Introduction

Welcome to the digital age, where technology continues to revolutionize every aspect of our lives. Among the various advancements, blockchain technology has emerged as a game-changer, promising significant benefits across various industries. But what exactly is blockchain? Why is it gaining so much attention? And why is it important?

Blockchain technology is a decentralized ledger system that records and verifies transactions across multiple computers. It was first introduced as the underlying technology for cryptocurrencies like Bitcoin. However, its potential applications extend far beyond digital currencies. Blockchain offers a secure, transparent, and efficient way to validate and store information, making it a transformative technology with wide-ranging implications.

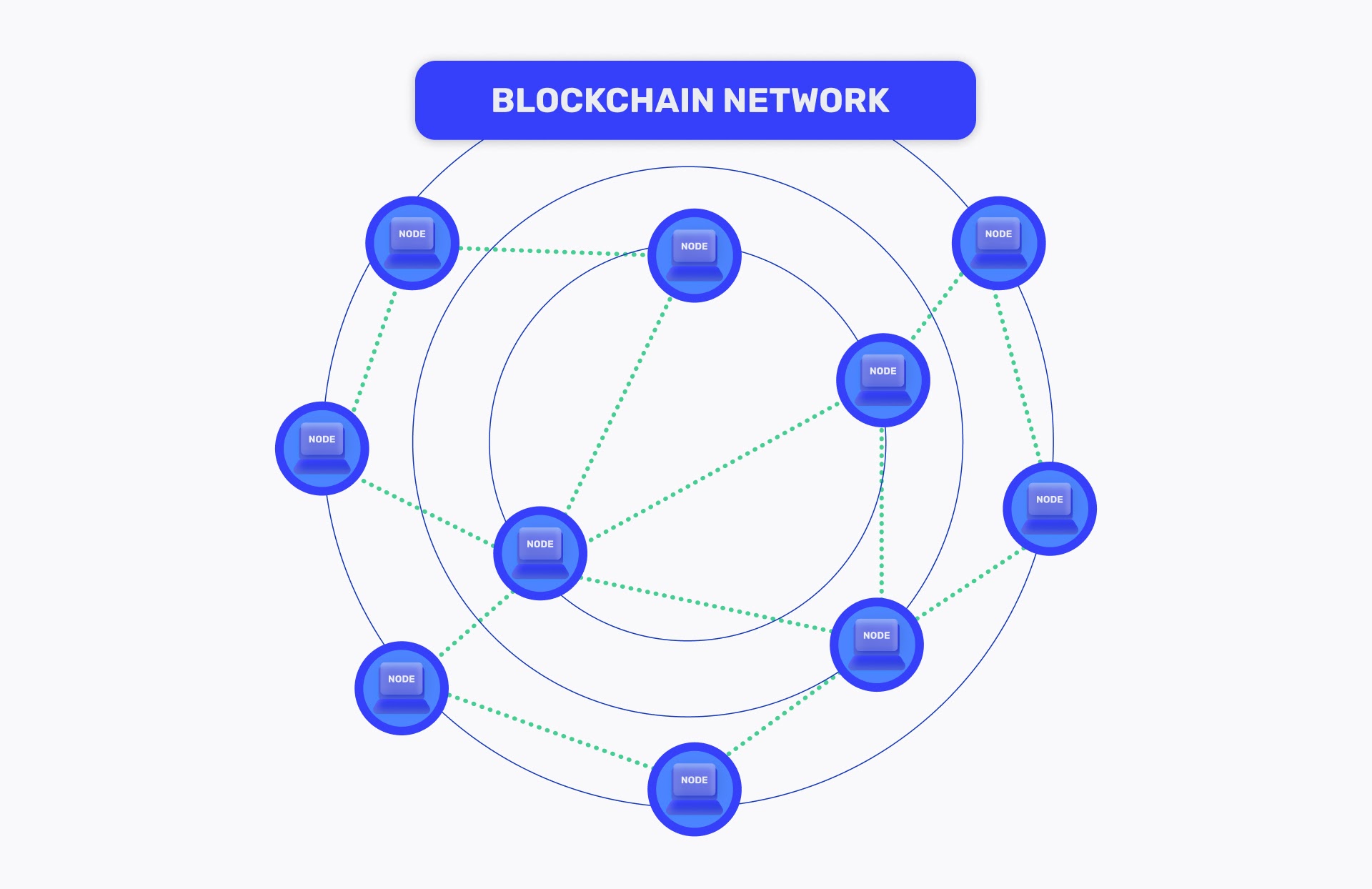

Understanding how blockchain works is crucial to grasp its importance. In a blockchain network, each transaction is grouped into a block, which is added to a chain of previous blocks. This chain is continuously updated and maintained by a network of computers, known as nodes, ensuring that all participants have a consistent and tamper-proof view of the transactions. This decentralized nature eliminates the need for intermediaries, such as banks or government institutions, resulting in greater efficiency, cost savings, and increased trust.

The importance of blockchain technology lies in its ability to address several critical challenges that exist in traditional systems. One of the key advantages is enhanced security and privacy. Unlike centralized databases, where a single point of failure can lead to data breaches, blockchain uses advanced cryptographic algorithms to secure data. Each transaction is encrypted and linked to the previous transaction, creating an immutable record that is nearly impossible to alter or tamper with. This immutability and transparency foster trust and credibility, making blockchain highly desirable for applications that require secure and private data storage.

In addition to security, blockchain technology has the potential to eliminate intermediaries and reduce costs. Traditional processes often involve numerous intermediaries, each adding their fees and delays to the transaction. With blockchain, transactions can be conducted directly between parties, cutting out unnecessary intermediaries and reducing costs and processing time. This is particularly impactful for cross-border transactions, where the involvement of multiple intermediaries can result in high fees and significant delays.

