Introduction

As the world of finance continues to evolve, so do the technologies that shape it. Two terms that have gained significant attention in recent years are Regtech and Fintech. These innovative concepts have paved the way for disruptive changes in the financial industry, offering new possibilities and solutions for both businesses and consumers.

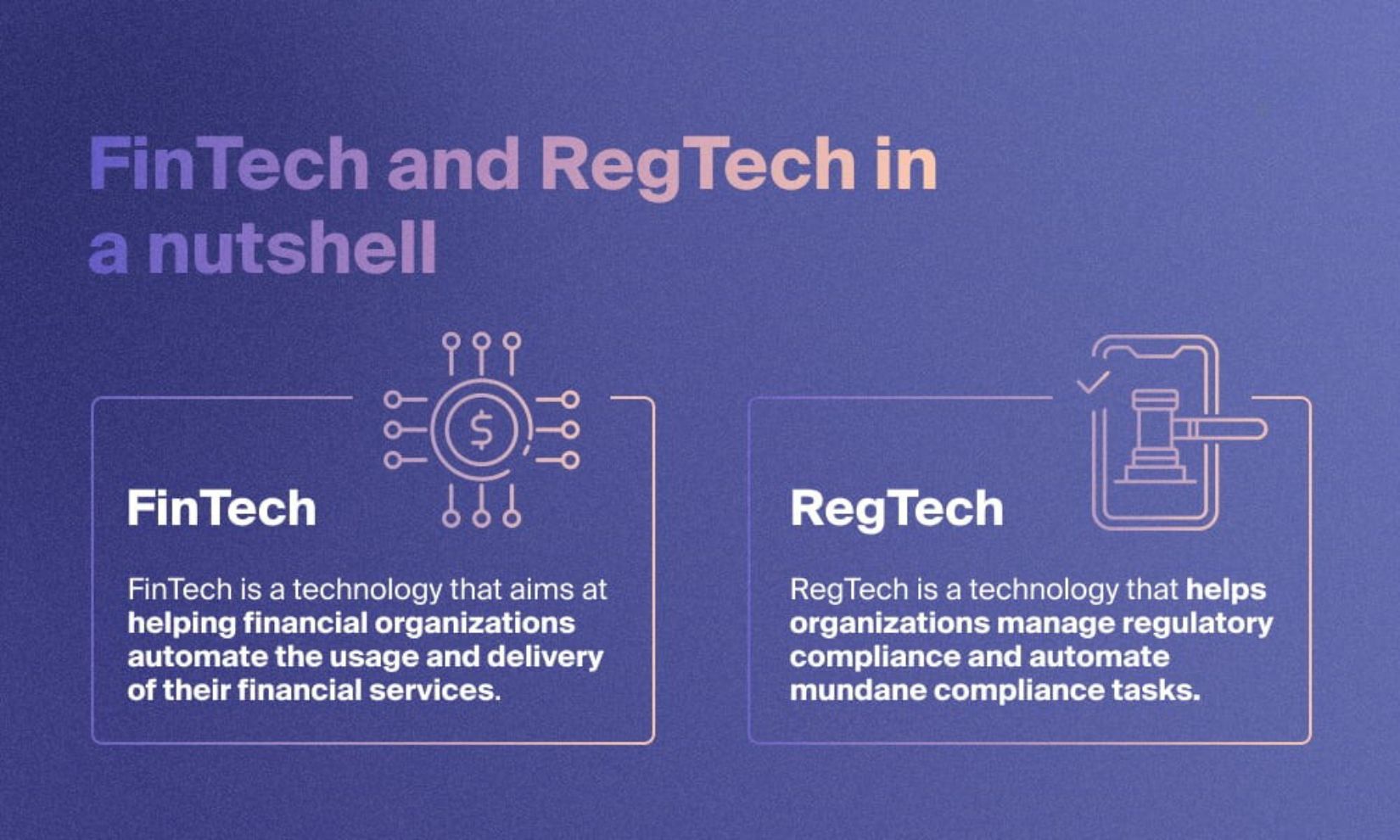

Regtech, short for regulatory technology, refers to the use of advanced technologies to streamline and automate compliance processes in the financial sector. Its primary goal is to assist financial institutions in meeting their regulatory obligations more efficiently and effectively. On the other hand, Fintech, or financial technology, encompasses a broad range of technologies that aim to improve financial services, enhance customer experiences, and reshape traditional financial systems.

