Understanding Algorithmic Trading

Algorithmic trading, also known as algo trading, is the process of using computer programs or algorithms to automate trading activities in financial markets. It involves the use of predefined sets of rules and instructions to execute trades with high speed and accuracy. By leveraging advanced mathematical models and historical data analysis, algorithmic trading aims to take advantage of market opportunities and generate profits.

Algorithmic trading has become increasingly popular in recent years due to its ability to execute trades at a faster pace than human traders. It eliminates human emotions and biases from the trading process, which can often lead to poor decision-making. With algorithmic trading, trades can be executed in milliseconds, allowing investors to take advantage of even the smallest market fluctuations.

One of the key advantages of algorithmic trading is its ability to automate repetitive tasks, such as order placement and trade execution. This frees up human traders to focus on more strategic activities, such as developing new trading strategies and analyzing market trends.

To successfully navigate the world of algorithmic trading, it is important to have a solid understanding of financial markets and trading principles. This includes knowledge of different asset classes, such as stocks, bonds, commodities, and currencies, as well as an understanding of various trading strategies and risk management techniques.

Additionally, it is crucial to stay up-to-date with the latest technological advancements in trading platforms and market data analysis tools. This includes familiarity with programming languages such as Python or C++, as well as proficiency in data analysis and statistical modeling.

It is also important to note that algorithmic trading is not without risks. While it can greatly increase the speed and efficiency of trading, it is still subject to market volatility and unforeseen events. Therefore, it is essential to continuously monitor and adjust algorithms to ensure they are aligned with market conditions.

In summary, algorithmic trading is a powerful tool that leverages computer programs and mathematical models to automate trading activities. With its ability to execute trades at high speeds and eliminate human emotions from the decision-making process, algorithmic trading has revolutionized the financial markets. However, it is important to approach algorithmic trading with a solid understanding of financial markets, trading principles, and risk management techniques to maximize its potential and mitigate risks.

Choosing the Right Trading Strategy

Choosing the right trading strategy is a critical step in algorithmic trading. It involves identifying a set of rules and techniques that will guide your trading decisions and help you achieve your financial goals. With numerous trading strategies available, it is important to consider several factors before making a decision.

The first factor to consider is your risk tolerance. Different trading strategies carry varying levels of risk. Some strategies, such as trend following or momentum trading, may be more aggressive and suitable for traders willing to take higher risks. On the other hand, strategies like mean reversion or arbitrage focus on low-risk opportunities. It is essential to assess your risk appetite and choose a strategy that aligns with your comfort level.

Another important factor is your trading timeframe. Are you looking for short-term opportunities or do you prefer a longer-term trading approach? Scalping and day trading strategies are suitable for those who prefer quick trades and frequent market analysis. Conversely, swing trading or position trading strategies are better suited for traders with a longer investment horizon.

Market conditions and the characteristics of the asset you are trading also play a significant role in strategy selection. Some strategies perform better in trending markets, while others excel in ranging or volatile markets. It is important to assess market conditions and choose a strategy that is expected to perform well under those conditions.

Furthermore, your trading style and personality should be taken into account. Are you comfortable with fast-paced trading or do you prefer a more patient and disciplined approach? Some traders thrive on high-frequency trading, while others may prefer a more relaxed trading style. Understanding your personal preferences and aligning them with a suitable strategy can greatly improve your chances of success.