The transparency and traceability provided by blockchain technology are also key factors in its importance. Every transaction on the blockchain is visible to all participants, creating a transparent and auditable system. This level of transparency can be invaluable in industries such as supply chain management, where tracking the origin and movement of goods is crucial. With blockchain, stakeholders can have real-time visibility into the entire supply chain, reducing fraud, counterfeiting, and ensuring ethical sourcing practices.

What is Blockchain Technology?

Blockchain technology is a revolutionary concept that has gained immense popularity in recent years. At its core, blockchain is a decentralized digital ledger that records and verifies transactions. It was initially developed as the underlying technology for cryptocurrencies like Bitcoin, but its potential applications extend far beyond digital currencies.

At its most basic level, a blockchain can be viewed as a chain of blocks, with each block containing a list of transactions. These transactions are securely and permanently recorded in a chronological order. The unique feature of blockchain technology lies in its decentralized nature. Unlike traditional systems where a central authority controls and manages the ledger, blockchain operates on a distributed network of computers or nodes. This network collaboratively maintains and updates the blockchain, ensuring that all participants have an identical copy of the ledger.

The process of adding new transactions to the blockchain involves a validation mechanism known as consensus. Various consensus algorithms, such as Proof of Work (PoW) or Proof of Stake (PoS), are used to ensure that the transactions are validated and added to the blockchain in a secure and trustless manner. Once a block is added to the chain, it becomes an immutable part of the blockchain that cannot be altered without consensus from the network.

One of the fundamental characteristics of blockchain technology is its transparency. All transactions recorded on the blockchain are visible to all participants, providing a high level of transparency and accountability. This transparency is particularly valuable in industries such as finance, supply chain management, and healthcare, where secure and transparent recordkeeping is crucial.

In addition to transparency, blockchain technology offers enhanced security. Each transaction on the blockchain is secured using advanced cryptographic techniques. The use of cryptographic hash functions ensures that the data stored in each block is protected and tamper-proof. Furthermore, the decentralized nature of blockchain makes it exceedingly difficult for hackers or malicious actors to manipulate the data or launch cyber attacks.