The relationship between Regtech and Fintech is significant, as their combined forces offer immense potential for startups in the financial industry. Fintech startups can leverage Regtech solutions to navigate complex regulatory landscapes, ensuring compliance while simultaneously innovating their services and products.

In this article, we will explore the benefits of Regtech for fintech startups, the challenges they may face when implementing these solutions, and the key considerations when choosing Regtech solutions tailored to their specific needs. We will also delve into real-life case studies of successful Regtech integration and provide insights into future trends in the Regtech and Fintech space.

By understanding the pivotal role of Regtech and its symbiotic relationship with Fintech, startups in the financial sector can position themselves to thrive in an ever-evolving regulatory landscape while driving innovation and delivering exceptional value to their customers.

What is Regtech?

Regtech, short for regulatory technology, refers to the use of technological solutions to simplify and automate compliance processes in the financial industry. It encompasses a wide range of technologies such as data analytics, artificial intelligence, machine learning, blockchain, and cloud computing, among others.

The main aim of Regtech is to help financial institutions meet their regulatory obligations in a more efficient and cost-effective manner. By leveraging these advanced technologies, companies can streamline compliance workflows, reduce manual efforts, accelerate data analysis, and improve reporting accuracy.

Regulatory requirements in the financial sector can be complex and constantly evolving. Traditional compliance methods often involve manual processes, paperwork, and significant human resources. This approach can be time-consuming, error-prone, and costly, leading to inefficiencies and exposing businesses to compliance risks.

In contrast, Regtech solutions offer innovative tools and systems that automate compliance processes, enhance data accuracy, and provide real-time monitoring capabilities. These solutions help financial institutions monitor and adhere to regulations more effectively, detect and prevent potential compliance violations, and minimize the risk of penalties or reputational damage.

Regtech solutions can be categorized into several areas, including:

- Reporting and Compliance: These solutions automate reporting requirements by collecting, analyzing, and submitting the necessary data to regulatory authorities. They ensure timely and accurate reporting, reducing the risk of non-compliance.

- Risk Management: These tools help institutions assess and monitor risks more efficiently. They utilize advanced analytics to identify potential compliance breaches, vulnerabilities, and emerging risks.

- Identity Verification and KYC: Know Your Customer (KYC) regulations require financial institutions to verify the identity of their customers. Regtech solutions provide secure and automated processes for identity verification, customer due diligence, and risk assessment.

- Transaction Monitoring: Regtech solutions offer real-time monitoring of financial transactions to identify suspicious activities, fraud, money laundering, and other financial crimes. They use algorithms and pattern recognition to detect anomalies and trigger alerts for investigation.

Overall, Regtech empowers financial institutions by offering efficient compliance solutions, reducing costs, improving accuracy, and mitigating regulatory risks. By leveraging these technologies, businesses can navigate complex regulatory frameworks and focus on innovating and delivering better services to their customers, while ensuring compliance with stringent regulations.

What is Fintech?

Fintech, short for financial technology, refers to the use of advanced technologies to improve financial services, streamline processes, and provide innovative solutions in the financial industry. Fintech encompasses a wide range of applications, including mobile banking, digital payments, peer-to-peer lending, robo-advisors, and blockchain technology.

Fintech has emerged as a disruptive force in the financial sector, challenging traditional banking models and transforming the way financial transactions are conducted. It aims to bridge the gap between technology and finance, introducing faster, more convenient, and user-friendly financial services.

