Introduction

The rapid evolution of technology has transformed various industries, and the financial sector is no exception. The emergence of innovative technologies and digital solutions has given rise to the concept of financial technology, or fintech. Fintech companies leverage technology to provide efficient and user-friendly financial services, disrupting traditional banking models and revolutionizing the way we conduct financial transactions.

Fintech operates at the intersection of finance and technology, leveraging advancements in mobile technology, artificial intelligence, big data analytics, and blockchain to offer a wide array of services such as online payments, peer-to-peer lending, crowdfunding, robo-advisory, and digital currencies. These companies have gained momentum globally, attracting significant investments and gaining the trust of consumers who are seeking convenient and accessible financial services.

As fintech continues to gain prominence in the financial industry, a new trend has emerged – the expansion of fintech companies into the traditional banking sector. Fintech companies are increasingly obtaining banking licenses or partnering with existing banks to provide a broader range of services and establish themselves as digital banks. This strategic move allows them to leverage their technological expertise, customer-centric approach, and agility to compete with incumbent banks and harness the potential of a rapidly evolving digital landscape.

The rise of fintech companies entering the banking sector has raised several questions about the potential impact on traditional banking institutions and financial markets as a whole. This article will explore the implications of fintech companies becoming banks and the effects on financial markets. We will discuss the benefits and challenges of this trend, regulatory considerations for fintech companies, and the overall disruption caused by this shift.

As the financial services industry continues to evolve, it is crucial to analyze and understand the impact of fintech companies becoming banks to navigate the changing financial landscape. By exploring this topic, we can identify the potential opportunities and challenges that arise from this convergence of technology and banking, and gain insights into how financial markets are being transformed by these innovative players.

What is fintech?

Financial technology, commonly known as fintech, refers to the use of technological innovations to deliver financial services and solutions. It encompasses a wide range of products, services, and business models that leverage technology to revolutionize traditional financial processes.

Fintech aims to address the challenges and inefficiencies present in traditional banking models by leveraging advancements in areas such as mobile technology, cloud computing, artificial intelligence, big data analytics, and blockchain. These technologies enable fintech companies to streamline processes, enhance security, improve accessibility, and provide personalized services to consumers.

Fintech companies operate in various sectors within the financial industry, including banking, payments, lending, insurance, wealth management, and even regulatory compliance. They utilize technology to create user-friendly platforms, applications, and tools that enable individuals and businesses to manage their finances, make payments, access loans, invest, and protect their assets more conveniently and efficiently.

One of the key characteristics of fintech is its customer-centric approach. Fintech companies prioritize user experience and aim to address the pain points experienced by consumers when dealing with traditional financial institutions. By offering intuitive user interfaces, seamless integration with mobile devices, and personalized recommendations, fintech companies are able to deliver a superior customer experience and cater to the evolving needs and expectations of users.

Fintech has democratized financial services, making them more accessible to a wider audience. It has played a significant role in reaching underserved populations, allowing individuals without access to traditional banking services to utilize digital tools and platforms for their financial needs. This inclusivity is achieved through the use of mobile banking, digital wallets, and innovative lending solutions that leverage alternative data to assess creditworthiness.

Overall, fintech is reshaping the financial industry by challenging traditional models and introducing disruptive innovations. Its emphasis on digitalization, automation, and customer-centricity has propelled the industry forward, driving innovation and improving the overall efficiency and accessibility of financial services. Fintech is not just a buzzword, but a transformative force that continues to shape the future of finance.

The rise of fintech companies

Over the past decade, fintech companies have experienced a remarkable ascent, disrupting the traditional financial landscape and transforming the way we manage our finances. This rise can be attributed to several key factors driving the growth of the fintech sector.

Firstly, advancements in technology have provided the foundation for the rise of fintech companies. The proliferation of smartphones, increased internet connectivity, and the availability of user-friendly mobile applications have created a conducive environment for the development of innovative financial solutions. With these technological advancements, fintech companies have been able to offer convenient and accessible services to a broader audience.