How Does Blockchain Technology Work?

Blockchain technology operates on a complex and secure system that allows for decentralized and transparent recordkeeping. Understanding how blockchain works is essential to comprehend its potential and importance in various industries.

At the core of blockchain technology is the concept of a distributed ledger. A distributed ledger is a database that is shared and maintained by multiple participants or nodes in a network. Each node has a copy of the entire blockchain, ensuring that all participants have the same version of the ledger.

To add a new transaction to the blockchain, several steps take place:

- Transaction Creation: A user initiates a transaction by creating a digital record that specifies the details, such as the sender, recipient, and transaction amount.

- Transaction Verification: The transaction is broadcasted to the network of nodes. Each node validates the transaction’s authenticity and ensures that the sender has sufficient funds or authority to execute the transaction.

- Block Formation: Verified transactions are grouped together to form a block. Each block contains a unique identifier called a hash, which is generated by applying cryptographic algorithms to the transactions’ data.

- Consensus Mechanism: The network of nodes works collectively to agree on the validity of the block. Consensus mechanisms, such as Proof of Work (PoW) or Proof of Stake (PoS), ensure that the majority of the network agrees on the integrity of the block before it is added to the chain.

- Block Addition: Once consensus is reached, the block is added to the existing chain. The hash of the new block is linked to the previous block’s hash, creating a chronological chain of blocks.

One of the key features of blockchain technology is its immutability. Once a block is added to the chain, it cannot be altered or deleted without consensus from the network. This makes the blockchain highly secure and tamper-evident, as any attempt to modify a block would require altering all subsequent blocks, which is computationally infeasible.

Furthermore, the decentralized nature of blockchain technology adds an extra layer of security. Unlike centralized systems that rely on a single point of control, blockchain is distributed across multiple nodes. This means that even if a few nodes are compromised, the integrity of the entire blockchain remains intact.

Overall, blockchain technology offers a transparent, secure, and tamper-proof system for recording and verifying transactions. By leveraging cryptographic techniques and distributed consensus, blockchain has the potential to revolutionize various industries and redefine the way we conduct transactions and store data.

The Importance of Blockchain Technology

Blockchain technology holds immense importance and has the potential to reshape various industries in profound ways. Its significance can be attributed to several key factors that make it a game-changer in the digital era.

Enhanced Security and Privacy: One of the primary advantages of blockchain technology is its ability to provide enhanced security and privacy. The decentralized nature of blockchain, coupled with advanced cryptographic techniques, ensures that the data stored on the blockchain is highly secure and resistant to tampering. Transactions on the blockchain are encrypted and linked to previous transactions, creating an immutable and transparent record. This level of security is particularly relevant in industries such as finance, healthcare, and supply chain management, where trust and privacy are paramount.

Eliminating Intermediaries and Reducing Costs: Traditional processes often involve intermediaries such as banks, financial institutions, or legal entities. These intermediaries not only introduce complexity and delays but also add significant costs to transactions. With blockchain technology, transactions can be conducted directly between parties, eliminating the need for intermediaries. This direct peer-to-peer interaction reduces costs, streamlines processes, and improves efficiency. It is especially beneficial in cross-border transactions, where intermediaries can cause delays and incur high fees.

Transparency and Traceability: Blockchain offers unparalleled transparency and traceability. Every transaction recorded on the blockchain is visible to all participants in the network. This transparency fosters trust and accountability, as all stakeholders can independently verify the validity of transactions. In industries such as supply chain management, blockchain ensures that the movement of goods is transparently tracked from the point of origin to the final destination. This can help prevent fraud, counterfeiting, and unethical practices, ensuring ethical sourcing and product authenticity.

