Introduction

Welcome to the fascinating world of blockchain technology! In recent years, blockchain has emerged as one of the most disruptive and transformative technologies across various industries. Its ability to provide transparent, secure, and decentralized transactions has garnered immense popularity and interest.

But what exactly is blockchain? How does it work? And why is it important to track transactions on the blockchain? In this article, we will delve into these questions and explore the methods and importance of transaction tracking on the blockchain.

Blockchain, at its core, is a distributed ledger technology that maintains a continuously growing list of records, or blocks, in a tamper-evident and immutable manner. Each block contains a timestamp and a cryptographic link to the previous block, forming a chain of interconnected blocks.

The decentralized nature of the blockchain eliminates the need for intermediaries or central authorities to validate and verify transactions. Instead, transactions are validated by a network of computers, known as nodes, through a consensus mechanism.

Transaction tracking on the blockchain refers to the ability to trace and follow the journey of a specific transaction within the blockchain network. It allows users to verify the authenticity, integrity, and status of a transaction without relying on a third party or centralized authority.

So why is it crucial to track transactions on the blockchain? One of the key benefits of blockchain technology is its transparency. Blockchain provides a transparent record of all transactions that have ever occurred on the network. This transparency enables users and businesses to hold one another accountable and ensures that transactions are conducted in a secure and trustworthy manner.

Furthermore, tracking transactions on the blockchain enhances the overall security and integrity of the network. By being able to track transactions, users can quickly identify and flag any suspicious or fraudulent activities, mitigating the risks associated with unauthorized access, tampering, or double-spending.

Next, we will explore the different methods available to track transactions on the blockchain, the importance of transaction tracking for businesses, the challenges and limitations of this process, and best practices for efficient transaction tracking on the blockchain.

What is Blockchain?

Blockchain is a revolutionary technology that has gained widespread attention for its potential to disrupt various industries. At its core, blockchain is a decentralized ledger that enables the secure and transparent recording of transactions across a network of computers.

Unlike traditional centralized systems where a single entity controls the ledger, blockchain distributes the ledger among multiple participants, known as nodes. Each node maintains a copy of the entire blockchain, ensuring that no single entity has complete control or authority over the data.

The fundamental concept behind blockchain is the use of cryptographic techniques to create a chain of blocks, each containing a combination of transactional data and a unique identifier. Transactions are grouped into blocks, which are then added to the existing chain in a sequential manner.

One of the key advantages of blockchain is its immutability. Once a block is added to the chain, it becomes extremely difficult to alter or tamper with the data within that block. This immutability ensures the integrity and trustworthiness of the recorded transactions.

Another distinguishing feature of blockchain is its ability to achieve consensus among the network participants without relying on a central authority. Through consensus algorithms such as Proof of Work (PoW) or Proof of Stake (PoS), nodes in the network collectively agree on the validity of transactions and the order in which they are added to the blockchain.

Blockchain technology has gained significant attention due to its application in the field of cryptocurrencies, most notably Bitcoin. Bitcoin, the first and most well-known cryptocurrency, utilizes blockchain to securely record all transactions without the need for intermediaries.

However, blockchain is not limited to cryptocurrencies. Its applications span across various industries, including finance, supply chain management, healthcare, voting systems, and more. In these industries, blockchain offers benefits such as increased transparency, reduced costs, enhanced security, and improved efficiency.

Overall, blockchain technology has the potential to fundamentally transform existing systems, business models, and interactions between individuals and organizations. Its decentralized and transparent nature provides a secure and efficient way to record and track transactions, opening up endless possibilities for innovation and disruption.

In the next section, we will explore how exactly blockchain works and the underlying mechanisms that make it such a powerful and transformative technology.

How does Blockchain work?

Blockchain, as a decentralized and secure ledger technology, operates through a series of complex mechanisms that ensure the integrity and transparency of recorded transactions. To understand how blockchain works, let’s explore its key components and processes.

At its core, a blockchain consists of a network of computers, or nodes, that participate in the transaction validation and record-keeping process. Each node holds a copy of the entire blockchain, which is continually updated through a consensus mechanism.

