Introduction

Welcome to the world of blockchain technology! In recent years, the blockchain has emerged as an innovative and revolutionary concept that has the potential to disrupt various industries, including finance, supply chain management, healthcare, and more. But what exactly is the blockchain, and how is it being integrated into popular applications like Cash App?

The blockchain can be described as a decentralized and distributed digital ledger that records transactions across multiple computers or nodes. Unlike traditional centralized systems, where transactions are processed by a single authority, the blockchain allows for peer-to-peer transactions without the need for intermediaries. This makes the blockchain transparent, secure, and resistant to tampering or fraud.

At its core, the blockchain is built upon a network of interconnected computers, each containing a copy of the ledger. As new transactions occur, they are grouped together into blocks and added to the chain in a chronological order. This ensures the immutability and integrity of the data, as any attempt to alter a previous block would require consensus from the majority of the network.

Now, let’s dive deeper into how the blockchain works and how it is utilized on Cash App, the popular mobile payment service developed by Square.

What is the blockchain?

The blockchain is a decentralized and distributed digital ledger that allows for transparent and secure transactions. It was first introduced in 2008 as a core component of the cryptocurrency Bitcoin, but its potential extends far beyond digital currencies. The blockchain can be thought of as a digital record-keeping system that records transactions across multiple computers or nodes.

Unlike traditional centralized systems, where transactions are processed and verified by a single authority, the blockchain operates on a peer-to-peer network. This means that transactions are validated by multiple participants, known as nodes, who reach consensus on the validity of each transaction.

One of the key features of the blockchain is its immutability. Once a transaction is recorded on the blockchain, it is nearly impossible to alter or delete. This is because each new block in the chain contains a cryptographic hash of the previous block, creating a chain of interlinking blocks. Any attempt to tamper with a previous block would require the alteration of subsequent blocks and the consensus of the majority of the network participants.

Another important characteristic of the blockchain is transparency. Every transaction that occurs on the blockchain is visible to all participants in the network. While the actual identities of the participants may be pseudonymous, the details of the transactions, including the sender, receiver, and the amount transacted, are recorded on the blockchain.

Privacy is also a critical consideration on the blockchain. While the details of transactions are visible, the identities of the participants are often obfuscated to protect their privacy. This is achieved through the use of cryptographic techniques that ensure the confidentiality of the participants involved.

The blockchain has gained significant attention due to its potential to revolutionize various industries. Its decentralized nature eliminates the need for intermediaries, reducing costs and increasing efficiency. Additionally, the use of cryptographic techniques ensures the security and integrity of transactions, making it highly resistant to fraud and tampering.

In the next section, we will explore how the blockchain works in more detail and how it is specifically utilized on Cash App.

How does the blockchain work?

To understand how the blockchain works, let’s break it down into three key components: transactions, blocks, and consensus.

1. Transactions: Transactions are the building blocks of the blockchain. They represent the transfer of assets, such as cryptocurrencies or digital assets, between participants. Each transaction contains information such as the sender’s address, the receiver’s address, and the amount being transferred. These transactions are grouped together and added to a block.

2. Blocks: Blocks are data structures that contain a set of transactions. Each block is linked to the previous block through a cryptographic hash, creating a chain of blocks, hence the term “blockchain”. The inclusion of the hash of the previous block ensures the integrity and immutability of the blockchain. Once a block is added to the chain, it cannot be altered without consensus from the majority of the network.

3. Consensus: Consensus is the mechanism by which participants in the blockchain agree on the validity of transactions and the order in which they are added to the blockchain. In a decentralized network, achieving consensus is crucial to prevent any single entity from gaining control or manipulating the blockchain. Different blockchain networks employ various consensus algorithms, such as Proof of Work (PoW) or Proof of Stake (PoS), to ensure agreement among participants.

