Introduction

Welcome to the world of ACH banking! Whether you’re a business owner or a curious individual, understanding how ACH banking works can greatly benefit you. ACH, which stands for Automated Clearing House, is a system that allows electronic funds transfers between banks in the United States.

With the rise of online banking and digital payments, ACH has become an essential part of our financial infrastructure. It enables seamless transactions, making it easier to send and receive money electronically, replacing the need for physical checks and cash transactions.

In this article, we will delve into the world of ACH banking and explore how it works, the benefits and drawbacks, ACH payment types, common uses, security measures, and the future outlook of this payment system.

So, whether you’re considering implementing ACH into your business operations or you’re simply interested in learning more about this popular payment method, read on to gain a comprehensive understanding of ACH banking and its impact in today’s digital age.

What is ACH Banking?

ACH banking, or Automated Clearing House banking, refers to the electronic payment system that facilitates the transfer of funds between different bank accounts. This system operates in the United States and allows businesses and individuals to send and receive money securely and efficiently, eliminating the need for physical checks or cash.

The ACH network acts as a central hub that processes a large volume of transactions every day. It connects various financial institutions, such as banks and credit unions, and enables the transfer of funds between them. This system has gained popularity due to its convenience, reliability, and cost-effectiveness.

How does ACH banking work? When a sender initiates an ACH payment, the funds are electronically debited from their bank account and then transmitted through the ACH network to the recipient’s bank account. The process involves several steps, including authorization, verification, and settlement.

One of the key features of ACH banking is its batch processing capability. Instead of processing transactions individually, ACH batches multiple transactions together, reducing processing time and costs. Batches are typically submitted at specific times throughout the day, and the transactions within the batch are consolidated and sent for processing as a group.