Secondly, changing consumer behaviors and expectations have fueled the growth of fintech. Consumers now seek speed, convenience, and personalized experiences in their financial dealings. Fintech companies have capitalized on this by providing easy-to-use platforms, 24/7 accessibility, and tailored financial solutions. Whether it’s making payments, investing, or managing personal finances, fintech offers streamlined processes that align with the evolving needs of modern consumers.

Another factor contributing to the rise of fintech companies is the dissatisfaction with traditional financial institutions. Many consumers have grown frustrated with the complexities, high costs, and lack of transparency associated with traditional banks. Fintech companies have positioned themselves as alternatives, offering more transparent fee structures, lower costs, and innovative services that better meet the needs of consumers.

Furthermore, fintech companies have been successful in attracting investments from venture capital firms as well as partnerships with established financial institutions. These investments have provided the necessary resources and expertise to fuel the growth of fintech companies. Additionally, partnerships with traditional banks have allowed fintech companies to tap into their established customer base, regulatory knowledge, and infrastructure, facilitating their entry into the financial sector.

The rise of fintech companies has also been driven by the increasing demand for financial inclusion. Fintech offers solutions that can reach underserved populations, particularly in developing countries where access to traditional banking services is limited. Innovative mobile payment systems, micro-lending platforms, and digital wallets are enabling individuals without traditional bank accounts to participate in the formal financial system and conduct transactions securely and efficiently.

Overall, the rise of fintech companies can be attributed to the convergence of technological advancements, changing consumer expectations, dissatisfaction with traditional banks, investments and partnerships, and the drive for financial inclusion. As these companies continue to disrupt the financial industry, it is imperative for traditional institutions to adapt and collaborate with fintech in order to stay relevant and meet the evolving needs of customers.

