What is Blockchain?

Blockchain is a revolutionary technology that has gained immense popularity in recent years. It is a decentralized ledger system that allows for secure and transparent peer-to-peer transactions without the need for intermediaries. In simple terms, it is a digital ledger that records transactions across multiple computers, known as nodes, which are linked together in a network.

Unlike traditional centralized systems, where transactions are controlled and verified by a single authority, blockchain relies on consensus among multiple participants to validate transactions. Each transaction is grouped into a block, which is then added to the chain of previous blocks, creating an immutable record of all transactions. This ensures that the data stored in the blockchain is secure, tamper-proof, and transparent.

One of the key features of blockchain is its ability to provide trust and transparency. As all participants in the network have access to the same information, it eliminates the need for intermediaries, such as banks or third-party payment processors, reducing costs and increasing efficiency in various industries.

Blockchain technology is most commonly associated with cryptocurrencies like Bitcoin, but its potential applications go beyond digital currencies. It can be used to streamline supply chain management, secure digital identities, enable smart contracts, enhance voting systems, and revolutionize various sectors including finance, healthcare, logistics, and more.

By utilizing cryptographic algorithms and distributed consensus mechanisms, blockchain ensures the integrity and security of data stored on the network. This makes it highly resistant to hacking and fraud, making it an attractive option for businesses and organizations looking to enhance security and efficiency in their operations.

Overall, blockchain is a transformative technology that has the potential to reshape industries and disrupt traditional processes. Its decentralized nature, transparency, and security make it a powerful tool for businesses to improve trust, reduce costs, and increase efficiency in a variety of applications.

How Does Blockchain Work?

Blockchain technology works through a combination of several key components to ensure the security and integrity of the data stored on the network. Understanding how blockchain works is essential to grasp its potential applications and benefits.