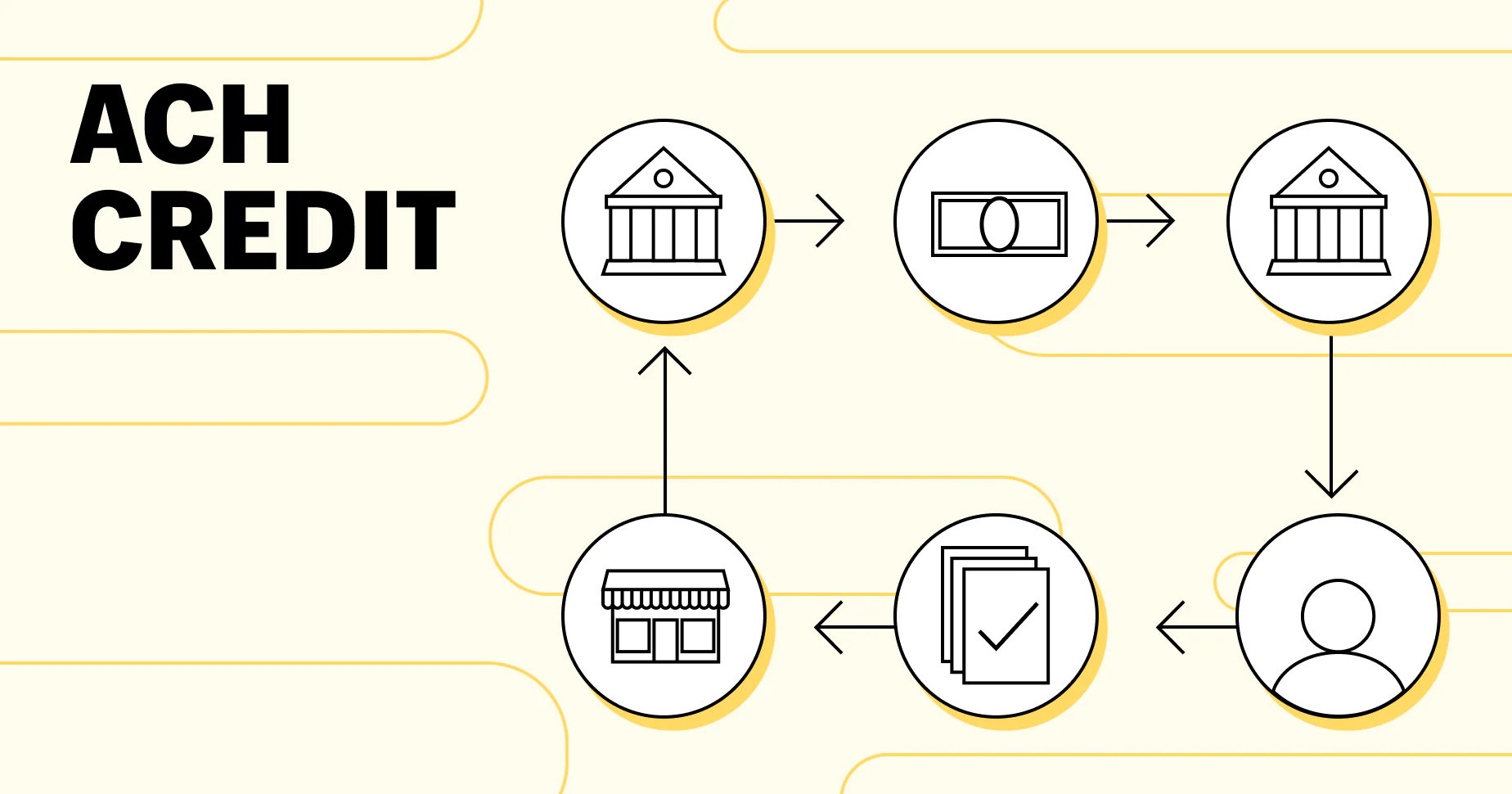

It’s worth noting that ACH banking supports both credit and debit transactions. A credit transaction occurs when funds are deposited into an account, while a debit transaction involves the withdrawal of funds. This versatility allows businesses and individuals to choose the most suitable option based on their specific needs.

Overall, ACH banking provides a secure and efficient way to transfer funds electronically. It has become a fundamental part of the modern banking system, streamlining financial transactions and reducing reliance on traditional paper-based methods. Whether you’re a business owner or an individual looking to simplify your financial transactions, ACH banking offers a reliable solution that saves time and money.

How Does ACH Banking Work?

ACH banking operates through a systematic process that ensures the secure transfer of funds between different bank accounts. Understanding how ACH banking works can help you navigate the world of electronic transactions with ease.

The process begins with the sender initiating an ACH transaction, whether it’s an individual making a payment or a business processing payroll for its employees. The sender provides their bank with instructions to initiate an ACH transaction, including the recipient’s bank account information, the amount to be transferred, and any additional details required.

Once the transaction is initiated, it goes through a series of steps within the ACH network to ensure its smooth processing:

- Authorization: Before the ACH payment can take place, the sender must have proper authorization from the recipient to initiate the transaction. This may involve obtaining consent or providing a signed agreement, depending on the nature of the transaction.

- Verification: The sender’s bank verifies the account information and availability of funds to ensure a successful transfer. This process helps prevent errors or insufficient fund situations.

- Batch Processing: ACH transactions are grouped into batches for more efficient processing. Throughout the day, banks collect and consolidate multiple transactions, which are then submitted to the ACH network at specific times.

- Routing: Once the batch of transactions is submitted, the ACH network routes the payments to the appropriate receiving banks based on the account information provided by the sender.

- Validation: The recipient’s bank validates the account information and verifies the availability of funds. This step ensures that the recipient receives the payment accurately and in a timely manner.

- Settlement: Finally, the settlement process occurs, where the funds are transferred from the sender’s bank to the recipient’s bank. This step completes the ACH transaction, and the funds become available in the recipient’s account.

It’s important to note that the timing of ACH transactions can vary. While same-day ACH processing is available for certain transactions, others may take a few business days to complete. Factors such as weekends, holidays, and cut-off times can impact the speed of the transaction.

Overall, ACH banking offers a streamlined and secure method for transferring funds electronically. The systematic process ensures the accuracy and efficiency of transactions, making it a reliable choice for individuals and businesses alike.

Benefits of ACH Banking

ACH banking offers a wide range of benefits for businesses and individuals alike. By utilizing this electronic funds transfer system, you can enjoy the following advantages:

- Convenience: ACH banking eliminates the need for physical checks, reducing the hassle of writing, mailing, and depositing paper checks. With ACH transfers, you can initiate transactions directly from your computer or mobile device, making it incredibly convenient and time-saving.

- Cost-effectiveness: ACH transactions are typically more cost-effective compared to other payment methods, such as wire transfers or credit card processing. With lower transaction fees and batch processing capabilities, businesses can save on processing costs, especially when dealing with a high volume of transactions.