Improved Efficiency and Speed: Blockchain technology enables faster and more efficient transactions. The removal of intermediaries and the ability to automate processes through smart contracts minimize delays and human errors. Additionally, the decentralized nature of blockchain eliminates the need for centralized recordkeeping and reconciliation, significantly reducing administrative overhead and enhancing operational efficiency. This speed and efficiency can have a transformative effect on industries such as finance, where settlement times can be reduced from days to minutes.

Decentralization and Resilience: The decentralized nature of blockchain technology contributes to its importance. Unlike centralized systems that are vulnerable to single points of failure or cyber attacks, blockchain is distributed across multiple nodes. This decentralization ensures that even if some nodes go offline or are compromised, the network remains operational and the data remains secure. This resilience and fault tolerance are critical in industries where system downtime or data loss can have severe consequences.

Overall, the importance of blockchain technology lies in its potential to revolutionize industries by providing enhanced security, eliminating intermediaries, fostering transparency, improving efficiency, and offering resilience. As more businesses and organizations recognize the benefits of blockchain, its applications will continue to expand, leading to a future where blockchain becomes an integral part of our digital infrastructure.

Enhanced Security and Privacy

In an increasingly digital world, security and privacy are of paramount importance. Blockchain technology offers enhanced security and privacy features that make it a highly desirable solution for businesses and individuals alike.

Immutable and Tamper-Proof Record: One of the key security benefits of blockchain is its immutability. Once a transaction is recorded on the blockchain, it becomes a permanent part of the ledger and cannot be altered or deleted without the consensus of the network. Each transaction is linked to the previous transaction through cryptographic hashes, creating an interdependent chain of blocks. This chain of blocks ensures that any attempted tampering with a transaction would require altering all subsequent blocks, making it virtually impossible to manipulate data or commit fraudulent activities without being detected.

Cryptography and Encryption: Blockchain technology employs advanced cryptographic algorithms to secure data and transactions. Each transaction on the blockchain is encrypted, providing an added layer of protection against unauthorized access. Furthermore, cryptographic techniques such as digital signatures validate the authenticity of transactions, ensuring that they are genuine and unaltered. These cryptographic measures contribute to the overall security of the blockchain, making it highly resistant to hacking and tampering.

Decentralization and Security: Traditional centralized systems are vulnerable to cyber attacks and data breaches because they have a single point of failure. In contrast, blockchain operates on a decentralized network of nodes, where multiple copies of the ledger are stored and maintained. This decentralization makes the blockchain more secure, as an attacker would need to compromise a majority of the nodes to alter the data. With no central authority controlling the blockchain, it becomes more difficult for malicious actors to manipulate or tamper with the records.

Identity Protection: In a blockchain network, participants have control over their own digital identities. When engaging in transactions, users can provide only the necessary information required, minimizing the risk of exposing sensitive personal data. Additionally, blockchain technology allows for the use of private and public keys, which ensure secure authentication and authorization without the need to share personal information. This protection of personal identity and data helps to mitigate the risk of identity theft and unauthorized access to sensitive information.

Secure Data Storage: Blockchain technology offers a secure and decentralized solution for storing data. Traditional centralized databases are vulnerable to data breaches and unauthorized access. In contrast, the distributed nature of the blockchain ensures that data is stored across multiple nodes, making it highly resilient to attacks. Furthermore, the use of cryptographic hashing protects the integrity and confidentiality of the data stored on the blockchain.

Overall, enhanced security and privacy are among the most significant advantages of blockchain technology. With its decentralized architecture, cryptographic techniques, and immutability, blockchain provides a secure and tamper-proof environment for conducting transactions and storing sensitive data. These features make it an attractive solution for industries such as finance, healthcare, and supply chain management, where security and privacy are critical considerations.

Eliminating Intermediaries and Reducing Costs

Blockchain technology has the potential to disrupt the traditional role of intermediaries in various industries. By enabling direct peer-to-peer transactions, blockchain eliminates the need for intermediaries, resulting in significant cost savings and increased efficiency.