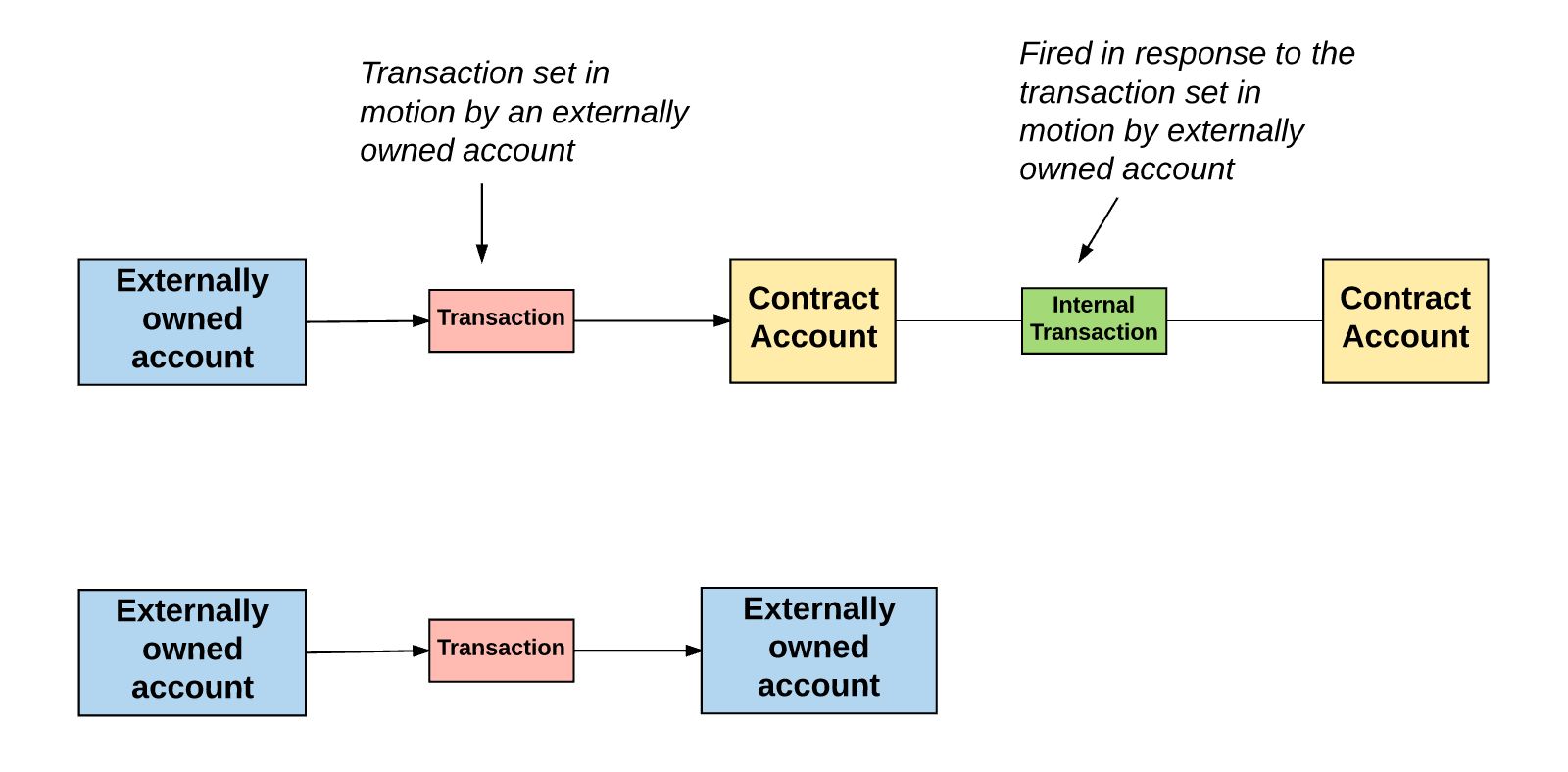

At its core, a blockchain consists of a chain of blocks, each containing a list of transactions. These transactions are grouped together and added to a block. Each block is then linked to the previous block using cryptographic hashes, creating a chain of blocks. This linkage ensures the immutability of the data, as any change in a block would require altering all subsequent blocks, making it virtually impossible to tamper with the data.

The key features that enable blockchain to work are:

- Decentralization: Instead of relying on a central authority, blockchain operates on a distributed network of computers, called nodes. These nodes validate transactions and store copies of the blockchain. Each node has a copy of the entire blockchain, ensuring redundancy and preventing a single point of failure.

- Consensus Mechanisms: In order to validate transactions and add them to the blockchain, consensus among the participating nodes is required. Different blockchain networks employ various consensus mechanisms, such as Proof of Work (PoW) or Proof of Stake (PoS), to ensure agreement and prevent malicious activities.

- Cryptography: Blockchain utilizes cryptographic algorithms to secure the data and maintain privacy. Each transaction within a block is secured using cryptographic hashing, which converts the transaction data into a unique string of characters. Any change in the transaction data will lead to a different hash, alerting the network to potential tampering.

- Smart Contracts: Blockchain technology also supports the execution of smart contracts, which are self-executing contracts with predefined rules and conditions. Smart contracts eliminate the need for intermediaries, automatically executing transactions when certain conditions are met. They enable automation and streamline processes in various industries.

When a new transaction occurs, it is broadcasted to the network and validated by the participating nodes. Once a consensus is reached, the transaction is added to a block. The block is then added to the blockchain and distributed to all nodes in the network, ensuring that all participants have an up-to-date and identical copy of the blockchain.

Blockchain’s transparency, security, and decentralization make it an ideal solution for industries that require reliable and tamper-proof record-keeping. Its ability to eliminate intermediaries, reduce fraud, and enhance data security has the potential to transform various sectors and improve trust among participants.

Factors That Affect the Cost of Blockchain

When considering the cost of implementing a blockchain project, it is important to understand the factors that can influence the overall expense. While the cost can vary depending on specific requirements and project complexity, there are several key factors that typically impact the cost of blockchain development.

- Scope of the Project: The scope and scale of the blockchain project play a significant role in determining the cost. Projects with complex functionalities, multiple integration points, and extensive customization will generally require more time and resources, resulting in a higher cost.

- Development Team: The cost of blockchain development also depends on the expertise and experience of the development team. Hiring highly skilled blockchain developers and experts can be more expensive, but it contributes to the successful implementation and efficient operation of the blockchain project.

- Infrastructure Costs: Implementing a blockchain requires appropriate infrastructure to support the network. This includes servers, storage systems, and other hardware components. The cost of infrastructure can vary depending on the scale and requirements of the blockchain network.