Fintech companies entering the banking sector

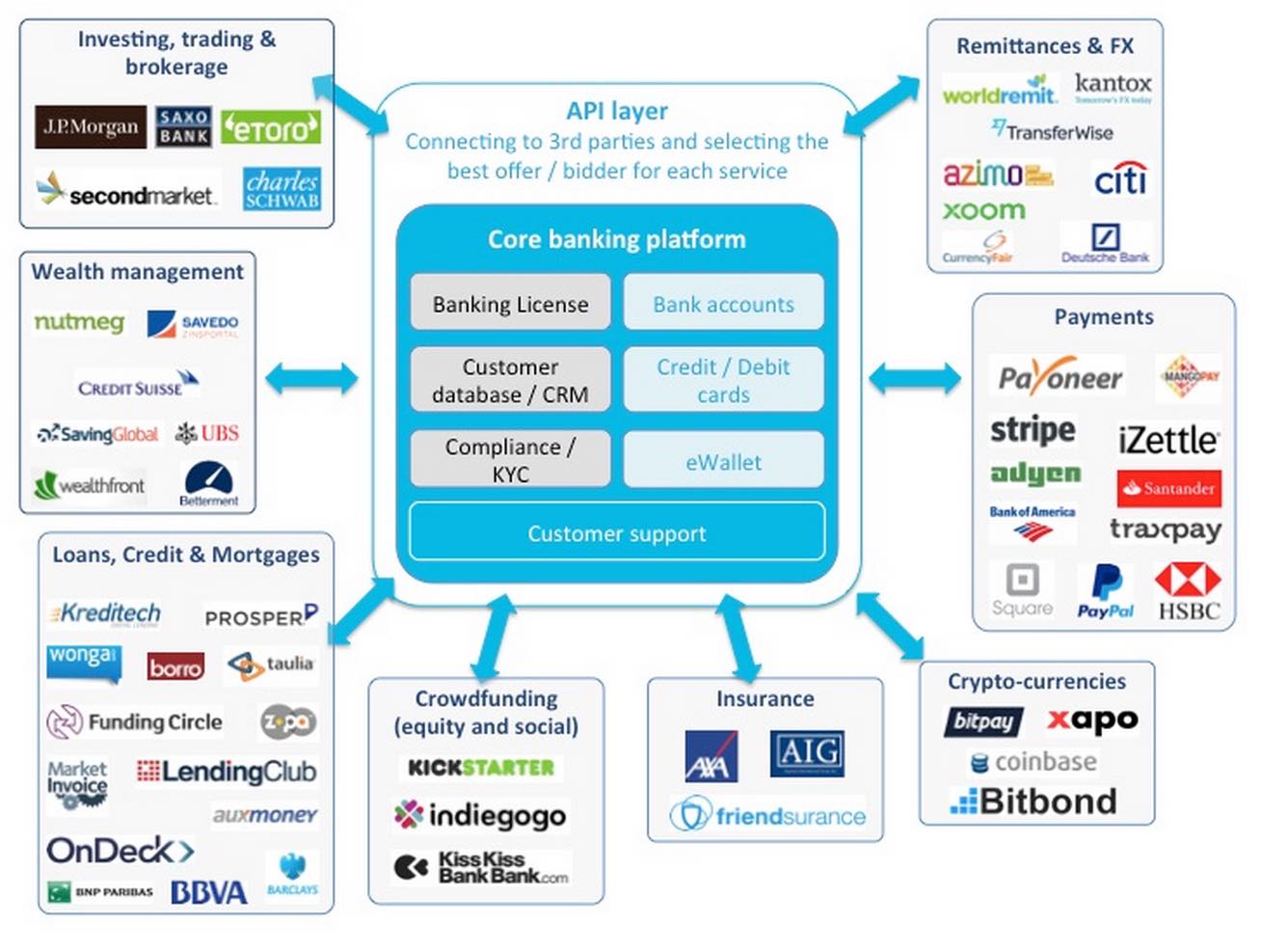

In recent years, there has been a notable trend of fintech companies entering the traditional banking sector. These companies are obtaining banking licenses or partnering with existing banks to offer a broader range of financial services. This move allows fintech companies to effectively compete with traditional banks and capitalize on their technological expertise and customer-centric approach.

By becoming banks themselves, fintech companies can expand their service offerings beyond their initial focus areas. They can provide services such as deposit accounts, loans, and other traditional banking products while leveraging their technological capabilities to offer unique and innovative solutions. This shift into the banking sector enables fintech companies to provide a more comprehensive and holistic financial experience to their customers.

One of the key advantages of fintech companies entering the banking sector is their ability to provide seamless and integrated digital banking experiences. Traditional banks have often struggled with outdated legacy systems and cumbersome processes, whereas fintech companies have developed robust and user-friendly digital platforms from the ground up. By combining their technological expertise with the banking infrastructure, fintech companies can deliver efficient and streamlined banking services that meet the expectations of today’s digital-savvy customers.

Moreover, fintech companies entering the banking sector can leverage their expertise in data analytics and artificial intelligence (AI) to offer personalized financial services. These technologies enable fintech banks to gain deeper insights into customer behavior, preferences, and financial needs, allowing them to tailor their offerings accordingly. By harnessing the power of AI-driven algorithms, fintech banks can deliver customized recommendations, automated budgeting tools, and personalized financial advice, enhancing the overall customer experience.

Another benefit of fintech companies becoming banks is their agility and ability to adapt quickly to market trends and changing consumer demands. Traditional banks are often burdened by complex regulatory requirements and bureaucratic processes that hinder their ability to innovate rapidly. Fintech banks, on the other hand, are more nimble and can quickly implement new technologies and services to meet evolving customer needs. This agility allows fintech banks to stay ahead of the competition and provide cutting-edge financial solutions.

However, there are also challenges that fintech companies face when entering the banking sector. Compliance with regulatory requirements, capitalization requirements, and establishing trust and credibility among customers are some of the hurdles they need to overcome. Additionally, traditional banks may view fintech companies as competitors and pose challenges in terms of partnerships and market access.

In summary, fintech companies entering the banking sector are expanding their service offerings, leveraging their technological expertise, and delivering innovative and customer-centric financial solutions. This trend is reshaping the banking industry and challenging traditional banks to adapt and collaborate. As fintech companies continue to disrupt the financial sector, their entry into the banking sector presents both opportunities and challenges for the industry as a whole.