Streamlined Processes: In many industries, transactions and processes often involve multiple intermediaries, such as banks, brokers, or legal entities. Each intermediary adds complexity, delays, and additional costs to the transaction. With blockchain, transactions can be conducted directly between parties, removing the need for intermediaries and simplifying the overall process. This streamlined approach results in faster and more efficient transactions, reducing the time and effort required to complete a transaction.

Reduced Transaction Costs: Intermediaries typically charge fees for their services, increasing the overall cost of transactions. By eliminating intermediaries, blockchain technology reduces or even eliminates these fees. This can result in significant cost savings, especially in industries with high transaction volumes or complex financial processes. For example, cross-border transactions often involve multiple intermediaries, each charging fees and adding processing time. With blockchain, transactions can be conducted directly between parties, reducing fees and increasing the speed of transactions.

Increased Accessibility: Traditional financial systems often exclude individuals without access to banking services or identification documentation. Blockchain technology has the potential to provide financial services to the unbanked or underbanked populations by enabling decentralized peer-to-peer transactions. This increased accessibility can drive financial inclusion and empower individuals who are currently excluded from traditional financial systems.

Smart Contracts: Smart contracts are self-executing contracts with the terms of the agreement written directly into code. These contracts automatically execute predefined actions and eliminate the need for intermediaries to enforce or oversee the agreement. With blockchain, smart contracts can be implemented, reducing the need for costly legal intermediaries and streamlining contract execution. Organizations can automate processes, such as payment settlements or supply chain agreements, reducing costs and improving efficiency.

Supply Chain Efficiency: Supply chains often involve multiple parties, including manufacturers, suppliers, distributors, and retailers. Each party has its own systems and records, leading to inefficiencies and lack of transparency. By utilizing blockchain technology, supply chain transactions can be recorded and shared on a single, transparent ledger. This shared visibility eliminates disputes, reduces fraud, and ensures traceability of goods. By eliminating intermediaries and enhancing transparency, blockchain improves supply chain efficiency and reduces costs associated with delays, disputes, or unverified products.

Financial Inclusion: In developing countries, many individuals lack access to traditional banking services. Blockchain technology can enable the creation of decentralized financial systems that provide accessible and affordable financial services. By eliminating the need for intermediaries and using digital wallets, blockchain can empower individuals to participate in financial activities such as saving, borrowing, and transferring money without depending on traditional banking systems.

By eliminating intermediaries and reducing costs, blockchain technology offers significant benefits to various industries. The ability to conduct direct peer-to-peer transactions, streamlining processes, and removing unnecessary fees can revolutionize sectors such as finance, supply chain, and legal services. As blockchain adoption increases, the potential for cost savings and increased efficiency will continue to expand, opening doors to new possibilities and disrupting traditional business models.

Transparency and Traceability

Transparency and traceability are crucial factors in building trust and accountability in modern business operations. Blockchain technology offers unparalleled transparency and traceability, revolutionizing industries by providing a clear view of transactions and the movement of goods or information.

Transparent Transactions: Blockchain technology ensures transparency by recording all transactions on a shared ledger that is visible to all participants. Unlike traditional systems where transaction data is hidden behind closed doors, blockchain provides real-time visibility into each transaction. Every participant in the network can independently verify the validity and details of each transaction, creating a level of trust that was previously difficult to achieve.

Immutable Audit Trail: The blockchain’s immutable nature creates an audit trail of all transactions, ensuring transparency and accountability. Once a transaction is recorded on the blockchain, it cannot be altered or deleted without consensus from the network. This feature provides a permanent and tamper-proof record of each transaction, making it ideal for industries where auditability is critical, such as finance, supply chain management, and healthcare.

Fraud Prevention: By providing a transparent view of transactions, blockchain technology helps prevent fraud and unauthorized activities. The visibility and traceability provided by blockchain make it easier to detect any inconsistencies or suspicious transactions. This is particularly impactful in industries such as finance and insurance, where fraudulent activities can have significant consequences and financial losses. With transparent transactions and permanent records, blockchain reduces the room for fraudulent behavior.