- Integration and Customization: If the blockchain needs to integrate with existing systems or requires customization to meet specific business needs, the development cost may increase. Integrating with external systems, such as payment gateways or IoT devices, can add complexity and require additional resources.

- Security Considerations: Security is a crucial aspect of any blockchain implementation. Implementing robust security measures, such as encryption, secure access controls, and auditing mechanisms, can add to the development cost. However, investing in security is essential to mitigate the risk of data breaches or unauthorized access.

- Network Scalability: If the blockchain project is expected to handle a large volume of transactions or support a growing number of users, scalability becomes a significant factor. Developing a scalable blockchain network may require additional resources and technology solutions, impacting the overall cost.

- Maintenance and Updates: After the initial development, ongoing maintenance and updates are necessary to keep the blockchain network secure and efficient. Regular software updates, bug fixing, and performance monitoring contribute to the long-term cost of the project.

It is essential to carefully consider these factors when estimating the cost of a blockchain project. Collaborating with a reputable blockchain development company or engaging experienced blockchain consultants can help determine an accurate cost assessment based on project requirements and objectives.

By understanding and accounting for these factors, businesses can better plan their budget and make informed decisions when embarking on a blockchain project.

Types of Blockchain Projects

Blockchain technology can be applied across various industries and use cases, resulting in different types of blockchain projects. Each type of project serves specific purposes and addresses unique challenges. Understanding the different types of blockchain projects can help businesses identify the most suitable approach for their needs. Here are some common types:

- Public Blockchains: Public blockchains, like Bitcoin and Ethereum, are open and decentralized networks accessible to anyone. They allow for transparent and permissionless participation, enabling individuals to transact and interact with the blockchain without any central authority. Public blockchains are ideal for projects that require a high level of trust and transparency.

- Private Blockchains: Private blockchains, on the other hand, are restricted and accessible only to authorized participants. These networks are often used within organizations or consortia to streamline processes, enhance data privacy, and improve efficiency. Private blockchains offer more control over the network, making them suitable for industries with specific regulatory requirements.

- Consortium Blockchains: Consortia blockchains are a hybrid approach that combines features of both public and private blockchains. They involve multiple organizations collaborating to establish and maintain a blockchain network. Consortium blockchains offer a shared infrastructure while allowing authorized participants to manage and govern the network collaboratively.

- Permissioned Blockchains: Permissioned blockchains are designed to restrict access to authorized participants only. They require permission or authentication to join the network and participate in transactions. Permissioned blockchains ensure better control over the network and are often used in enterprise settings where privacy and compliance are crucial.

- Smart Contract Platforms: Some blockchain projects are focused on providing a platform for executing smart contracts. Smart contracts are self-executing contracts with predefined conditions that automatically execute when those conditions are met. Platforms like Ethereum, NEO, and Cardano enable the development and deployment of smart contracts for various applications beyond traditional financial transactions.

- Supply Chain Blockchains: Supply chain management is an area that can greatly benefit from blockchain technology. Supply chain blockchains enable transparent tracking of products from the source to the end user, ensuring provenance, authenticity, and reducing the risk of counterfeit goods. These projects aim to simplify and secure supply chain processes.

- Identity Management Blockchains: Identity management blockchain projects seek to provide secure and decentralized solutions for managing digital identities. These blockchains enhance privacy, reduce identity theft, and enable individuals to maintain control over their personal data. They offer improved security and trust in digital identity verification.

These are just a few examples of the types of blockchain projects currently being implemented. The suitability of each type depends on the specific requirements, objectives, and industry context of the project. Businesses should carefully assess their needs and consider which type of blockchain project aligns best with their goals.

Estimating the Cost of a Blockchain Project

Estimating the cost of a blockchain project is a crucial step in the planning and budgeting process. However, determining the exact cost can be challenging due to the unique requirements and complexity of each project. Here are some factors to consider when estimating the cost of a blockchain project:

- Project Scope: The scope of the project plays a significant role in determining the cost. Projects with complex functionalities, multiple integration points, and extensive customization will generally require more time and resources, resulting in a higher cost.