- Security: ACH banking is built on a secure network, protecting your financial information throughout the transaction process. Encryption technologies and authentication methods ensure that sensitive data remains confidential, safeguarding against unauthorized access and fraud.

- Efficiency: ACH transactions are processed quickly, enabling faster settlement times compared to traditional paper-based methods. This efficiency is particularly beneficial for businesses managing payroll, recurring payments, or managing cash flow.

- Automation: ACH banking allows for automated payments and collections, reducing the need for manual intervention. Businesses can set up recurring payments for regular expenses, such as rent or utility bills, streamlining their financial operations.

- Wider Reach: ACH banking enables the transfer of funds between different banks, expanding your reach to recipients across the United States. This broader accessibility makes it easier to conduct business and manage transactions with customers and suppliers nationwide.

- Environmentally Friendly: By reducing the reliance on paper checks and physical documentation, ACH banking contributes to environmental sustainability. It helps minimize paper waste, carbon emissions from transportation, and energy consumption associated with paper-based payment processes.

Whether you’re a business owner seeking cost savings and efficiency or an individual looking for a secure and convenient way to manage your finances, ACH banking provides a multitude of benefits. Embracing this electronic payment system can enhance your financial operations and simplify your day-to-day transactions.

Drawbacks of ACH Banking

While ACH banking offers numerous benefits, it’s important to consider some of the drawbacks associated with this payment system:

- Processing Time: ACH transactions may take time to process, especially when compared to other payment methods such as wire transfers. While same-day ACH is available for certain transactions, others can take a few business days to complete. This delay in processing may not be ideal for time-sensitive payments or urgent financial transactions.

- Transaction Limits: Some institutions impose limits on the amount that can be transferred through ACH banking. These limits can vary depending on the banks involved, and exceeding the limit may require alternative payment methods. It’s important to be aware of your bank’s transaction limits to ensure they meet your needs.

- Authorization Requirements: ACH transactions require proper authorization from both the sender and the recipient. This can involve obtaining consent or signing agreements, which may add an extra layer of administrative work and potential delays in initiating transactions.

- Disputed Transactions: In situations where a transaction is disputed, the resolution process for ACH transactions can be complex and time-consuming. Resolving disputes may involve contacting multiple parties, providing supporting documentation, and waiting for a resolution, which can cause inconvenience and delay in accessing funds.

- Cut-Off Times: Banks have cut-off times for submitting ACH transactions, typically on business days. Transactions initiated after the cut-off time may be processed on the next business day, resulting in a delay in the transfer of funds. It’s essential to be aware of your bank’s cut-off times to ensure timely processing of your transactions.

- Potential for Errors: While ACH transactions are generally secure, there is still a possibility of human error or technical glitches. Incorrect bank account details, incorrect amounts, or system malfunctions can lead to failed or delayed transactions. It’s crucial to double-check all transaction details before initiating an ACH payment.

While these drawbacks exist, they are outweighed by the advantages of ACH banking for most individuals and businesses. It’s important to be aware of these potential limitations and take them into account when considering ACH as a payment method.

ACH Payment Types

ACH banking supports various payment types, offering flexibility for different financial transactions. Understanding the different types of ACH payments can help you choose the most appropriate method for your specific needs:

- Direct Deposit: Direct deposit is one of the most common ACH payment types. It involves electronically depositing funds directly into an individual’s bank account, typically used for payroll purposes. Employers can deposit employees’ salaries, bonuses, and reimbursements through this method, providing convenience and security for both parties.

- Direct Payment: Direct payment, also known as ACH debit, allows businesses or individuals to withdraw funds directly from a customer’s bank account. This method is commonly used for recurring payments, such as utility bills, subscription services, or loan repayments. With the customer’s authorization, the funds are debited from their account, streamlining payment collections and reducing the need for paper checks.

- Person-to-Person Payments: ACH banking facilitates person-to-person (P2P) payments, enabling individuals to transfer funds electronically to friends, family, or acquaintances. P2P payments have gained popularity with the rise of digital wallets and peer-to-peer payment apps. This method offers a convenient and secure way to split bills, repay debts, or send money to loved ones.

- B2B Payments: Business-to-business (B2B) payments via ACH are common for companies conducting transactions with other businesses. This method allows for efficient and secure payment processing between parties, eliminating the need for physical checks or wire transfers. B2B payments through ACH are particularly useful for recurring payments, invoices, supply chain transactions, and vendor payments.