The impact on traditional banking institutions

The entry of fintech companies into the banking sector has had a significant impact on traditional banking institutions. These institutions, with their established structures and legacy systems, have been forced to adapt and respond to the disruptions caused by fintech.

One of the prominent impacts is increased competition. Fintech companies, with their innovative products, user-friendly interfaces, and personalized services, have been able to attract a growing customer base. This has put pressure on traditional banks to enhance their offerings and improve the customer experience. To remain competitive, many traditional banks have had to invest in technology, revamp their digital platforms, and streamline their processes.

Furthermore, fintech companies have reshaped customer expectations. The convenience and efficiency offered by fintech services have set a new standard in the industry. Customers now expect seamless digital experiences, quick access to financial services, and personalized solutions. Traditional banks have had to re-evaluate their service delivery and ramp up their digital capabilities to meet these changing demands.

Another impact is the erosion of traditional revenue streams. Fintech companies, with their leaner operating models and lower cost structures, have presented challenges to the traditional fee-based revenue models of banks. For instance, the rise of peer-to-peer lending platforms and digital payment systems has reduced the demand for traditional banking services such as loans and payment processing. To compensate, banks have had to explore new revenue streams or collaborate with fintech companies to offer complementary services.

Moreover, the entry of fintech companies has prompted regulatory scrutiny and oversight. Financial services are highly regulated, and fintech companies entering the banking sector are subject to the same regulations as traditional banks. However, regulators have had to navigate the unique characteristics of fintech, such as data privacy concerns, cybersecurity risks, and the rapid pace of technological advancements. Striking the right balance between innovation and consumer protection has been a challenge for regulators, and this ongoing process has shaped the regulatory landscape for both fintech and traditional banks.

Nevertheless, traditional banks also have certain advantages over fintech companies. Their well-established brand recognition, extensive customer base, and deep industry knowledge give them a competitive edge. Many traditional banks have recognized the potential of fintech and have embraced collaboration with these innovative startups. Partnerships between traditional banks and fintech companies have enabled a mutually beneficial exchange of expertise, resources, and market access.

In summary, the impact of fintech companies on traditional banking institutions has been profound. Traditional banks have had to adapt to the changing landscape, invest in technology, and deliver enhanced digital experiences. The competition has intensified, revenue streams have been challenged, and regulatory frameworks have evolved. Yet, the collaboration between traditional banks and fintech companies presents opportunities for both to thrive in a rapidly evolving financial ecosystem.

The disruption of financial markets

The entry of fintech companies into the banking sector has caused significant disruption in financial markets, reshaping how financial services are delivered, and challenging traditional market players.

One of the major disruptions is the democratization of financial services. Fintech companies, with their technology-driven solutions, have opened up access to financial services for underserved populations. Digital banking services, mobile payment platforms, and alternative lending options have provided individuals and businesses with greater financial inclusion, enabling them to participate more actively in the formal economy.

Moreover, fintech has facilitated the rise of alternative financing options. Crowdfunding platforms and peer-to-peer lending sites have created new avenues for businesses and individuals to access capital. These alternative financing models have reduced reliance on traditional banking institutions, providing more options for borrowers and investors alike.

The rise of fintech has also sparked innovation in traditional financial markets. Traditional stock exchanges, for instance, have faced competition from fintech-powered investment platforms and robo-advisors. These digital platforms offer low-cost investment options, personalized portfolio management, and algorithm-driven investment recommendations, challenging the traditional model of human financial advisors.

Furthermore, the use of blockchain technology has the potential to disrupt various aspects of financial markets, particularly in areas such as remittances, clearing and settlement, and trade finance. Blockchain technology enables decentralized and transparent peer-to-peer transactions, reducing costs, increasing efficiency, and enhancing security. This technology has garnered attention from both fintech companies and traditional financial institutions, with many exploring its potential applications.