- Development Team: The cost of hiring a skilled and experienced development team can vary. Factors such as location, expertise, and reputation can influence the cost. It is essential to find a team with expertise in blockchain development to ensure the successful implementation of the project.

- Technology Platforms: The choice of blockchain platform can impact the cost. Different platforms have varying development frameworks, toolkits, and support ecosystems. Consider the features, scalability, and documentation provided by the platform, as these can affect the development time and cost.

- Integration and Customization: If the blockchain project requires integration with existing systems or specific customization, the cost may increase. Integrating with external systems, such as payment gateways or IoT devices, can add complexity and require additional resources.

- Security Measures: Security is a critical aspect of any blockchain project. Implementing robust security measures, such as encryption, secure access controls, and auditing mechanisms, can increase the cost but is essential to protect against data breaches and unauthorized access.

- Testing and Quality Assurance: Rigorous testing and quality assurance are crucial for a successful blockchain project. Allocating resources and budget for comprehensive testing and quality assurance activities ensures that the project functions as intended and minimizes the risk of bugs or vulnerabilities.

- Ongoing Support and Maintenance: After the initial development, ongoing support and maintenance are necessary to keep the blockchain network secure and efficient. Regular updates, bug fixing, and performance monitoring contribute to the long-term cost of the project.

It is important to partner with a reputable blockchain development company or engage experienced blockchain consultants to ensure an accurate cost estimation. They can assess the project requirements, provide a detailed breakdown of costs, and help identify potential cost-saving measures.

Keep in mind that blockchain projects can vary significantly in terms of complexity, scale, and requirements. Therefore, it is recommended to define a clear project scope and engage in open communication with the development team to align expectations and estimate the cost accurately.

Blockchain Development Cost Breakdown

When considering the cost of blockchain development, it is important to understand the breakdown of expenses involved in the process. Although individual project requirements may vary, here is a general cost breakdown for blockchain development:

- Planning and Consultation: This stage involves understanding the project requirements, defining the scope, and consulting with blockchain experts. Costs associated with planning and consultation include project analysis, requirement gathering, and strategy formulation.

- Design and Prototyping: During this phase, the blockchain architecture is designed, and prototypes are developed to validate the concept. The cost includes activities such as system design, interface design, and creation of the minimum viable product (MVP).

- Development: The development phase involves coding the smart contracts, creating the blockchain network, and integrating the necessary features. The cost includes backend development, frontend development, and the implementation of smart contract logic.

- Integration and Customization: If the blockchain project requires integration with existing systems or specific customization, additional costs may be incurred. This includes integrating with third-party APIs, implementing required functionalities, and customizing the blockchain network as per project requirements.

- Testing and Quality Assurance: Rigorous testing is essential to ensure the reliability and security of the blockchain project. The cost includes activities such as unit testing, integration testing, security testing, and performance testing. Quality assurance measures are implemented to minimize risks and ensure smooth operation.

- Deployment and Infrastructure: The deployment phase involves launching the blockchain network and configuring the necessary infrastructure. It includes costs associated with setting up servers, databases, network nodes, and other infrastructure components required for the smooth operation of the blockchain project.

- Support and Maintenance: After the deployment, ongoing support and maintenance are crucial to keep the blockchain project updated and secure. This includes bug fixing, system upgrades, monitoring, and regular maintenance. The cost will depend on the level of support required and the complexity of the project.

It is important to note that these costs can vary depending on various factors such as project complexity, customization requirements, the size of the development team, and the technology platform chosen. Engaging with a reputable blockchain development company can provide a more accurate cost breakdown based on the specific project needs.

Proper planning, realistic budgeting, and effective project management are essential to ensure that the blockchain development process stays within budget and meets the desired objectives. Taking these factors into consideration allows for a well-informed decision-making process and a successful blockchain implementation.

The Cost of Building a Public vs Private Blockchain

When considering the cost of building a blockchain, the type of blockchain – public or private – plays a significant role in determining the expenses involved. Both public and private blockchains have distinct characteristics and cost implications. Here is a breakdown of the cost differences between building a public and private blockchain:

Public Blockchain:

Public blockchains, such as Bitcoin and Ethereum, are open and decentralized networks accessible to anyone. Building a public blockchain involves several cost factors:

- Network Setup and Infrastructure: Building a public blockchain network requires setting up a distributed network of nodes and servers. Costs associated with infrastructure, including server hardware, storage, and network components, can be significant.