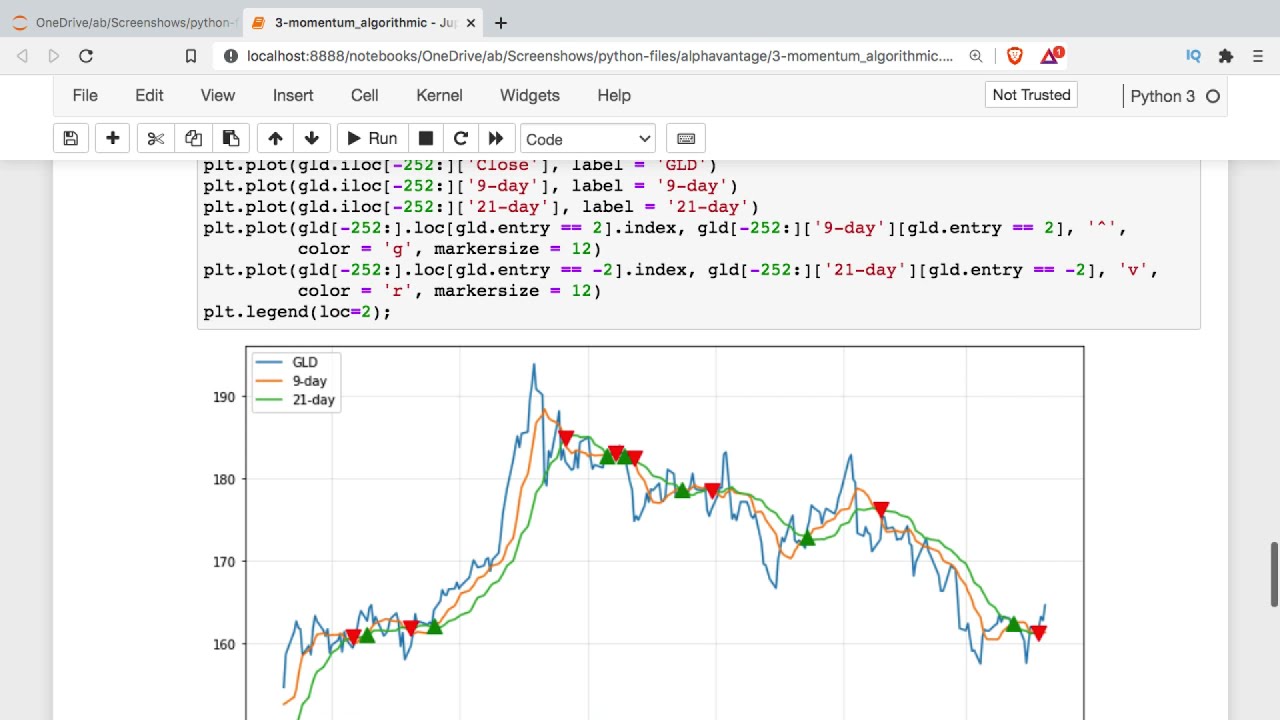

Evaluating and comparing different strategies is essential before making a final decision. Backtesting, which involves running historical data through the strategy to assess its performance, is a widely used method. It enables traders to simulate their strategy’s historical performance, identify potential weaknesses, and make necessary adjustments.

Additionally, it can be beneficial to consult industry experts and seek advice from experienced traders. Engaging in trading communities or joining online forums can provide valuable insights and help you make informed decisions.

Choosing the right trading strategy requires careful consideration of various factors, including your risk tolerance, trading timeframe, market conditions, personal preferences, and performance evaluation through backtesting. By taking the time to select a strategy that is well-suited to your goals and aligns with your trading style, you increase the likelihood of achieving success in algorithmic trading.

Gathering and Analyzing Market Data

Gathering and analyzing market data is a crucial part of algorithmic trading. The quality and accuracy of the data you use can greatly impact the performance and profitability of your trading strategy. Here, we will explore the importance of data in algorithmic trading and the steps involved in gathering and analyzing it.

First and foremost, it is essential to have access to reliable and comprehensive market data. This includes price data, volume data, news feeds, and other relevant information. There are various sources available to obtain market data, including financial data providers, online platforms, and exchanges themselves.

Once you have obtained the necessary data, the next step is to clean and preprocess it. Raw market data often contains errors, outliers, and missing values. Therefore, it is crucial to clean the data by removing anomalies and filling in missing values. This ensures that your analysis is based on accurate and complete information.

After cleaning the data, the next step is to organize and structure it for analysis. This may involve aggregating data into specific time intervals, such as minutes, hours, or days, depending on your trading strategy. Data organization is important to identify patterns, trends, and correlations that can be used to develop trading models.

Once the data is organized, the next step is to analyze it using various statistical and mathematical techniques. This may include calculating moving averages, volatility measures, price patterns, or other indicators relevant to your trading strategy. The goal is to gain insights into the market dynamics and identify potential trading opportunities.