Fintech has also catalyzed the growth of digital currencies and cryptocurrencies. Cryptocurrencies such as Bitcoin and Ethereum have gained popularity as alternative forms of payment and investment. This has prompted regulators and central banks to grapple with the implications of these digital currencies on monetary policy, financial stability, and consumer protection.

Additionally, fintech companies have leveraged big data analytics to gain insights into consumer behavior and risk profiles. This data-driven approach has revolutionized risk assessment and underwriting processes, enabling more accurate and efficient credit scoring models. This has opened up avenues for alternative credit providers, allowing them to compete with traditional banks.

Overall, the disruption caused by fintech companies in financial markets is driving innovation, enhancing accessibility, and challenging traditional players. Fintech’s ability to leverage technology, offer alternative financing options, and transform traditional financial processes is reshaping the industry. As fintech continues to evolve, it will play a pivotal role in shaping the future of financial markets, with implications for both consumers and incumbent financial institutions.

Benefits and challenges of fintech companies becoming banks

The convergence of fintech and banking presents both benefits and challenges for fintech companies as they enter the banking sector.

One of the key benefits is the expanded range of services that fintech companies can offer as banks. By becoming banks themselves, fintech companies can provide a more comprehensive suite of financial offerings to their customers. This includes deposit accounts, loans, mortgages, and other traditional banking products, allowing them to address a wider range of financial needs. This expansion of services enables fintech banks to provide end-to-end financial solutions, enhancing customer convenience and increasing their competitive edge.

Additionally, the entry of fintech companies into the banking sector allows for a seamless digital banking experience. Fintech companies have demonstrated their expertise in designing user-friendly and intuitive digital platforms. By leveraging their technological capabilities in their banking operations, they can offer customers a seamless and integrated digital banking experience. This includes features such as 24/7 access, real-time updates, and personalized recommendations, creating a more convenient and personalized banking experience.

Another benefit is the potential for cost savings and operational efficiencies. Fintech companies are known for their agile and lean operational models. By applying these models to their banking operations, they can reduce costs associated with physical infrastructure and legacy systems. This cost efficiency can lead to more competitive pricing for customers, lower fees, and faster service delivery.

However, there are also challenges that fintech companies face when becoming banks. One of the major challenges is navigating the complex regulatory landscape. Traditional banking is subject to strict regulations and oversight to protect consumer interests and maintain financial stability. Fintech companies entering the banking sector must ensure compliance with these regulations, which may require significant resources and expertise. Failure to comply with regulations can lead to penalties, reputational damage, and legal repercussions.

Another challenge is building trust and credibility as a new banking entity. Traditional banks have established trust and credibility over many years, while fintech companies are relatively new players in the banking space. Fintech banks must work to gain the trust of customers who may be hesitant to switch from traditional banking institutions. This can be achieved through transparent communication, robust security measures, and reliable customer service.

Additionally, fintech banks may face challenges in attracting and retaining customers. Traditional banks have an advantage in terms of brand recognition and an established customer base. Fintech banks need to differentiate themselves through innovative, user-friendly, and competitive offerings to attract new customers. Moreover, maintaining customer loyalty in a highly competitive market requires continuous innovation and exceptional customer service.

In summary, fintech companies becoming banks can benefit from an expanded range of services, a seamless digital banking experience, and cost savings. However, they also face challenges in navigating regulations, building trust, and competing with established banks. By addressing these challenges and leveraging their technological expertise, fintech companies can successfully enter the banking sector and contribute to the ongoing transformation of the financial industry.

Regulatory considerations for fintech companies

As fintech companies venture into the banking sector, they must navigate a complex regulatory landscape to ensure compliance with applicable laws and regulations. Regulatory considerations are crucial to maintaining consumer protection, ensuring financial stability, and fostering innovation in the fintech industry.

One of the primary regulatory considerations for fintech companies is obtaining the necessary licenses and approvals to operate as a bank. Every jurisdiction has its own regulatory framework for banking activities, and fintech companies must adhere to these requirements. This includes meeting capital adequacy, liquidity, and solvency standards, as well as demonstrating the ability to mitigate operational and financial risks.