One key aspect of Fintech is its focus on customer-centric solutions. By leveraging technology, Fintech companies can offer personalized, on-demand services that cater to the specific needs and preferences of individual customers. This includes providing seamless mobile banking experiences, enabling quick and secure digital payments, and offering automated investment advisory services.

Some notable examples of Fintech applications include:

- Mobile Banking: Fintech has revolutionized the banking industry by enabling customers to perform banking transactions through mobile apps. These apps provide easy access to account information, fund transfers, bill payments, and other services, all from the convenience of their smartphones.

- Digital Payments: Fintech has made digital payments simpler and more efficient. Mobile wallets, payment gateways, and contactless payment options have gained popularity, offering convenient and secure alternatives to traditional cash and card-based transactions.

- Peer-to-Peer Lending: Fintech platforms have facilitated peer-to-peer lending, connecting borrowers directly with lenders without the involvement of traditional financial institutions. This allows for easier access to loans, lower interest rates, and quicker approval processes.

- Robo-Advisors: Fintech has introduced automated investment advisory services through robo-advisors. These digital platforms utilize algorithms and data analysis to provide personalized investment recommendations and portfolio management services, often at lower costs than traditional financial advisors.

- Blockchain Technology: Fintech has embraced blockchain technology, which offers transparent, secure, and decentralized transactional systems. Blockchain enables faster and more secure cross-border payments, smart contracts, and eliminates the need for intermediaries in various financial processes.

Fintech has not only transformed the way consumers interact with financial services but has also opened up new opportunities for startups and entrepreneurs in the industry. It has fostered innovation, increased competition, and improved financial inclusion by providing access to financial services for underserved populations.

The growth of Fintech shows no signs of slowing down, as technology continues to advance and consumer expectations evolve. Financial institutions and startups that embrace Fintech are at the forefront of shaping the future of finance, driving efficiency, convenience, and accessibility across the financial landscape.

The Relationship between Regtech and Fintech

The relationship between Regtech and Fintech is symbiotic, as these two realms of technology work together to create new possibilities and solutions in the financial industry.

On one hand, Fintech startups leverage Regtech solutions to navigate complex regulatory landscapes and ensure compliance with stringent regulations. This is crucial as compliance costs and risks can often hinder the growth and innovation of these startups. By implementing Regtech solutions, Fintech companies can automate compliance processes, reduce errors, and mitigate compliance risks, allowing them to focus on developing and delivering innovative financial products and services.

On the other hand, Regtech solutions benefit from the advancements in Fintech by leveraging cutting-edge technologies to streamline compliance processes. Fintech provides Regtech with improved data analytics, artificial intelligence, and machine learning capabilities, allowing for more accurate and efficient compliance monitoring, risk assessment, and reporting. In this way, Fintech acts as an enabler for the effectiveness and efficiency of Regtech solutions.

Moreover, Fintech startups often face challenges in entering highly regulated industries, such as banking and insurance. The integration of Regtech solutions helps these startups meet compliance requirements and gain the trust of regulatory authorities and potential customers. The combination of Regtech and Fintech allows startups to navigate regulatory complexities more effectively, overcome barriers to entry, and establish scalable and sustainable businesses.

Regtech and Fintech also share a common goal of enhancing customer experiences. By leveraging technology, both domains aim to provide more efficient, accessible, and user-friendly financial services. Regtech solutions help Fintech companies improve customer onboarding processes, enhance security measures, and ensure due diligence in identity verification and Know Your Customer (KYC) procedures. This enables startups to build trust with customers and offer seamless and secure financial experiences.

Additionally, the integration of Regtech and Fintech contributes to the broader digital transformation of the financial industry. As both sectors continue to evolve and innovate, they have the potential to reshape traditional financial systems and establish more agile, responsive, and resilient financial ecosystems. Regtech and Fintech pave the way for open banking initiatives, real-time transaction monitoring, data-driven decision making, and improved risk management in the financial sector.