In addition to traditional data analysis methods, machine learning and artificial intelligence techniques can also be applied to market data. These advanced techniques can uncover complex patterns and relationships that may not be immediately apparent through traditional analysis. Machine learning models can be trained to predict future market movements, identify anomalies, or classify market conditions.

Furthermore, it is important to continuously update and refresh your market data. Financial markets are dynamic and constantly evolving. New information, events, and market conditions can significantly impact trading strategies. Regularly updating your data allows you to adapt to changing market dynamics and ensure the accuracy and relevance of your analysis.

Lastly, it is crucial to have a robust data management system in place. This includes securely storing and backing up your data, as well as implementing data governance and data security measures. As market data is a valuable asset, protecting it from unauthorized access or loss is of utmost importance.

To sum up, gathering and analyzing market data is a vital step in algorithmic trading. Access to reliable and comprehensive data, proper cleaning and preprocessing, organizing and structuring the data, applying statistical and mathematical techniques, utilizing advanced technologies like machine learning, and maintaining a robust data management system are all key factors for successful data analysis. By effectively analyzing market data, traders can gain valuable insights and enhance the performance of their algorithmic trading strategies.

Developing a Mathematical Model

In algorithmic trading, developing a robust mathematical model is a key step in creating a successful trading strategy. A mathematical model provides a framework for making trading decisions based on historical data, market indicators, and statistical analysis. In this section, we will explore the importance of developing a mathematical model and the steps involved in this process.

The first step in developing a mathematical model is to define the objective of your trading strategy. What specific goals do you want to achieve? This could range from maximizing returns, minimizing risk, or a combination of both. Defining a clear objective helps guide the development process and ensures that the model aligns with your desired outcomes.

Next, it is important to select the appropriate variables and inputs for your model. These variables could include price data, volume data, technical indicators, economic indicators, or any other relevant data points. The selection of variables should be based on their relevance to the objective of your strategy and their ability to provide predictive power.

Once the variables are identified, the next step is to determine the mathematical functions and algorithms that will be used to analyze and interpret the data. This could involve statistical regression models, time series analysis, machine learning algorithms, or any other mathematical techniques that are suitable for your trading strategy.

After defining the mathematical functions, the model needs to be calibrated and optimized using historical data. This involves adjusting the model’s parameters and fine-tuning the algorithms to improve its performance. The calibration process helps validate the model’s effectiveness and ensures that it can make accurate predictions and generate profitable trading signals.

It is important to note that the process of developing a mathematical model is iterative. It requires continuous monitoring, evaluation, and refinement. As new data becomes available and market conditions change, the model may need to be adjusted or updated to adapt to the evolving market dynamics.

Moreover, it is essential to validate the mathematical model using out-of-sample data or through backtesting. This involves testing the model’s performance using data that was not used in the development process. By doing so, you can assess the model’s robustness and its ability to perform in real-world trading scenarios.

Lastly, it is crucial to understand the limitations of the mathematical model. No model is perfect, and there will always be uncertainties in the financial markets. It is important to acknowledge and account for these limitations in the decision-making process and implement risk management strategies to mitigate potential losses.

In summary, developing a mathematical model is a crucial step in algorithmic trading. Through a systematic and iterative process, traders can define their objectives, select relevant variables, choose appropriate mathematical techniques, calibrate and optimize the model, validate its performance, and account for its limitations. By developing a robust mathematical model, traders can enhance the effectiveness and profitability of their algorithmic trading strategies.

Implementing the Model into Code

After developing a mathematical model for your algorithmic trading strategy, the next step is to implement the model into code. This involves translating the mathematical concepts and rules into a programming language that can be executed by a computer. In this section, we will explore the importance of implementing the model into code and the steps involved in this process.

The implementation of the model into code allows for automation and real-time execution of your trading strategy. By coding the model, you can create a program that can analyze market data, make trading decisions, and execute trades automatically, without the need for manual intervention.

The first step in implementing the model into code is to select a programming language. Popular choices for algorithmic trading include Python, Java, C++, and MATLAB. The programming language should be compatible with the mathematical functions and algorithms used in the model and offer the necessary libraries and frameworks for data analysis and backtesting.