Supply Chain Transparency: Blockchain technology has the potential to transform supply chains by providing transparent and traceable records of every step. From raw material sourcing to manufacturing and distribution, blockchain allows all participants to track and verify the origin, movement, and quality of goods. This transparency reduces the risk of counterfeit products, ensures ethical sourcing, and enhances consumer trust. Consumers can verify the authenticity and quality of products by simply scanning a QR code or accessing the blockchain network, providing them with unprecedented insight into the supply chain.

Data Transparency and Privacy: Blockchain strikes a balance between transparency and privacy when it comes to data. While all transactions are visible on the blockchain, the personal or sensitive data within those transactions can be protected through encryption and cryptography. Users can maintain control over their own data, deciding what information to share and with whom. This enhanced data privacy ensures transparency in transactions while protecting individual privacy rights.

Accountability and Ethical Practices: Blockchain technology promotes accountability and ethical practices by making it easier to track and verify actions. Industries with complex supply chains, such as food production and luxury goods, can use blockchain to ensure that ethical standards are met at every stage. For example, blockchain can help verify that fair trade practices are followed, ensuring that producers are paid fairly and consumers are obtaining ethically sourced products.

Blockchain technology’s transparency and traceability features have far-reaching implications in numerous industries. By providing a clear view of transactions, reducing fraud, enhancing supply chain transparency, and promoting ethical practices, blockchain is transforming the way businesses operate, instilling trust, and creating a more accountable and responsible ecosystem.

Improved Efficiency and Speed

Efficiency and speed are crucial factors in today’s fast-paced and competitive business environment. Blockchain technology offers significant improvements in efficiency and speed, revolutionizing processes across various industries.

Streamlined Transactions: Traditional transactions often involve multiple intermediaries and complicated processes. Each intermediary adds delays, administrative overhead, and the potential for errors. Blockchain eliminates the need for intermediaries by enabling direct peer-to-peer transactions. This streamlined approach simplifies the transaction process, reducing the time and effort required to complete a transaction. By removing intermediaries, blockchain eliminates the need for time-consuming verifications and manual reconciliations, resulting in faster and more efficient transactions.

Automated Processes with Smart Contracts: Blockchain technology introduces the concept of smart contracts, which are self-executing contracts with predefined conditions written directly into the code. Smart contracts automate transactional processes and eliminate the need for manual intervention. These contracts automatically execute tasks and trigger actions based on predefined conditions, ensuring accuracy and efficiency. For example, in supply chain management, smart contracts can automate payment settlements and trigger shipment notifications, reducing delays and human errors.

Real-Time Settlements: Traditional financial systems and cross-border transactions often involve lengthy settlement periods. The involvement of multiple intermediaries and complex processes can result in delays that can extend for several days. Blockchain technology allows for near-instantaneous settlement of transactions. By removing intermediaries and utilizing smart contracts, blockchain enables real-time settlements, providing immediate transaction finality. This speed of settlement is particularly valuable in industries such as finance, where time is of the essence.

Efficient Supply Chain Management: The supply chain involves numerous stakeholders, including manufacturers, suppliers, distributors, and retailers. Traditional supply chain systems often lack transparency, resulting in delays, disruptions, and inefficiencies. With blockchain technology, supply chain processes can be streamlined, and information can be seamlessly shared between participants. Real-time visibility and access to shared data eliminate delays caused by manual data entry and reconciliation. By improving coordination and reducing administrative inefficiencies, blockchain enhances overall supply chain efficiency.

Reduced Administrative Overhead: Traditional recordkeeping and reconciliation processes are often labor-intensive and time-consuming. Blockchain technology eliminates the need for centralized record-keeping and manual reconciliation, reducing administrative overhead. By providing a single, immutable source of truth, blockchain eliminates discrepancies and reduces the need for costly auditing and verification processes. This reduction in administrative burden frees up resources to focus on more value-added tasks, ultimately improving overall efficiency.