Overall, the relationship between Regtech and Fintech is one of mutual support and collaboration. Fintech leverages Regtech tools and solutions to ensure compliance and mitigate regulatory risks, while Regtech harnesses the advancements in Fintech to enhance the efficiency and effectiveness of compliance processes. This synergy offers significant advantages for startups in the financial industry, enabling them to navigate regulatory challenges, deliver better customer experiences, and drive innovation in the ever-evolving landscape of finance.

Benefits of Regtech for Fintech Startups

Regtech solutions offer numerous benefits for Fintech startups, enabling them to navigate regulatory challenges, streamline compliance processes, mitigate risks, and focus on innovation and growth. Here are some key advantages of incorporating Regtech into Fintech startups:

- Efficiency and Automation: Regtech automates compliance processes, reducing manual efforts and the risk of human error. By streamlining workflows and leveraging advanced technologies such as AI and machine learning, Fintech startups can efficiently handle regulatory tasks, including data collection, reporting, and auditing.

- Cost Savings: Traditional compliance methods can be expensive, requiring significant human resources and manual checks. Regtech solutions offer cost-effective alternatives, minimizing the need for extensive staff or outsourced compliance services. The automation and digitization of compliance processes result in long-term cost savings for startups.

- Accuracy and Transparency: Regtech solutions enhance data accuracy and reporting transparency, reducing the risk of compliance errors, inaccuracies, and fraudulent activities. By implementing real-time monitoring tools and analytics, Fintech startups can detect anomalies, inconsistencies, and potential violations promptly, allowing for timely corrective action.

- Compliance Risk Mitigation: Regtech helps Fintech startups proactively identify and address compliance risks. By leveraging advanced analytics and risk assessment tools, they can assess potential risks, monitor regulatory changes, and adjust their operations accordingly. This proactive approach minimizes the risk of regulatory penalties, reputational damage, and customer trust erosion.

- Simplified Regulatory Reporting: Regtech solutions streamline the reporting process, making it easier for Fintech startups to meet regulatory requirements. These solutions automate the collection, analysis, and submission of data, reducing the time and effort required for compliance reporting tasks. As a result, startups can focus more on their core business activities and innovation.

- Enhanced Customer Trust and Experience: Compliance with regulations is essential for building trust with customers. Regtech solutions help Fintech startups establish robust and secure processes for customer onboarding, identity verification, and data privacy. This ensures that customers feel confident in the security and compliance practices of the startup, leading to improved customer trust and satisfaction.

- Scalability and Expansion: Regtech solutions are designed to scale with the growth of Fintech startups. These solutions offer flexibility, adaptability, and customization options, allowing startups to meet their evolving compliance needs as their business expands into new markets and jurisdictions. Regtech enables startups to stay compliant while venturing into new territories and exploring new business opportunities.

By leveraging the benefits of Regtech, Fintech startups can overcome regulatory hurdles, efficiently manage compliance, and optimize their operations. This allows them to dedicate more time and resources to innovation, product development, and delivering an exceptional customer experience. Ultimately, the integration of Regtech empowers Fintech startups to build sustainable, compliant, and successful businesses in the dynamic financial landscape.

Challenges of Implementing Regtech for Fintech Startups

While Regtech offers numerous benefits for Fintech startups, there are also challenges that they may face during the implementation process. Understanding these challenges is essential for startups to effectively integrate Regtech solutions into their operations. Here are some common challenges associated with implementing Regtech for Fintech startups:

- Complex Regulatory Environment: The regulatory landscape in the financial industry can be intricate and constantly evolving. Fintech startups must navigate through a multitude of regulations, compliance requirements, and licensing obligations. Adapting Regtech solutions to comply with these complex regulations can be a significant challenge.

- Data Privacy and Security: Fintech startups often deal with sensitive customer data, making privacy and security crucial considerations. Implementing Regtech solutions requires robust data privacy and security measures to protect customer information from theft, breaches, or unauthorized access. Compliance with data protection laws, such as GDPR, adds an additional layer of complexity.