When a new transaction is initiated, it is broadcasted to the network and verified by multiple nodes. The verification process ensures that the transaction meets the predefined criteria, such as digital signatures, available funds, and adherence to specific rules or smart contracts.

Once verified, the transaction is grouped with other validated transactions to form a block. Every block contains a unique identifier, a timestamp, and a reference to the previous block. This chaining of blocks enables the creation of a tamper-evident and verifiable record of transactions.

But how are blocks added to the blockchain? This is where the consensus mechanism comes into play. Consensus algorithms, such as Proof of Work (PoW) or Proof of Stake (PoS), dictate how nodes in the network agree on the validity of transactions and the order in which they are added to the blockchain.

In a PoW algorithm, nodes compete to solve complex mathematical puzzles. The first node to solve the puzzle earns the right to add the next block to the blockchain. This process requires significant computational power and serves as a mechanism to prevent spamming or malicious activities on the network.

In contrast, PoS algorithms operate based on a node’s stake, or ownership, of a particular cryptocurrency. The likelihood of a node being chosen to add the next block to the blockchain is proportional to its stake. This approach aims to reduce the energy consumption associated with PoW algorithms.

Once a block is added to the blockchain, it becomes practically impossible to alter or tamper with the data within that block. Any modification to a block would require changing the corresponding data in all subsequent blocks, a computationally infeasible task due to the distributed and interconnected nature of the blockchain.

To ensure the security and decentralization of the network, blockchain also employs encryption techniques. Each transaction within a block is encrypted and linked to the previous block through a cryptographic hash function, creating a chain that is resistant to tampering.

Additionally, blockchain networks often implement mechanisms for incentivizing network participants. In the case of cryptocurrencies, participants may earn rewards, such as newly created coins, for their contributions to the network’s operation and security.

With these mechanisms in place, blockchain technology facilitates secure, transparent, and decentralized transactions. Its potential applications extend beyond cryptocurrencies, offering a robust solution for various industries seeking improved efficiency, transparency, and trust.

In the following section, we will explore the process of tracking transactions on the blockchain and why it is crucial for businesses.

Understanding transactions on the Blockchain

Transactions on the blockchain serve as the fundamental building blocks of the technology. Understanding how transactions work is essential to grasp the intricacies and benefits of blockchain technology.

A transaction on the blockchain represents the transfer of value, whether it is a monetary transaction, a digital asset exchange, or the execution of a smart contract. Each transaction contains specific information, such as the sender’s address, the recipient’s address, the amount transferred, and any additional data relevant to the transaction.

When a transaction is initiated, it undergoes a verification process to ensure its validity. This verification includes checks for digital signatures, available funds, and compliance with the predefined rules or conditions set by the blockchain network, such as smart contracts.

Once verified, the transaction is propagated to the network, where it awaits confirmation by the participating nodes. During this confirmation stage, nodes validate the transaction independently to ensure consensus on its legitimacy.

Consensus mechanisms, such as Proof of Work (PoW) or Proof of Stake (PoS), play a crucial role in determining the validity and order of transactions. PoW algorithms require nodes to solve complex mathematical puzzles to authenticate transactions, while PoS algorithms consider a node’s stake or ownership of a cryptocurrency to verify transactions.

Once consensus is reached, the validated transaction is grouped with other validated transactions and bundled together in a block. This block is then added to the blockchain. The addition of a new block requires solving mathematical puzzles or meeting specific criteria, depending on the consensus mechanism employed.

Once added to the blockchain, a transaction becomes a permanent and immutable record. It forms part of the chain of blocks and can be traced back to its origin, allowing for transparency and accountability.

It’s important to note that while transactions on the blockchain are public and transparent, the identities of the participants involved are generally pseudonymous. Instead of real names or personal information, users are identified by their unique wallet addresses, ensuring a certain level of privacy.

Furthermore, transactions on the blockchain are sequential and time-stamped. The order of transactions within a block and the subsequent blocks form a chronological ledger of activities, enabling easy tracking and verification.