Decentralized Verification and Validation: Blockchain operates on a decentralized network of nodes, eliminating the need for centralized verification and validation processes. Each node in the network independently verifies transactions, ensuring their accuracy and integrity. This decentralized approach reduces reliance on a single point of authority and eliminates the delays and costs associated with centralized verification. As a result, transactions can be processed and validated more efficiently, speeding up the overall process.

Overall, blockchain technology offers improved efficiency and speed in various aspects of business operations. Whether it’s streamlining transactions, automating processes with smart contracts, enabling real-time settlements, enhancing supply chain management, reducing administrative overhead, or decentralizing verification, blockchain has the potential to revolutionize industries by making them faster, more efficient, and ultimately more competitive.

Decentralization and Resilience

Decentralization and resilience are fundamental characteristics of blockchain technology that contribute to its importance and potential impact. By operating on a decentralized network, blockchain enhances security, reduces the vulnerability of centralized systems, and ensures the continuity of operations even in the face of disruptions.

Decentralized Network: Unlike traditional systems that rely on a central authority or a single point of control, blockchain operates on a decentralized network of computers or nodes. Each node independently participates in maintaining the blockchain, ensuring that no single entity has control over the entire system. This decentralized architecture distributes the processing power, storage, and decision-making across multiple nodes, enhancing security, and reducing the risk of a single point of failure.

Enhanced Security: Decentralization makes the blockchain highly secure by reducing the risks associated with traditional centralized systems. In a decentralized blockchain network, an attacker would need to compromise a majority of the nodes to manipulate or alter the data. This level of security is significantly higher compared to centralized systems, where a single point of vulnerability can lead to data breaches or malicious activities.

Reduced Operational Disruptions: Decentralization contributes to the resilience of blockchain. In traditional systems, a single point of failure or a network outage can bring the entire system to a halt. Blockchain’s distributed nature ensures that the network remains operational even if some nodes go offline or are compromised. The redundancy created by multiple nodes ensures the continuity of operations, making blockchain highly resilient to disruptions.

Consensus Mechanisms: Blockchain networks rely on consensus mechanisms to validate and agree on the state of the blockchain. Consensus mechanisms, such as Proof of Work (PoW) or Proof of Stake (PoS), involve multiple participants in the decision-making process. This decentralized consensus ensures that the majority of the network agrees on the validity and integrity of the blockchain. By reaching a consensus, the network validates the transactions and maintains the security and integrity of the system.

Trust and Transparency: Decentralization fosters trust and transparency in blockchain networks. Since every participant has access to the same information and can independently verify the transactions, trust is established without the need for a central authority. This transparency ensures accountability and eliminates the need to trust a single entity to maintain the integrity of the system.

Resilience in Disaster Recovery: Blockchain’s decentralization also proves valuable in disaster recovery scenarios. Traditional systems rely on centralized backups, making them vulnerable to physical damage, natural disasters, or cyber attacks. In contrast, blockchain’s decentralized architecture ensures the data is distributed across multiple nodes. If one node or location is affected, the data can be recovered from other nodes, ensuring the continuity of operations even in the face of unforeseen events.

Decentralization and resilience are key attributes of blockchain technology that contribute to its importance and application in various industries. By enhancing security, reducing reliance on centralized systems, ensuring operational continuity, and fostering trust and transparency, blockchain has the potential to transform business operations, provide robust solutions, and enable reliable services in an increasingly interconnected world.

Potential Applications of Blockchain Technology

Blockchain technology has the potential to revolutionize numerous industries by providing secure, transparent, and efficient solutions. While its initial use case was as the underlying technology for cryptocurrencies, blockchain’s versatility extends far beyond digital currencies. Here are some of the potential applications of blockchain technology:

- Finance and Banking: Blockchain can streamline financial processes by enabling faster and more secure transactions. It can facilitate cross-border payments, reduce remittance fees, and improve identity verification. Additionally, blockchain-based smart contracts can automate loan agreements, insurance claims, and trade settlements, minimizing the need for intermediaries.