Let’s take a closer look at two common consensus algorithms:

– Proof of Work (PoW): In a PoW algorithm, participants, known as miners, compete to solve complex mathematical puzzles in order to validate transactions and add them to the blockchain. The first miner to solve the puzzle is rewarded with newly minted cryptocurrency. This process requires a significant amount of computational power and energy, making it secure but resource-intensive.

– Proof of Stake (PoS): In a PoS algorithm, the ability to validate transactions and add blocks to the blockchain is based on the participant’s stake, or ownership, of the cryptocurrency. Participants who hold a larger amount of the cryptocurrency have a higher chance of being chosen to validate transactions. This consensus mechanism is more energy-efficient than PoW but still ensures the security and integrity of the blockchain.

Overall, the blockchain operates on a decentralized network where transactions are grouped into blocks and added to a chain in a sequential and immutable manner. The consensus mechanism ensures that transactions are validated by multiple participants and prevents any single entity from controlling the blockchain.

Now that we have a clear understanding of how the blockchain works, let’s explore how it is used on Cash App in the next section.

How is the blockchain used on Cash App?

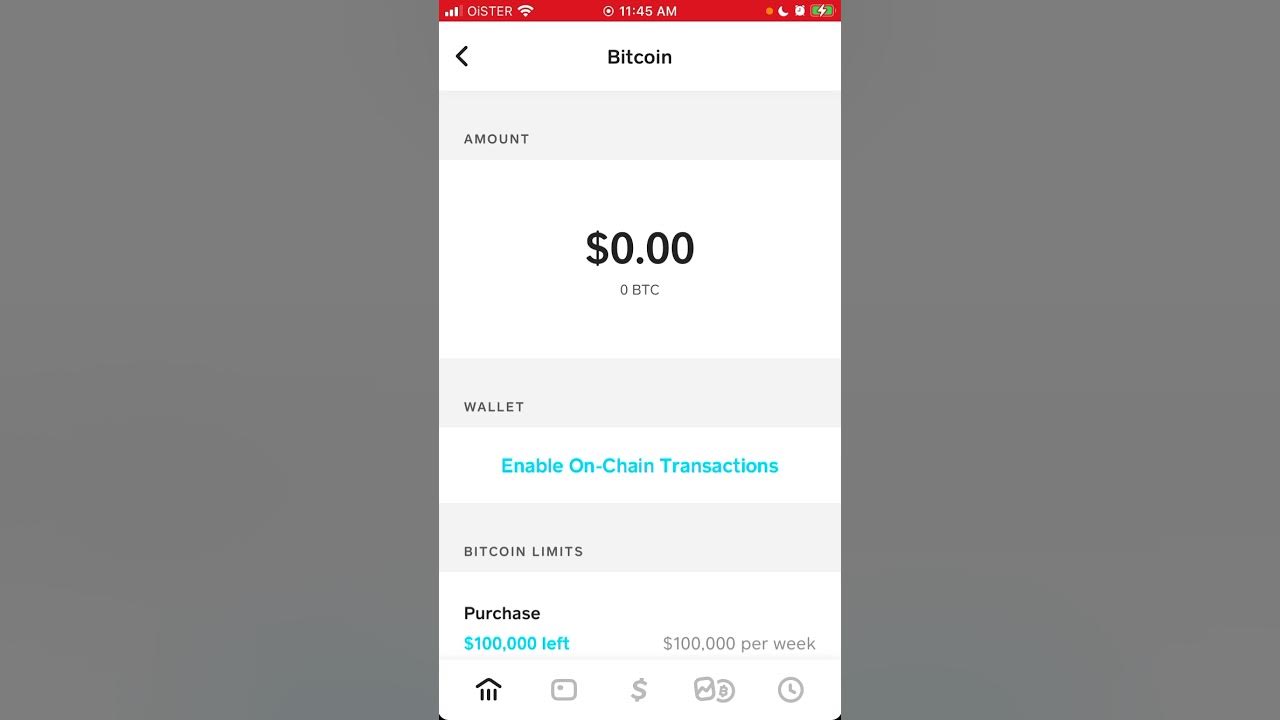

Cash App, a popular mobile payment service developed by Square, has integrated the blockchain into its platform to enhance the speed and efficiency of transactions. Cash App users have the option to buy, sell, and send cryptocurrencies, such as Bitcoin, directly from their accounts.