- Integration with Legacy Systems: Fintech startups may have existing legacy systems that are not easily compatible with Regtech solutions. Integrating new technologies with legacy systems can be a complex and time-consuming process, requiring thorough data mapping, system restructuring, and ensuring seamless connectivity between different platforms.

- Capacity and Resource Constraints: Fintech startups, particularly those in their early stages, may face limitations in terms of financial resources, skilled personnel, and operational capacity. Implementing Regtech solutions often requires upfront investments in technology, training, and infrastructure, which can pose challenges for startups with limited budgets or small teams.

- Regulatory Updates and Change Management: As regulatory requirements change, Fintech startups need to keep their Regtech solutions up to date. This can involve monitoring regulatory changes, implementing necessary updates, and ensuring ongoing compliance. Managing these updates across various jurisdictions and keeping up with evolving regulations can be a complex task.

- Vendor Selection and Due Diligence: Choosing the right Regtech vendor is critical for startups. Conducting thorough due diligence, evaluating vendor capabilities, assessing scalability, and considering long-term partnerships are vital steps. However, the vast number of Regtech providers in the market can make the selection process daunting and time-consuming.

- Resistance to Change: Implementing Regtech solutions often requires changes in workflows, processes, and mindset within the organization. Resistance to change from employees and stakeholders can pose challenges, as they may need to adapt to new systems, learn new skills, and accommodate shifts in responsibilities.

Despite these challenges, Fintech startups can overcome them by taking a strategic and proactive approach to Regtech implementation. By conducting thorough planning, collaborating with Regtech vendors, dedicating resources to training and change management, and staying updated on regulatory changes, startups can navigate these challenges and unlock the benefits that Regtech offers.

Successful Case Studies of Regtech in Fintech Startups

Several Fintech startups have successfully implemented Regtech solutions, showcasing the transformative impact these technologies can have on compliance processes and overall business operations. Here are a few notable case studies:

- Stripe: Stripe, a leading online payment processing platform, leverages Regtech to facilitate compliance with anti-money laundering (AML) regulations. By integrating AI and machine learning algorithms into their system, Stripe automatically detects and blocks suspicious transactions, minimizing the risk of money laundering activities. This not only ensures compliance with regulatory requirements but also safeguards the platform’s integrity and protects user transactions.

- Trulioo: Trulioo, a global identity verification company, utilizes Regtech to assist Fintech startups in adhering to Know Your Customer (KYC) regulations. Their platform leverages a vast network of data sources, advanced analytics, and AI-driven algorithms to verify customer identities in real-time. Fintech startups can seamlessly integrate Trulioo’s Regtech solution to streamline customer onboarding processes, reduce manual checks, and ensure compliance with KYC requirements.

- Onfido: Onfido, an identity verification and authentication company, employs Regtech to help Fintech startups verify customer identities remotely. By utilizing AI algorithms and utilizing document verification, facial biometrics, and fraud detection technologies, Onfido automates the KYC process, improving accuracy, reducing fraud, and expediting customer onboarding. Their Regtech solution enables Fintech startups to maintain compliance with regulatory requirements while providing a seamless and secure user experience.

- Chainalysis: Chainalysis, a blockchain analysis firm, offers Regtech solutions to Fintech startups operating in the cryptocurrency sector. Their platform utilizes blockchain analytics, risk scoring algorithms, and compliance tools to monitor transactions, identify suspicious activities, and ensure compliance with anti-money laundering (AML) and counter-terrorism financing (CTF) regulations. Fintech startups can leverage Chainalysis’ Regtech solution to establish trust with regulatory bodies and strengthen their compliance practices.

- Kryon: Kryon, a robotic process automation (RPA) company, enables Fintech startups to automate compliance processes using Regtech. By deploying intelligent bots, Kryon’s Regtech solution automates data extraction, validation, and report generation for regulatory compliance. Fintech startups can significantly reduce manual efforts, improve accuracy, and ensure timely compliance with regulatory requirements, all while optimizing operational efficiency and scalability.