Additionally, fintech banks are subject to regulatory oversight surrounding data privacy and cybersecurity. As custodians of sensitive customer information and digital payment systems, fintech banks must comply with data protection laws and ensure robust cybersecurity measures. This includes implementing secure systems, encrypting customer data, and adhering to industry best practices to safeguard against data breaches and cyber threats.

Fintech companies must also consider anti-money laundering (AML) and know-your-customer (KYC) regulations. These regulations aim to prevent illicit activities, such as money laundering and terrorist financing, by ensuring the identification and verification of customers. Fintech banks must establish robust AML and KYC processes to detect and prevent fraudulent activities, implement transaction monitoring systems, and report suspicious transactions to regulatory authorities.

Furthermore, cross-border operations require fintech companies to navigate the regulatory frameworks of multiple jurisdictions. International transactions may be subject to additional regulations, including foreign exchange controls, trade restrictions, and cross-border data transfer regulations. Compliance with local regulations is vital to ensure a seamless and compliant cross-border operation.

Regulators have also recognized the importance of fostering innovation and providing regulatory sandboxes for fintech companies. Regulatory sandboxes offer a controlled environment for fintech companies to test their services while providing regulatory oversight and consumer protection. Participating in these sandboxes allows fintech companies to validate their business models, address regulatory concerns, and iterate their offerings before a full-scale launch.

Moreover, regulators are continuously evolving their regulatory frameworks to keep pace with the rapidly changing fintech landscape. Collaborative efforts between regulatory bodies, fintech companies, and traditional banks are aimed at striking the right balance between innovation and consumer protection. Roundtable discussions, consultations, and regulatory sandboxes facilitate dialogue and ensure that regulations remain practical, technology-neutral, and conducive to fintech innovation.

In summary, regulatory considerations are essential for fintech companies venturing into the banking sector. Compliance with licensing requirements, data privacy and cybersecurity regulations, AML and KYC obligations, and cross-border regulatory frameworks are critical to ensuring a secure and trustworthy banking environment. By actively engaging with regulatory authorities, fintech companies can contribute to the development of regulations that foster innovation, consumer protection, and financial stability.

Conclusion

The entry of fintech companies into the banking sector has reshaped the financial industry, challenging traditional banking models, and driving innovation. Fintech’s use of technology, customer-centric approach, and agility have disrupted traditional financial markets, leading to increased competition and improved accessibility to financial services.

Fintech companies have capitalized on advancements in technology to provide user-friendly platforms, personalized services, and streamlined processes. By becoming banks themselves, fintech companies can expand their service offerings, deliver seamless digital banking experiences, and offer a more comprehensive suite of financial products. This convergence of technology and banking has opened up new opportunities for financial inclusion, alternative financing options, and improved customer experiences.

Traditional banking institutions have had to adapt to the changing landscape and enhance their digital capabilities to remain competitive. Fintech’s entry into the banking sector has triggered a range of regulatory considerations, such as licensing, data privacy, cybersecurity, AML, and cross-border regulations. Addressing these challenges is crucial to ensure compliance and maintain consumer trust and financial stability.

Collaboration between fintech companies and traditional banks has become increasingly common, enabling a mutually beneficial exchange of expertise and resources. Such partnerships drive innovation, enhance customer experiences, and create opportunities for both fintech and traditional banks to thrive in the evolving financial ecosystem.

As fintech continues to evolve, it will play a pivotal role in shaping the future of financial markets. The democratization of financial services, alternative financing options, innovations in blockchain and digital currencies, and data-driven intelligence will continue to transform financial markets and redefine the way individuals and businesses engage with their finances.

In conclusion, the convergence of fintech and banking has led to groundbreaking advancements in the financial industry. Fintech companies entering the banking sector have brought about benefits such as expanded service offerings, seamless digital experiences, and cost savings. However, challenges including regulatory compliance, building trust, and competition with traditional banks need to be addressed. The ongoing collaboration and innovation between fintech companies and traditional banks will drive further disruption, shaping a more inclusive, efficient, and customer-centric financial landscape.