When users make a cryptocurrency transaction on Cash App, it is processed and recorded on the blockchain. This provides a transparent and secure way of verifying and tracking the movement of digital assets. By leveraging the blockchain, Cash App ensures the integrity of transactions and reduces the reliance on traditional banking systems.

One key advantage of utilizing the blockchain on Cash App is the speed of transactions. Traditional banking systems often involve multiple intermediaries, resulting in delays and higher transaction fees. With the blockchain, transactions can be processed and settled quickly, bypassing intermediaries and streamlining the payment process.

In addition, the use of the blockchain on Cash App provides users with greater control and ownership of their assets. By holding cryptocurrencies in their Cash App account, users have the ability to manage and transfer their digital assets at any time. This empowers individuals to be in control of their financial transactions without the need for third-party intervention.

Cash App also offers a feature called “Bitcoin Boost,” which allows users to invest in Bitcoin directly from their Cash App balance. This feature leverages the blockchain to enable fractional ownership of Bitcoin, making it accessible to a wider range of users. It provides a convenient and seamless way for individuals to enter the world of cryptocurrencies without the need for complex wallets or exchanges.

Furthermore, Cash App utilizes the blockchain to ensure the security and privacy of its users. The decentralized nature of the blockchain eliminates the risk of a single point of failure and makes it highly resistant to hacking or data breaches. Additionally, the use of cryptographic techniques guarantees the confidentiality of user information and transaction details.

By incorporating the blockchain into its platform, Cash App is able to offer users a secure, efficient, and user-friendly way to transact with cryptocurrencies. Whether it’s buying, selling, or sending digital assets, Cash App ensures that transactions are processed quickly and securely, providing users with a seamless experience in the world of digital finance.

Benefits of using the blockchain on Cash App

The integration of the blockchain into Cash App brings several benefits to users, enhancing the overall user experience and making transactions more efficient, secure, and transparent.

1. Speed and Efficiency: The use of the blockchain on Cash App enables fast and seamless transactions. By eliminating intermediaries and leveraging the decentralized nature of the blockchain, transactions can be processed and settled quickly, reducing the time and effort required for traditional banking processes. Users can send and receive funds internationally without the delays and fees associated with traditional cross-border transactions.

2. Security and Transparency: The blockchain provides enhanced security for transactions on Cash App. The decentralized nature of the blockchain means that there is no single point of failure, making it highly resistant to hacking and fraud. Each transaction is recorded on the blockchain, ensuring transparency and enabling users to track the movement of their funds. This transparency builds trust and confidence among users, as they can verify the legitimacy and integrity of transactions.

3. Ownership and Control: By utilizing the blockchain, Cash App offers users greater control and ownership of their digital assets. Users can hold and manage cryptocurrencies directly within their Cash App accounts, giving them full control over their funds without relying on third-party custodians. This empowers individuals to be in charge of their financial transactions and eliminates the need for intermediaries.

4. Accessibility: Cash App’s integration with the blockchain makes cryptocurrencies more accessible to a wider audience. Users can easily buy, sell, and hold cryptocurrencies such as Bitcoin with just a few taps on their mobile devices. The fractional ownership feature, known as “Bitcoin Boost,” allows users to invest in Bitcoin without needing to buy a whole coin, making it more affordable and inclusive for individuals interested in digital assets.

5. Lower Costs: By leveraging the blockchain, Cash App reduces transaction costs associated with traditional banking systems. The elimination of intermediaries and the streamlined process of blockchain transactions result in lower fees for users. This enables individuals to transact with cryptocurrencies more cost-effectively, encouraging wider adoption and usage of digital assets.