These case studies highlight the successful integration of Regtech in Fintech startups, demonstrating the tangible benefits these technologies bring in terms of compliance efficiency, risk mitigation, customer trust, and operational effectiveness. By leveraging Regtech solutions tailored to their specific needs and regulatory requirements, Fintech startups can navigate complex compliance landscapes with confidence, enabling them to focus on delivering innovative financial solutions and driving business growth.

Key Considerations when Choosing Regtech Solutions for Fintech Startups

When selecting Regtech solutions for Fintech startups, it’s essential to carefully consider various factors to ensure the chosen solution aligns with the startup’s specific needs and compliance requirements. Here are some key considerations to keep in mind:

- Regulatory Compliance: The chosen Regtech solution must align with the regulatory framework applicable to the Fintech startup’s industry, jurisdiction, and target market. It should assist in meeting specific compliance requirements, such as KYC, AML, data privacy, and reporting obligations.

- Scalability and Flexibility: Fintech startups typically experience rapid growth and need Regtech solutions that can scale alongside their business. The chosen solution should have the capacity to handle increasing data volumes, adapt to future regulatory changes, and accommodate the startup’s expansion into new markets or product offerings.

- Security and Data Privacy: Data protection is of utmost importance in Regtech implementations. Startups must evaluate the security measures and data privacy protocols of Regtech vendors to ensure compliance with applicable data protection regulations and protect sensitive customer information from unauthorized access or breaches.

- Integration and Compatibility: It’s crucial to assess how the chosen Regtech solution integrates with the existing IT infrastructure and systems of the Fintech startup. Seamless integration promotes efficiency, reduces implementation complexity, and minimizes disruptions to ongoing operations.

- Vendor Expertise and Reputation: Conduct thorough due diligence on Regtech vendors, considering factors like their experience, industry knowledge, track record, and reputation. Engaging with reputable vendors with a proven history of successful Regtech implementations will enhance the chances of a successful partnership.

- User Experience and Training: Consider the user-friendliness and intuitiveness of the Regtech solution’s interface. The chosen solution should be easy to navigate and understand for both technical and non-technical users within the startup. Additionally, evaluate the vendor’s training and support programs to ensure proper onboarding and ongoing assistance.

- Cultural Fit and Change Management: Assess how the Regtech solution aligns with the startup’s organizational culture and the willingness of employees to adapt to new technologies. Implementing Regtech requires change management processes to ensure smooth adoption and integration within the organization.

- Cost and ROI: Evaluate the total cost of ownership of the Regtech solution, including implementation, licensing, maintenance, and support. Consider the return on investment (ROI) in terms of time saved, operational efficiencies gained, compliance risk reduction, and potential future scalability.

By carefully considering these key factors, Fintech startups can make informed decisions when choosing Regtech solutions. Selecting the right Regtech partner will enable startups to effectively address their compliance needs, enhance operational efficiency, mitigate regulatory risks, and focus on driving innovation and growth in the dynamic world of financial technology.

Future Trends in Regtech and Fintech

The future of both Regtech and Fintech is characterized by continuous evolution and innovation, driven by technological advancements and changing regulatory landscapes. Here are some key trends to watch out for:

- Artificial Intelligence (AI) and Machine Learning (ML): The integration of AI and ML technologies will play a significant role in shaping the future of Regtech and Fintech. AI-powered solutions can analyze vast amounts of data in real-time, enabling more accurate risk assessment, fraud detection, and compliance monitoring. ML algorithms can improve predictive analytics, anomaly detection, and decision-making capabilities.

- Regulatory Sandboxes: Regulatory sandboxes, which provide a controlled environment for testing innovative products and services, will continue to gain traction. These sandboxes allow Fintech startups to collaborate with regulators, reducing the time to market for new solutions while ensuring compliance with regulatory requirements.