- E-commerce Payments: ACH payments can also be used for online transactions, providing an alternative to credit card payments. E-commerce businesses can offer ACH as a payment option, allowing customers to pay directly from their bank accounts. This method provides convenience, security, and cost savings for both merchants and customers.

- Government Payments: ACH banking is widely used for various government payments, such as tax refunds, social security benefits, and veterans’ benefits. This electronic payment method ensures timely and secure delivery of funds to eligible recipients, eliminating the need for paper checks and reducing administrative costs.

Each ACH payment type offers distinct advantages depending on the specific transaction requirements. Whether you’re an employer managing payroll, a business collecting payments, or an individual making personal transfers, ACH banking provides flexible payment options to suit your needs.

Common Uses of ACH Banking

ACH banking has become widely adopted in various industries and everyday financial transactions. Its versatility and efficiency have made it a preferred method for several common applications:

- Payroll Processing: Many businesses rely on ACH banking for processing their employee payrolls. Direct deposit allows employers to deposit salaries, bonuses, and other compensation directly into employees’ bank accounts. This method eliminates the need for paper checks and provides a convenient and secure way to distribute funds to employees.

- Bill Payments: ACH banking is commonly used for bill payments, both for individuals and businesses. Whether it’s utility bills, mortgage payments, credit card bills, or recurring subscription fees, ACH payment options are often available. This offers a convenient and cost-effective alternative to traditional check payments or credit card transactions.

- Vendor Payments: Businesses often use ACH banking for vendor payments and supplier relationships. By setting up direct payments through ACH, companies can streamline their accounts payable processes, ensuring timely and accurate payments to their vendors. This helps maintain positive business relationships and simplifies financial management.

- Online Purchases: ACH banking has made its way into the e-commerce world as an alternative to credit card payments. Online retailers may offer ACH payment options, allowing customers to pay directly from their bank accounts. This provides a secure and convenient payment method, especially for recurring purchases or larger transactions.

- Charitable Contributions: Non-profit organizations often rely on ACH banking to process charitable contributions. Donors can set up recurring donations or make one-time gifts via ACH transactions. This method provides a seamless and cost-effective way for individuals to support their favorite causes.

- Tax Payments and Refunds: ACH banking is extensively used by individuals and businesses for tax-related transactions. Taxpayers can make electronic tax payments to the IRS through the Electronic Federal Tax Payment System (EFTPS). Similarly, when taxpayers are due tax refunds, the IRS can deposit the funds directly into their bank accounts using ACH.

- Insurance Premiums: ACH payments are commonly utilized for insurance premium payments. Policyholders can authorize insurers to deduct premiums directly from their bank accounts, providing a seamless and automated payment process. This helps policyholders ensure that their coverage remains in effect without the hassle of manual payments.

These are just a few examples of the common uses of ACH banking. Its widespread adoption across various industries demonstrates its reliability, cost-effectiveness, and efficiency in facilitating electronic transactions and simplifying financial processes.

ACH Banking vs. Wire Transfers

When it comes to transferring funds electronically, two common methods that often come to mind are ACH banking and wire transfers. While both serve the purpose of transferring money, there are significant differences between the two:

Speed: One of the primary distinctions between ACH banking and wire transfers is the speed of transactions. Wire transfers are typically faster, with funds being transferred in real-time or within a few hours. On the other hand, ACH banking transactions may take longer, ranging from one to three business days for standard processing. Same-day ACH options are available for certain transactions, but it still takes longer compared to wire transfers.

Cost: Wire transfers often incur higher fees compared to ACH banking. Wire transfer fees can vary depending on the financial institutions involved and the destination of the funds. In contrast, ACH banking fees are generally lower, making it a more cost-effective option, especially for businesses processing a high volume of transactions.

Transaction Limits: Wire transfers typically allow for higher transaction limits compared to ACH banking. This makes wire transfers more suitable for larger transactions, such as international transfers or significant business transactions. ACH banking often has lower transaction limits, making it more suitable for everyday payments, payroll processing, bill payments, and smaller business transactions.

Security: Both ACH banking and wire transfers utilize secure systems to protect sensitive financial information. However, wire transfers are often considered more secure due to their real-time processing and stringent authentication measures. ACH transactions, while secure, may carry a slightly higher risk as they are processed in batches and not in real-time.