By leveraging the decentralized and transparent nature of blockchain, transactions can be securely conducted without the need for intermediaries or centralized authorities. The technology ensures trust and eliminates the risk of fraudulent or tampered transactions.

In the next section, we will explore the reasons why tracking transactions on the blockchain is crucial for businesses and organizations.

Why track transactions on the Blockchain?

Tracking transactions on the blockchain is of utmost importance for various reasons. Whether you are an individual, a business, or a regulatory body, understanding the significance of transaction tracking can help ensure trust, security, and accountability within the blockchain ecosystem.

One of the primary reasons to track transactions on the blockchain is to establish transparency. Blockchain technology provides a transparent and publicly accessible ledger that records all transactions. By tracking transactions, users can verify the authenticity of transactions, ensuring that they are conducted in a fair and accountable manner.

Additionally, tracking transactions on the blockchain enhances security. The distributed and immutable nature of blockchain makes it incredibly difficult for malicious actors to tamper with or alter recorded transactions. By monitoring and tracing transactions, users can quickly detect and address any potential threats or unauthorized activities.

Transaction tracking also helps in mitigating the risks associated with fraudulent activities. By monitoring the flow of transactions on the blockchain, users can identify any suspicious patterns or unauthorized access attempts. This not only protects their own assets but also contributes to the overall security of the blockchain network.

Moreover, tracking transactions on the blockchain provides an opportunity for data analysis. The transparent nature of blockchain enables insights into transactional behavior, market trends, and user preferences. This data can be utilized by businesses for market research, targeted marketing, and strategic decision-making, leading to improved efficiency and competitive advantage.