- Regulatory Reporting Standardization: Standardization of regulatory reporting formats and data requirements will simplify compliance processes for Fintech startups. Common data models and reporting frameworks will enable seamless data sharing, reduce reporting redundancies, and enhance regulatory oversight capabilities.

- Privacy-Enhancing Technologies: With the increasing focus on data privacy and protection, Regtech solutions will incorporate privacy-enhancing technologies such as differential privacy, secure multiparty computation, and homomorphic encryption. These technologies allow businesses to comply with data privacy regulations while still extracting valuable insights from sensitive data.

- Regtech for Emerging Technologies: As emerging technologies like blockchain, cryptocurrencies, and decentralized finance (DeFi) gain prominence, Regtech solutions will evolve to address the unique compliance challenges associated with these technologies. Implementing Regtech will help ensure the secure and compliant adoption of these emerging fintech trends.

- Collaboration and Partnerships: Collaboration between Regtech startups, Fintech startups, and regulatory bodies will foster innovative solutions and industry-standard compliance practices. Partnerships between Regtech vendors, Fintech startups, and traditional financial institutions will also drive the adoption of Regtech solutions, allowing for seamless integration within existing financial systems.

- Real-Time Monitoring and Reporting: The trend towards real-time monitoring and reporting will continue to gain momentum. Regtech solutions will provide real-time insights into potential compliance breaches, enabling proactive risk management and faster response to emerging regulatory challenges.

- Cloud and SaaS Solutions: The adoption of cloud-based and Software-as-a-Service (SaaS) models in Regtech will increase. Cloud-based solutions offer scalability, cost-effectiveness, and flexibility, allowing Fintech startups to access advanced Regtech functionalities without significant upfront investments in infrastructure.

- Global Regulatory Harmonization: Efforts towards global regulatory harmonization and collaboration will drive the development of standardized Regtech solutions. By aligning regulations and compliance frameworks across jurisdictions, Fintech startups can streamline their operations and expand their services internationally more easily.

These future trends in Regtech and Fintech will shape the landscape of the financial industry, allowing for more efficient compliance processes, improved customer experiences, and increased regulatory oversight. By embracing these trends and staying ahead of regulatory changes, Fintech startups can position themselves as leaders in the industry and drive further innovation in the intersection of technology and finance.

Conclusion

The integration of Regtech and Fintech heralds a new era of innovation, efficiency, and compliance in the financial industry. Regtech solutions empower Fintech startups to navigate complex regulatory landscapes, automate compliance processes, mitigate risks, and enhance customer trust.

Regtech streamlines compliance workflows, provides real-time monitoring capabilities, and leverages advanced technologies such as AI, ML, and blockchain. These solutions automate reporting, enhance risk management, ensure identity verification, and streamline transaction monitoring, enabling startups to meet regulatory obligations efficiently and effectively.

Fintech startups benefit from Regtech in various ways, including cost savings, improved accuracy, enhanced security, and enhanced scalability. By implementing Regtech solutions, startups can dedicate more resources to innovation, product development, and enhancing the customer experience.

Selecting the right Regtech solution requires careful consideration of factors such as regulatory compliance, scalability, security, integration, and vendor expertise. Fintech startups must also anticipate challenges related to regulatory complexity, data privacy, legacy system integration, and cultural change.

Looking into the future, trends such as AI/ML adoption, regulatory sandboxes, standardization, privacy-enhancing technologies, and global harmonization will continue to shape the Regtech and Fintech landscape. Collaboration and partnerships will drive innovation, while real-time monitoring, cloud/SaaS solutions, and regulatory harmonization will enhance operational effectiveness and compliance efficiency.

In conclusion, the combination of Regtech and Fintech holds immense potential for revolutionizing the financial industry. Fintech startups that effectively leverage Regtech solutions will gain a competitive edge, ensuring regulatory compliance, driving innovation, and delivering exceptional financial services to customers. As technology and regulations evolve, the successful integration of Regtech will be pivotal in shaping the future of finance.