Overall, the integration of the blockchain into Cash App brings numerous advantages to users. It enhances the speed, security, and transparency of transactions, provides greater control and ownership of digital assets, and lowers costs associated with traditional banking systems. Cash App’s utilization of the blockchain demonstrates its commitment to offering innovative and user-friendly financial services, making it a popular choice for individuals looking to transact with cryptocurrencies.

Security and Privacy Considerations

While the integration of the blockchain into Cash App brings numerous benefits, it is important to understand and address the security and privacy considerations that come with transacting with digital assets.

1. Security: The blockchain itself is considered highly secure due to its decentralized and immutable nature. However, it is crucial for users to take additional precautions to protect their accounts and assets. Strong password protection, two-factor authentication, and keeping software up to date are essential to safeguard against unauthorized access. Users should also be cautious of phishing attempts and avoid sharing sensitive information.

2. Wallet Security: Cash App offers users a digital wallet to store cryptocurrencies. It is important to understand that the security of the wallet lies in the hands of the user. Keeping private keys secure and utilizing hardware wallets or other offline storage methods can provide an extra layer of protection against hacking attempts. It is recommended to research and implement best practices for securing digital wallets.

3. Counterparty Risk: While the blockchain offers transparency and eliminates the need for intermediaries, there is still a risk when transacting with unknown or untrusted parties. Users should exercise caution when sending funds to unfamiliar addresses and verify the legitimacy of recipients. It is advisable to double-check wallet addresses and use trusted platforms for exchanging or purchasing cryptocurrencies.

4. Privacy: While the blockchain is transparent, it also offers pseudonymity for users. Cryptocurrency transactions on the blockchain are associated with unique wallet addresses rather than personal identification. However, it is important to note that the transaction details themselves are publicly visible. To enhance privacy, users can employ techniques like CoinJoin or privacy-focused cryptocurrencies.

5. Regulatory Compliance: As cryptocurrencies and blockchain technology evolve, there may be legal and regulatory considerations to be aware of. Users should stay updated on changing regulations and tax obligations related to cryptocurrency transactions. Cash App, as a reputable service provider, follows regulatory guidelines and implements security measures to ensure compliance and protect user interests.

It is essential for users to educate themselves about the potential risks and take appropriate measures to protect their security and privacy when using Cash App or any other platform that utilizes the blockchain. Staying informed, employing secure practices, and being mindful of potential scams or vulnerabilities are key in mitigating risks associated with digital asset transactions.

Conclusion

The integration of the blockchain into Cash App has revolutionized the way individuals transact with digital assets, offering users a secure, efficient, and user-friendly platform for buying, selling, and sending cryptocurrencies. By leveraging the decentralized nature of the blockchain, Cash App has enhanced the speed, security, and transparency of transactions, providing users with greater control and ownership of their digital assets.

The blockchain, as the underlying technology, ensures the integrity and immutability of transactions recorded on the Cash App platform. Its decentralized and distributed nature eliminates the need for intermediaries, reducing costs and enabling faster settlements. This enhances the overall user experience, making it easier and more accessible for individuals to participate in the world of digital finance.

Security and privacy considerations play a vital role in ensuring the protection of user accounts and assets. Cash App provides users with tools and features to enhance security, such as strong password protection and two-factor authentication. However, users should also take responsibility for safeguarding their accounts, implementing best practices for wallet security and staying vigilant against potential scams.

While the blockchain brings transparency to transactions, it also offers pseudonymity, enabling users to transact with a certain level of privacy. However, users should be aware of the potential risks associated with the publicly visible transaction details and take appropriate measures to enhance privacy and comply with regulatory requirements.

In conclusion, the integration of the blockchain into Cash App has revolutionized the way individuals engage with digital assets. By utilizing the blockchain, Cash App has created a user-friendly and secure platform that empowers individuals to transact with cryptocurrencies quickly and conveniently. As the blockchain technology continues to evolve, Cash App and similar platforms will continue to play a pivotal role in shaping the future of digital finance.