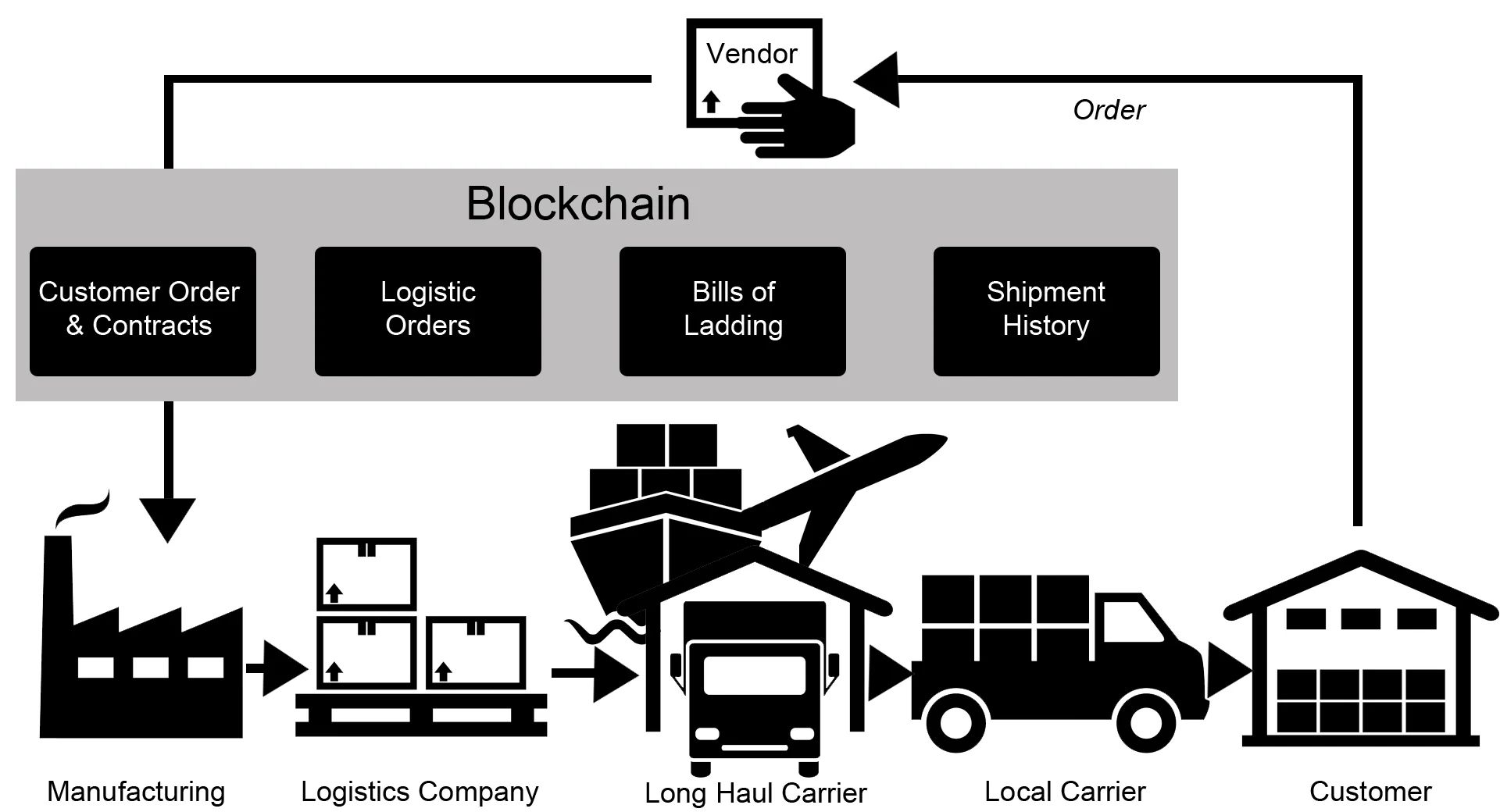

For businesses that rely on supply chains, tracking transactions on the blockchain can help ensure accountability and traceability. By recording each transaction involving the movement of goods or products, businesses can track the origin, quality, and handling of their products. This level of visibility builds trust among consumers and suppliers, as it minimizes the risk of counterfeit or substandard goods.

Furthermore, tracking transactions on the blockchain can streamline regulatory compliance. In industries such as finance, healthcare, and legal, where strict regulations are in place, monitoring transactions on the blockchain can assist in verifying compliance with regulatory requirements. This not only simplifies auditing processes but also ensures adherence to legal and industry standards.

Lastly, transaction tracking on the blockchain can facilitate dispute resolution and arbitration. Through the transparent and tamper-resistant nature of blockchain, parties involved in a transaction can refer to the recorded information to resolve any disagreements or disputes that may arise. This eliminates the need for costly and time-consuming legal procedures, providing a faster and more efficient resolution process.

In summary, tracking transactions on the blockchain is essential for establishing transparency, enhancing security, mitigating risks, enabling data analysis, ensuring supply chain accountability, simplifying regulatory compliance, and facilitating dispute resolution. It is a vital aspect of harnessing the full potential of blockchain technology.

Different methods to track transactions on the Blockchain

Tracking transactions on the blockchain can be accomplished using various methods and tools tailored to different needs and preferences. These methods provide users with the ability to monitor, analyze, and verify transactions on the blockchain network. Let’s explore some of the different approaches to tracking transactions.

1. Explorers and Block Explorers: Blockchain explorers are web-based tools or applications that allow users to search and explore transactions on the blockchain network. They provide a user-friendly interface to access transaction details, block information, and other relevant data. These explorers are commonly used for tracking transactions in popular blockchain networks like Bitcoin, Ethereum, and others.

2. Wallet Software: Many blockchain wallets include built-in transaction tracking features. These wallets provide users with real-time updates on incoming and outgoing transactions, along with details such as transaction IDs, timestamps, and wallet addresses involved. Wallet software offers a convenient way to keep track of transactions and manage digital assets securely.

3. APIs and Development Tools: Blockchain platforms often offer application programming interfaces (APIs) that developers can use to integrate transaction tracking functionalities into their applications. These APIs provide access to relevant data, allowing developers to build custom tracking tools tailored to specific requirements.

4. Blockchain Analytics Platforms: Blockchain analytics platforms utilize advanced data analysis techniques to track, visualize, and interpret on-chain transactions. These platforms provide insights into transaction patterns, addresses, and network statistics. They are commonly used for compliance monitoring, fraud detection, and market research.