- Consensus Mechanism: Public blockchains typically rely on energy-intensive consensus mechanisms such as Proof of Work (PoW) or Proof of Stake (PoS). The cost of mining equipment, electricity consumption, and network security must be considered.

- Development and Maintenance: Developing a public blockchain requires skilled developers proficient in the chosen blockchain platform’s programming language. Ongoing maintenance, including system upgrades, bug fixes, and network monitoring, adds to the overall cost.

- Community Engagement and Governance: Public blockchains thrive on community engagement. Building and maintaining an active community involves marketing, community outreach, engagement programs, and governance mechanisms. These activities come with associated costs.

Private Blockchain:

Private blockchains are restricted networks accessible only to authorized participants. The cost considerations for building a private blockchain are slightly different:

- Network Setup and Infrastructure: Deploying a private blockchain requires setting up a network infrastructure specific to the organization or consortium. The cost of servers, storage, and other infrastructure components depends on the scale and complexity of the network.

- Development and Integration: Customizing and integrating a private blockchain with existing systems and processes can add to the development cost. The level of complexity and the need for third-party integrations can affect the overall expense.

- Security and Access Controls: Private blockchains often require robust security measures, access controls, and encryption to protect sensitive information. The cost of implementing necessary security protocols and authentication mechanisms should be taken into account.

- Maintenance and Governance: Ongoing maintenance and support is necessary for a private blockchain. This includes software updates, bug fixes, and monitoring. Governance mechanisms for decision-making within the consortium may also incur additional costs.

It is important to note that the cost of building a blockchain can vary greatly depending on project-specific requirements and complexities. Engaging with experienced blockchain developers and experts can provide a more accurate cost estimation based on the specific needs of the organization or consortium.

Ultimately, whether to build a public or private blockchain depends on the use case, desired level of decentralization, regulatory considerations, and security requirements of the project. Evaluating the associated costs and benefits helps organizations make an informed decision that aligns with their goals and resources.

Hidden Costs of Blockchain Implementation

While blockchain technology offers numerous benefits, it is important to consider the hidden costs that may arise during the implementation process. These hidden costs are often overlooked but can significantly impact the overall expenses of a blockchain project. Here are some commonly encountered hidden costs:

- Infrastructure and Network Costs: Building and maintaining the necessary infrastructure for a blockchain network can be a significant expense. The cost of servers, storage systems, networking equipment, and bandwidth should be considered. Additionally, as the blockchain network grows, the need for scalability and additional resources may arise, resulting in added costs.

- Integration and Interoperability: Integrating a blockchain with existing systems and applications can be complex and time-consuming. The cost of integrating with legacy systems, third-party services, or APIs should be factored into the budget. Compatibility and interoperability challenges may require additional development efforts and resources.

- Data Storage and Management: Blockchain technology involves the storage of large amounts of data. As the blockchain network expands, the cost of storing and managing the growing volume of data can increase. Future planning for data storage and backup solutions is crucial to avoid unexpected costs.

- Security Measures: While blockchain is known for its security features, additional security measures may be required based on the specific use case. Implementing robust security protocols, audits, and regular vulnerability assessments should be factored into the budget. Ongoing security maintenance and updates are also necessary to protect the blockchain network from emerging threats.

- Regulatory Compliance: Depending on the industry and jurisdiction, there may be regulatory requirements that must be adhered to when implementing a blockchain project. Ensuring compliance with regulations and engaging legal experts to navigate any legal or regulatory complexities adds to the overall cost.

- User Adoption and Training: Blockchain projects often require user adoption and training initiatives to ensure seamless integration into existing workflows. Investing in user education and training programs can help users understand the benefits and functionalities of the blockchain and reduce resistance to change.

- Updates and Upgrades: Blockchain technology is evolving rapidly, with new features and improvements being regularly introduced. Budgeting for future updates and upgrades is essential to stay current with the latest advancements and avoid obsolescence. Failure to allocate resources for updates may result in compatibility issues or the need for costly system migrations.

Considering these hidden costs in the planning phase can help organizations better estimate the total expenses of implementing a blockchain project. Engaging with experienced blockchain consultants and development teams can provide valuable insights and guidance to identify and manage these hidden costs effectively.

