like wills and trusts. It’s crucial to ensure that beneficiary designations align with your overall estate planning strategy and any instructions provided in other legal documents.

8. Failing to Communicate Intentions: Finally, not communicating your intentions with your designated beneficiaries can lead to surprises, confusion, or even disputes when it comes time for asset distribution. Openly discuss your wishes with your beneficiaries to avoid any misunderstandings or surprises.

By being mindful of these common mistakes and taking proactive steps to avoid them, you can ensure that your beneficiary designations accurately reflect your intentions and help facilitate a smooth transfer of assets to your intended beneficiaries.

Frequently Asked Questions about Beneficiaries in Banking

Here are some frequently asked questions about beneficiaries in banking:

Q: Can I designate multiple beneficiaries for my accounts?

A: Yes, many financial institutions allow you to designate multiple beneficiaries for your accounts. You can specify the percentages or proportions of the assets each beneficiary will receive.

Q: What happens if I want to change my designated beneficiary?

A: You can typically change your designated beneficiary by completing the necessary forms provided by your financial institution. It’s important to keep your beneficiary designations up to date to reflect any changes in your relationships or intentions.

Q: Will my beneficiary be liable for my debts?

A: Generally, beneficiaries are not held liable for the debts of the account holder. However, creditors may be able to claim any assets before they are distributed to the designated beneficiaries. It’s best to consult with a legal professional to understand the specific laws in your jurisdiction.

Q: Can I designate a minor as a beneficiary?

A: While it is possible to designate a minor as a beneficiary, it is advisable to set up a trust or designate a guardian to manage the assets until the minor reaches the age of majority. Consult with an attorney or financial advisor to ensure that you choose the most appropriate option for your situation.

Q: What happens if my designated beneficiary predeceases me?

A: If your primary beneficiary predeceases you, the assets will typically pass to the contingent beneficiary, if one is named. If no contingent beneficiary is named, the assets may be distributed according to the default rules set by the financial institution or state laws.

Q: Can I name a charity or organization as my beneficiary?

A: Yes, you can designate a charitable organization as your beneficiary. Ensure that you have the correct legal name and any necessary identification numbers for the organization.

Q: Do I need an attorney to designate a beneficiary?

A: In most cases, you do not need an attorney to designate a beneficiary for your banking accounts. However, if you have complex estate planning needs or specific legal considerations, consulting with an attorney or financial advisor can provide valuable guidance.

Q: How often should I review my beneficiary designations?

A: It is advisable to review your beneficiary designations periodically and after any major life events. This can include marriage, divorce, births, deaths, or any other significant changes in your personal or financial circumstances.

Q: Can I designate a trust as my beneficiary?

A: Yes, it is possible to designate a trust as your beneficiary. This can provide more control and flexibility in distributing the assets according to your wishes. Ensure that you work with an attorney to properly establish the trust and designate it as the beneficiary.

Q: What happens if I don’t designate a beneficiary for my accounts?

A: If you don’t designate a beneficiary, the assets may be subject to default rules set by the financial institution or state laws. This can lead to delays, additional costs, and potential disputes among family members or other claimants.

Remember, it’s important to consult with a financial advisor or attorney to understand the specific laws and regulations applicable to beneficiary designations in your jurisdiction and to tailor your decisions to your individual circumstances.

Conclusion

Designating a beneficiary in banking is a crucial step in estate planning and ensuring the smooth transfer of your assets. By understanding the definition of a beneficiary, the different types of beneficiaries, and the importance of designating one, you can take proactive measures to protect your financial interests and the well-being of your loved ones.

Adding or changing a beneficiary involves a straightforward process of reviewing account terms, obtaining the necessary forms, and providing accurate information. It’s essential to periodically review and update your beneficiaries to reflect any changes in your relationships or intentions.

By avoiding common mistakes such as failing to designate a beneficiary, providing outdated information, or overlooking legal and tax implications, you can prevent potential complications and ensure that your assets are distributed according to your wishes.

Frequently asked questions shed light on common queries about beneficiaries in banking, such as designating multiple beneficiaries, changing beneficiaries, liability for debts, and designating minors or charitable organizations as beneficiaries. It’s important to stay informed and consult with professionals when needed.

In conclusion, taking the necessary steps to designate and maintain beneficiaries for your banking accounts plays a crucial role in effective estate planning. By carefully considering your choices and keeping them up to date, you can have the peace of mind that your assets will be distributed according to your wishes and provide financial stability for your loved ones in the future.