5. Smart Contract Monitoring: In blockchain networks that support smart contracts, transaction tracking can be performed by monitoring the execution and outcomes of smart contracts. By monitoring the smart contract addresses and associated transactions, users can track the flow of value and the state changes triggered by contract interactions.

6. Cryptocurrency Exchanges: Cryptocurrency exchanges often provide transaction history and tracking features within their platforms. Users can view their transaction history, check the status of deposits and withdrawals, and track the movement of funds within the exchange environment.

7. Node Operations: Running a full node on the blockchain network can provide an in-depth view and control over transaction tracking. Full nodes store a complete copy of the blockchain and participate in the validation and propagation of transactions. By running a node, users can access raw transaction data, verify transactions independently, and contribute to the network’s decentralization.

It is worth noting that the availability and functionalities of transaction tracking methods may vary depending on the blockchain network and the tools being used. Additionally, the level of transaction detail and privacy may differ based on the blockchain’s design and the user’s role within the network.

Each method offers its unique advantages and limitations, and the choice of which method to use depends on the specific requirements, technical expertise, and desired level of involvement. It is essential to carefully evaluate the options and select the most suitable method for tracking transactions on the blockchain.

In the next section, we will explore the importance of transaction tracking for businesses and organizations utilizing blockchain technology.

The importance of transaction tracking for businesses

Transaction tracking is of paramount importance for businesses operating in the blockchain ecosystem. It ensures transparency, security, and accountability, enabling businesses to thrive with confidence. Let’s delve into the key reasons why transaction tracking is crucial for businesses.

1. Financial Integrity: Tracking transactions on the blockchain helps businesses maintain the integrity of their financial operations. By monitoring and verifying transactions, businesses can ensure the accurate flow of funds and identify any discrepancies or fraudulent activities. This level of financial transparency builds trust among stakeholders and safeguards the reputation of the business.

2. Regulatory Compliance: Tracking transactions on the blockchain plays a significant role in complying with regulatory requirements. Many industries, such as finance, healthcare, and supply chain, are subject to strict regulations and compliance standards. Transaction tracking allows businesses to provide auditable records and demonstrate adherence to these regulations, minimizing the risk of penalties or legal consequences.

3. Supply Chain Visibility: For businesses involved in supply chain management, transaction tracking on the blockchain brings enhanced visibility and traceability. By tracking transactions at each stage of the supply chain, businesses can identify the origin, movement, and handling of goods. This transparency minimizes the risk of counterfeiting, ensures product authenticity, and maintains quality control, ultimately leading to increased consumer trust.

4. Fraud Detection and Prevention: Transaction tracking helps businesses detect and prevent fraudulent activities on the blockchain. By monitoring transaction patterns and identifying any suspicious behavior, businesses can take immediate action to prevent potential fraud. Additionally, the immutability of blockchain ensures that once a transaction is recorded, it cannot be fraudulently altered or tampered with, providing an additional layer of security.

5. Market Analysis and Business Insights: Tracking transactions on the blockchain opens up opportunities for market analysis and business insights. By studying transaction patterns, businesses can gain valuable information about customer behavior, market trends, and demand patterns. These insights can inform strategic decision-making, marketing campaigns, and product development, enabling businesses to stay competitive and cater to the needs of their target audience.

6. Stakeholder Trust and Transparency: Transaction tracking fosters trust among stakeholders, including customers, partners, and investors. The transparent nature of blockchain, combined with the ability to track transactions, allows businesses to provide verifiable records and evidence of their activities. This transparency enhances credibility, promotes accountability, and builds long-term trust-based relationships with stakeholders.

7. Dispute Resolution: In the event of disputes or disagreements, transaction tracking on the blockchain provides an objective and auditable source of information. Being able to refer to the recorded transactions, timestamps, and parties involved simplifies the process of resolving disputes. This reduces legal costs, minimizes the need for lengthy investigations, and facilitates efficient dispute resolution.

In summary, transaction tracking is vital for businesses as it ensures financial integrity, regulatory compliance, supply chain visibility, fraud detection and prevention, market analysis, trust-building, and efficient dispute resolution. By leveraging the transparency and security of the blockchain, businesses can operate with transparency, gain valuable insights, and establish themselves as trustworthy and reliable entities in the blockchain ecosystem.