Use Cases: ACH banking is commonly used for regular payments, direct deposits, bill payments, and other routine financial transactions. It is favored for its convenience, cost-effectiveness, and efficiency in handling these types of transactions. Wire transfers, on the other hand, are typically used for urgent or high-value transfers, international transactions, real estate transactions, or large business transactions that require immediate settlements.

When deciding between ACH banking and wire transfers, it is essential to consider the specific requirements of your transaction. Factors such as speed, cost, transaction limits, security, and use case will guide you in choosing the most suitable method for your needs.

ACH Processing Time

ACH processing time refers to the duration it takes for an ACH transaction to complete, from initiation to settlement. While ACH banking offers a convenient way to transfer funds electronically, it’s important to understand that the processing time can vary depending on several factors:

Type of Transaction: The type of ACH transaction being processed can impact the processing time. Standard ACH transactions, such as payroll deposits or bill payments, typically take one to three business days for settlement. Same-day ACH options are available for certain transactions, allowing for faster processing and settlement within the same business day.

Cut-Off Times: Each financial institution has specific cut-off times for submitting ACH transactions. Transactions initiated before the cut-off time are often processed on the same business day, while those initiated after the cut-off time may be processed on the next business day. Cut-off times can vary between institutions, so it’s essential to know your bank’s specific deadline to ensure timely processing.

Weekends and Holidays: ACH processing time is influenced by weekends and holidays. Transactions initiated on weekends or federal holidays are typically processed on the next business day. This means that if you initiate an ACH transfer on a Friday evening, it may not be processed until Monday or the next business day. It’s important to consider these non-business days when estimating the processing time of your ACH transactions.

Transaction Volume: The volume of ACH transactions being processed can impact the overall processing time. Higher transaction volumes or peak times may result in longer processing times, especially if the ACH network experiences high traffic. However, the batch processing nature of ACH transactions allows financial institutions to consolidate multiple transactions for more efficient processing.

Transaction Verification: Before an ACH transaction can be settled, the sender’s bank and the recipient’s bank must verify the transaction details, account information, and the availability of funds. This verification process adds an additional layer of security but may also contribute to the overall processing time of the transaction.

It’s important to keep these factors in mind when considering the processing time of your ACH transactions. If time sensitivity is crucial, it may be necessary to explore alternative options like wire transfers or same-day ACH services. However, for non-urgent transactions, ACH banking offers a cost-effective and convenient method for electronic fund transfers.

ACH Authorization and Security

ACH banking prioritizes the security and integrity of financial transactions to ensure the confidentiality and protection of sensitive information. ACH authorization and security measures are in place to safeguard the transfer of funds and to prevent unauthorized access or fraudulent activities. Here are the key aspects of ACH authorization and security:

Authorization: ACH transactions require proper authorization from both the sender and the recipient. The sender must obtain consent or provide a signed agreement from the recipient to initiate the transaction. This ensures that both parties are aware of and approve the electronic transfer of funds. Authorization forms may include details such as the amount of the transaction, frequency of payments, and any additional instructions necessary for successful processing.

Authentication: ACH banking relies on various authentication measures to verify the identity of the sender and protect against unauthorized access. Financial institutions implement security protocols such as usernames, passwords, PINs, and security questions to authenticate users accessing online banking platforms. Multi-factor authentication, which requires a combination of two or more identification factors, adds an extra layer of security to ACH transactions.

Encryption: ACH banking employs encryption technologies to encode sensitive data during transmission. Secure Socket Layer (SSL) and Transport Layer Security (TLS) protocols are commonly used to establish secure connections between financial institutions and their customers. These encryption methods ensure that confidential information, including bank account details and transaction data, remains encrypted and protected from unauthorized interception or tampering.

Fraud Detection and Prevention: Financial institutions utilize sophisticated fraud detection systems to identify and prevent fraudulent ACH transactions. These systems monitor transaction patterns, account activity, and other parameters to detect any suspicious or unusual behavior. Real-time monitoring and analysis enable rapid identification of potential fraudulent activities, minimizing any financial losses and protecting the integrity of the ACH network.

Regulatory Compliance: ACH banking is subject to stringent regulatory guidelines and compliance standards to ensure the security and protection of financial transactions. Organizations involved in ACH processing, including financial institutions and payment processors, adhere to industry best practices and comply with regulations such as the National Automated Clearing House Association (NACHA) rules. Compliance with these regulations helps maintain the security and integrity of ACH transactions.