It is important to take a holistic approach to budgeting and consider both the upfront costs and the long-term costs associated with the maintenance and scalability of the blockchain network. This proactive approach ensures that the implementation is financially feasible and sustainable in the long run.

Cost vs Value: Is Blockchain Worth It?

As with any technology investment, organizations must weigh the costs against the potential value when considering the implementation of blockchain. While blockchain offers numerous advantages, it is important to evaluate whether the benefits outweigh the associated costs. Here are key factors to consider when assessing the value of blockchain:

- Enhanced Efficiency and Transparency: Blockchain technology can streamline processes, reduce middlemen, and enable transparent transactions. This can lead to cost savings and increased operational efficiency. Organizations should assess how blockchain can improve existing workflows and the potential impact on productivity and cost-effectiveness.

- Improved Security and Trust: Blockchain’s distributed and immutable nature enhances data security and can reduce the risk of fraud and tampering. Evaluating the potential cost savings from mitigating security breaches, data manipulation, and unauthorized access is crucial in determining the value of blockchain implementation.

- Elimination of Intermediaries: One of the key benefits of blockchain is the removal of intermediaries in transactions. This can result in significant cost reductions for industries that rely heavily on intermediaries, such as finance and supply chain. Assessing the potential cost savings from reducing or eliminating third-party fees and processes is important in determining blockchain’s value.

- Increased Data Accuracy and Consistency: Blockchain’s decentralized and consensus-based approach ensures that all participants have access to the same, up-to-date information. This can minimize errors, disputes, and reconciliation efforts, resulting in cost savings for organizations. Evaluating the potential cost savings from improved data accuracy and reduced manual efforts is vital.

- Opportunities for New Business Models: Blockchain opens up new possibilities for innovative business models and revenue streams. Organizations should evaluate the potential revenue-generating opportunities and weigh them against the costs of implementing and maintaining the blockchain network.

While blockchain offers significant potential value, it is essential to conduct a thorough cost-benefit analysis specific to the organization’s needs and objectives. Consideration should also be given to market maturity, regulatory compliance, skill availability, and scalability requirements.

Additionally, blockchain implementations often require a long-term perspective, as the initial costs may be higher due to development, infrastructure setup, and training. Organizations must assess the return on investment over a longer timeframe rather than expecting immediate cost savings.

In some cases, the value of blockchain may be more evident for certain industries, such as finance, supply chain, healthcare, and legal sectors, where trust, security, and transparency are critical. For other industries, the potential benefits may be less pronounced, making a cost-benefit analysis even more important.

Ultimately, the decision to implement blockchain should be based on a comprehensive evaluation of the costs and potential value it can bring to the organization. By conducting thorough analysis and weighing the benefits against the costs, organizations can make informed decisions that align with their strategic goals and financial capabilities.

Conclusion

Blockchain technology has become a game-changer in various industries, offering improved security, transparency, and efficiency. However, before embarking on a blockchain project, it is crucial to assess the costs and value it can bring to an organization.

Understanding the factors that affect the cost of blockchain, such as project scope, development team, infrastructure, and maintenance, is essential for accurate budgeting and planning. Considering the hidden costs, including integration, data storage, security, and compliance, provides a more comprehensive financial picture.

In comparing the costs to the value of blockchain implementation, organizations should consider the potential benefits, such as enhanced efficiency, improved security and trust, elimination of intermediaries, increased data accuracy, and new business opportunities. Conducting a thorough cost-benefit analysis specific to the organization’s needs and industry context is crucial for informed decision-making.

Blockchain projects come in different forms, such as public, private, consortium, and identity management blockchains. Assessing the requirements and goals of the project helps determine the most suitable type of blockchain and associated costs.

Ultimately, the decision to implement blockchain should align with the organization’s strategic goals and financial capabilities. Engaging with experienced blockchain consultants and development teams can offer valuable insights and expertise, ensuring accurate cost estimates and successful implementation.

With careful evaluation, proper planning, and a clear understanding of the costs and potential value, organizations can determine whether blockchain technology is worth the investment. The transformative potential of blockchain makes it a technology worth considering for industries looking to enhance security, streamline processes, and unlock new opportunities.