Challenges and limitations of tracking transactions on the Blockchain

While tracking transactions on the blockchain offers numerous benefits, there are also challenges and limitations that businesses and users should be aware of. Understanding these obstacles is crucial for effective transaction tracking and informed decision-making. Let’s explore some of the challenges and limitations associated with tracking transactions on the blockchain.

1. Anonymity and Pseudonymity: Blockchain transactions often utilize pseudonyms rather than real-world identities, providing a degree of anonymity. While this can be advantageous for privacy, it also presents challenges for tracking transactions and associating them with specific individuals or entities. Identifying the true parties involved in a transaction can be difficult, especially when transactions are conducted via multiple addresses or through privacy-enhancing techniques like coin mixing.

2. Scaling and Throughput: Blockchain networks face scalability challenges, particularly when it comes to transaction throughput. Public blockchains like Bitcoin and Ethereum have limited transaction processing capabilities, leading to longer confirmation times and higher fees during periods of high demand. This can hamper real-time transaction tracking and hinder the efficiency of businesses relying on blockchain technology.

3. Privacy Concerns: While blockchain technology provides a transparent and immutable ledger, certain types of sensitive data may still need protection. Privacy concerns arise when personally identifiable information or confidential business data are exposed in blockchain transactions. Striking a balance between transparency and privacy is essential, especially in industries that handle sensitive information such as healthcare or finance.

4. Fragmentation and Interoperability: The blockchain ecosystem consists of multiple networks, each with its unique structure, protocols, and standards. This fragmentation poses challenges for tracking transactions seamlessly across different blockchains. Interoperability solutions, such as cross-chain bridges or standards, are still in development, making it difficult to track transactions that occur across multiple blockchain networks.

5. Lack of Standardization: Similar to interoperability challenges, the lack of standardization in transaction tracking methods and tools creates complexities. Various blockchain networks and applications may employ different transaction structures, data formats, or APIs. This lack of standardization can hinder seamless integration and interoperability between different tracking solutions.

6. Off-Chain Transactions: Blockchain networks may involve off-chain transactions, where certain transaction details are conducted outside the underlying blockchain. These off-chain transactions can pose challenges for tracking since their details may not be immediately visible on the blockchain itself. Businesses need to consider the tracking mechanisms and tools required to capture and monitor off-chain transaction activities accurately.

7. Legal and Regulatory Compliance: While blockchain provides transparency, aligning it with existing legal and regulatory frameworks can be challenging. Different jurisdictions have varying requirements regarding transaction tracking, data storage, and privacy. Businesses need to navigate these complex legal landscapes to ensure compliance without compromising the inherent benefits of blockchain technology.

Addressing these challenges requires ongoing research, innovation, and collaboration within the blockchain community. As the technology evolves, solutions such as privacy-enhancing techniques, scalability improvements, interoperability standards, and regulatory frameworks will likely emerge to mitigate these limitations.

To effectively track transactions on the blockchain, businesses must navigate these challenges while ensuring a balance between transparency, privacy, security, and legal compliance.

Best practices for efficient transaction tracking on the Blockchain

Efficient transaction tracking on the blockchain is vital for businesses to ensure transparency, security, and accurate record-keeping. To optimize the tracking process and maximize the benefits of blockchain technology, it is essential to follow a set of best practices. Let’s explore some of these best practices for efficient transaction tracking on the blockchain.

1. Choose the Right Tracking Method: Select the most suitable transaction tracking method based on your specific requirements and the blockchain network you are operating on. Consider factors such as the level of detail needed, privacy considerations, available tools and APIs, and your technical capabilities. Whether you opt for blockchain explorers, wallet software, analytics platforms, or custom-built solutions, choose a method that aligns with your goals and resources.

2. Leverage Data Analysis Tools: Utilize blockchain analytics platforms and data analysis tools to gain valuable insights from transaction data. These tools can help identify transaction patterns, track flows of value, and analyze network statistics. By leveraging data analysis, businesses can make informed decisions, optimize processes, and identify potential risks or opportunities.