By implementing robust authorization and security measures, ACH banking provides a secure environment for electronic fund transfers. However, it’s important for individuals and businesses to remain vigilant and follow recommended security practices, such as keeping login credentials confidential, regularly monitoring account activity, and promptly reporting any suspicious transactions to their financial institution.

The Future of ACH Banking

The future of ACH banking looks promising, with continued advancements and innovations that will further enhance the efficiency and convenience of electronic fund transfers. Here are some key trends and developments that are shaping the future of ACH banking:

Real-Time Payments: Real-time payments are gaining momentum in the ACH banking landscape. Initiatives such as the RTP® (Real-Time Payments) network are enabling the transfer of funds in real-time, 24/7. Real-time payments offer immediate availability of funds, providing businesses and individuals with faster access to their money and helping expedite transactions in a rapidly evolving digital economy.

API Integration: Application Programming Interface (API) integration is revolutionizing the way financial institutions and businesses interact with ACH banking. APIs allow for secure and seamless integration between systems, enabling faster onboarding, transaction processing, and enhanced data exchange. API integration facilitates smoother integration of ACH banking into various platforms and applications, resulting in a more streamlined and efficient user experience.

Mobile Payments: With the increasing adoption of smartphones and mobile payment apps, ACH banking is expected to further evolve in the realm of mobile payments. Mobile wallets and peer-to-peer payment apps already leverage ACH infrastructure to facilitate instant money transfers between individuals. The convenience and accessibility of mobile payments are likely to drive further innovation, leading to enhanced ACH mobile payment capabilities.

Enhanced Security Measures: As digital threats continue to evolve, ACH banking will prioritize the implementation of advanced security measures. Biometric authentication, such as fingerprint or facial recognition, may become more prevalent in ACH banking to provide enhanced security and mitigate the risk of unauthorized access or fraud. Additionally, artificial intelligence and machine learning technologies will play a crucial role in identifying potential fraudulent activities and enhancing fraud prevention measures.

International ACH: While ACH banking primarily facilitates domestic transactions, there is growing interest in expanding its capabilities for international transfers. Initiatives like the Global ACH Network aim to establish interoperability between different countries’ ACH systems, allowing for seamless cross-border transactions. The development of international ACH capabilities would provide businesses with cost-effective and efficient alternatives to traditional wire transfers for global payments.

Regulatory Innovations: Regulatory bodies continue to refine and update regulations governing ACH banking to adapt to technological advancements and changing needs. These regulatory innovations aim to strike a balance between security and convenience, ensuring that ACH transactions remain safe and efficient while fostering innovation and competition in the financial industry.

The future of ACH banking holds considerable potential for transforming the way we conduct financial transactions and manage our money. With ongoing technological advancements, expanding service offerings, and evolving regulatory frameworks, ACH banking is poised to continue revolutionizing electronic payments and empowering businesses and individuals with secure, efficient, and convenient financial solutions.

Conclusion

ACH banking has revolutionized the way we transfer funds electronically, providing a secure, efficient, and cost-effective method for individuals and businesses to manage their financial transactions. With its simplified processing, convenience, and wide range of applications, ACH banking has become an integral part of our modern financial infrastructure.

Throughout this article, we explored the various aspects of ACH banking, including its definition, functionality, benefits, drawbacks, and common uses. We learned that ACH banking offers numerous advantages, such as convenience, cost-effectiveness, and streamlined operations. From payroll processing and bill payments to vendor transactions and online purchases, ACH banking offers flexible and reliable solutions for a variety of financial needs.

While ACH banking provides many benefits, it’s important to consider factors such as processing time, transaction limits, and security measures when choosing this payment method. Understanding the differences between ACH banking and wire transfers can help determine the most suitable option for your specific transaction requirements.

Looking ahead, the future of ACH banking is promising, with ongoing advancements in real-time payments, API integration, mobile payments, and enhanced security measures. As technology continues to evolve, ACH banking will further adapt to meet the changing needs of businesses and individuals, offering faster and more convenient ways to transfer funds and manage financial transactions.

In conclusion, ACH banking has redefined the way we handle electronic funds transfers. It has improved efficiency, reduced costs, and provided a secure and convenient alternative to traditional payment methods. By embracing and understanding the capabilities of ACH banking, businesses and individuals can harness its benefits to streamline financial operations and simplify transactions in the digital age.