- Supply Chain Management: The transparency and traceability of blockchain make it ideal for supply chain management. Blockchain can enhance traceability by recording and verifying the movement of goods at every stage, ensuring ethical sourcing, reducing counterfeiting, and improving overall supply chain efficiency. Furthermore, blockchain’s decentralized nature enables real-time visibility, reducing delays, and minimizing disputes.

- Healthcare: Blockchain has the potential to solve challenges in healthcare, such as interoperability, data privacy, and security. By securely storing patient records on the blockchain, healthcare providers can share information seamlessly while maintaining patient privacy. Blockchain can also enable more efficient drug tracking, clinical trials, and secure sharing of medical research data.

- Digital Identity: Blockchain can offer a decentralized and secure digital identity solution. With blockchain, individuals can control and manage their digital identities, reducing the risk of identity theft and fraud. Blockchain-based identity systems can enable faster and more secure verification processes, benefiting sectors such as voting, e-commerce, and financial services.

- Real Estate: Blockchain can revolutionize the real estate industry by enabling transparent and secure property transactions. Smart contracts can automate property transfers, ensuring immutability and reducing fraud. Blockchain-based property records can streamline title searches, reducing administrative burdens and increasing transaction speed.

- Energy Management: Blockchain can optimize energy management by enabling peer-to-peer energy trading and decentralized grid management. With blockchain, individuals can buy and sell excess energy directly, promoting energy efficiency and reducing reliance on traditional energy providers. Additionally, blockchain can track and verify renewable energy sources, ensuring transparency in the generation and distribution of clean energy.

- Education and Credentialing: Blockchain can provide a secure and verified method of storing and sharing educational credentials and certifications. This could streamline hiring processes, minimize fraud, and increase trust in educational institutions. Blockchain technology can also enable micro-credentialing and lifelong learning records.

- Government Services: Blockchain has the potential to streamline government services by providing secure and transparent systems for voting, property registration, identity management, and public records. By leveraging blockchain, governments can enhance transparency, reduce corruption, and improve the efficiency of their operations.

These are just a few examples of the potential applications of blockchain technology. As the technology matures and more industries explore its capabilities, new and innovative use cases will continue to emerge. The versatility, security, and transparency provided by blockchain make it a transformative technology with wide-ranging implications across various sectors.

Conclusion

Blockchain technology has emerged as a powerful and transformative force, promising enhanced security, efficiency, and transparency across various industries. Its decentralized nature, coupled with advanced cryptographic techniques, provides a robust solution for addressing challenges in traditional systems. The potential applications of blockchain are vast and diverse, ranging from financial services to supply chain management, healthcare, digital identity, real estate, energy management, education, and government services.

By eliminating intermediaries, blockchain reduces costs, streamlines processes, and enhances efficiency. The transparency and immutability of the blockchain create trust and accountability, enabling secure and auditable transactions. Moreover, the decentralization of blockchain enhances security, making it resistant to attacks and ensuring operational resilience.

However, as with any emerging technology, blockchain also faces challenges that need to be addressed. Scalability, energy consumption, regulatory frameworks, and standardization are among the areas that require further exploration and development to unlock the true potential of blockchain.

As blockchain technology continues to evolve, businesses and organizations must embrace its capabilities and explore innovative use cases. Collaborations, research, and development efforts are key to harnessing the full potential of blockchain and creating solutions that truly transform industries.

In conclusion, blockchain technology offers a new paradigm for secure, transparent, and efficient transactions. Its potential to disrupt industries and reshape business processes is undeniable. By leveraging blockchain, organizations can improve security, reduce costs, enhance trust, and unlock new opportunities in a rapidly evolving digital landscape.