3. Implement Real-Time Tracking: Implement real-time transaction tracking to stay updated with the latest transaction activities. Explore solutions that provide live transaction notifications, allowing businesses to monitor and respond to transactions promptly. Real-time tracking enables effective fraud prevention, dispute resolution, and timely decision-making.

4. Strengthen Network Security: Prioritize network security measures to protect your transactions and data. Implement robust encryption, multi-factor authentication, and access control mechanisms to safeguard your blockchain network. Regularly update and patch software to address any vulnerabilities. Ensure that all participants in the network adhere to security practices and maintain awareness of emerging threats.

5. Ensure Regulatory Compliance: Stay informed about the legal and regulatory requirements relevant to your industry and location. Develop internal protocols and mechanisms to ensure compliance with data protection and privacy regulations. Consider deploying privacy-enhancing techniques, where applicable, to maintain a balance between transparency and privacy requirements. This ensures that your transaction tracking process aligns with legally mandated guidelines.

6. Embrace Interoperability Solutions: As the blockchain ecosystem evolves, interoperability solutions are becoming increasingly important. Explore interoperability protocols, cross-chain bridges, or standardized APIs to seamlessly track transactions across different blockchain networks. By embracing interoperability, businesses can overcome the challenges of fragmentation and enhance efficiency in transaction tracking.

7. Stay Educated and Adapt: Continuously stay up-to-date with the latest advancements, best practices, and emerging technologies in the blockchain space. Blockchain technology is evolving rapidly, and staying informed about new developments will help you adapt your transaction tracking processes accordingly. Active participation in industry forums, conferences, and communities contributes to knowledge sharing and fosters collaboration.

8. Regularly Audit and Review: Conduct regular audits and reviews of your transaction tracking processes to ensure accuracy, reliability, and efficiency. Regularly test your tracking tools and mechanisms to identify any potential issues or gaps. Additionally, periodically reassess your tracking requirements and make adjustments as necessary to meet evolving business needs or regulatory changes.

By following these best practices, businesses can enhance the efficiency and effectiveness of their transaction tracking on the blockchain. Efficient tracking ensures accurate record-keeping, enhances transparency and security, facilitates compliance, and enables businesses to make informed decisions based on reliable and up-to-date transaction data.

Conclusion

Transaction tracking on the blockchain is a critical aspect of harnessing the benefits of this transformative technology. By monitoring, analyzing, and verifying transactions, businesses can ensure transparency, security, and accountability in their operations. The decentralized and transparent nature of blockchain allows for efficient and reliable tracking, providing numerous advantages for businesses across various industries.

Throughout this article, we have explored what blockchain is and how it works, the importance of transaction tracking, different methods to track transactions on the blockchain, the significance for businesses, challenges and limitations, and best practices for efficient tracking.

Transaction tracking enables businesses to maintain financial integrity, comply with regulatory requirements, enhance supply chain visibility, detect and prevent fraud, gain valuable market insights, build trust with stakeholders, and facilitate dispute resolution. It empowers businesses to operate with transparency, efficiency, and accountability in the blockchain ecosystem.

However, it is important to be aware of the challenges and limitations associated with transaction tracking. Issues such as anonymity, scalability, privacy concerns, fragmentation, and legal compliance need to be considered and carefully addressed.

By following the best practices outlined in this article – choosing the right tracking method, leveraging data analysis tools, implementing real-time tracking, strengthening network security, ensuring regulatory compliance, embracing interoperability, staying educated and adaptable, and regularly auditing and reviewing – businesses can maximize the efficiency and accuracy of their transaction tracking processes.

As blockchain technology continues to evolve, it is crucial for businesses to stay informed and adapt their transaction tracking strategies accordingly. Collaboration and innovation within the blockchain community will drive the development of solutions to bridge existing gaps and overcome challenges.

In conclusion, transaction tracking on the blockchain is not only a necessity but also an opportunity for businesses to foster transparency, security, and trust. By embracing effective transaction tracking practices, businesses can unlock the full potential of blockchain technology and position themselves for success in the digital economy.