Once the programming language is chosen, the next step is to break down the model into smaller components or modules. This involves identifying the different parts of the model, such as data preprocessing, signal generation, risk management, and trade execution. Breaking down the model into modules helps create a modular and scalable code structure.

Each module can then be implemented by writing the necessary code. This may involve defining functions, classes, or methods that perform specific tasks within the trading strategy. It is important to write clean, well-organized, and readable code that can be easily understood and maintained.

In addition to implementing the model itself, it is crucial to handle data feeds and connectivity to the market. This includes setting up data feeds to receive real-time market data, establishing a connection to execute trades through a broker or exchange, and handling any necessary authentication or security protocols.

Furthermore, it is important to incorporate error handling and exception handling mechanisms into the code. This helps to handle unexpected errors, data inconsistencies, or network issues that may arise during the execution of the trading strategy. By implementing robust error handling, you can ensure the stability and reliability of your algorithmic trading system.

Once the code is implemented, it should be thoroughly tested to ensure its accuracy and functionality. This involves conducting extensive testing and debugging to identify and fix any errors or bugs in the code. It is advisable to perform both unit testing, which tests individual components, and integration testing, which tests the system as a whole.

Finally, documenting the code is essential for future references and troubleshooting. Clear and detailed documentation should be provided, explaining the purpose and functionality of each component, as well as providing usage instructions for other users or collaborators.

In summary, implementing the model into code is a critical step in algorithmic trading. By translating the mathematical model into a computer program, you can automate the execution of your strategy, analyze real-time market data, and make trading decisions without manual intervention. By following a systematic approach, selecting an appropriate programming language, breaking down the model into modules, writing clean and readable code, handling data feeds and connectivity, incorporating error handling mechanisms, testing the code, and documenting the implementation, you can create a robust and efficient algorithmic trading system.

Testing the Algorithm

Testing the algorithm is a crucial step in algorithmic trading. It allows traders to assess the performance, accuracy, and robustness of their trading strategy before deploying it in real-world trading scenarios. In this section, we will explore the importance of testing the algorithm and the key steps involved in this process.

The first step in testing the algorithm is to conduct thorough historical data testing or backtesting. This involves running the algorithm on past market data to simulate its performance and evaluate its profitability. Backtesting helps traders understand how the algorithm would have performed in different market conditions and identify any potential weaknesses or flaws.

During backtesting, it is important to use a sufficient amount of historical data to obtain statistically significant results. This includes using a wide range of market environments, including different market cycles, volatility levels, and economic conditions. By testing the algorithm on diverse historical data, traders can gain a better understanding of its performance under various scenarios.

In addition to historical data testing, it is crucial to perform forward testing or paper trading. This involves running the algorithm on live market data but without actual capital at risk. Forward testing allows traders to assess the real-time performance of the algorithm and identify any discrepancies or issues that may not have been captured during backtesting.

During the testing phase, it is important to carefully monitor the performance metrics of the algorithm. These metrics may include measures such as profitability, risk-adjusted returns, maximum drawdown, success rate of trades, and other relevant performance indicators. By tracking and analyzing these metrics, traders can assess the effectiveness of the algorithm and make informed decisions about its deployment.

Furthermore, it is important to conduct stress testing or sensitivity analysis. This involves subjecting the algorithm to extreme market conditions or parameter variations to evaluate its resilience and robustness. Stress testing helps traders understand how the algorithm performs under adverse circumstances and identify any potential vulnerabilities that may need to be addressed.

Another aspect of testing the algorithm is to assess its performance against benchmark indices or other trading strategies. This helps traders determine whether the algorithm outperforms standard market benchmarks or other commonly used strategies. By benchmarking the algorithm’s performance, traders can gain insights into its competitive advantage and evaluate its potential profitability.

Lastly, it is important to keep a record of the results and lessons learned during the testing process. This includes documenting any modifications or adjustments made to the algorithm based on the testing outcomes. Keeping a detailed record helps in refining the algorithm, enhancing its performance, and maintaining a comprehensive historical record for future analysis.

In summary, testing the algorithm is a critical step in algorithmic trading. Through thorough historical data testing, forward testing, monitoring performance metrics, conducting stress testing, benchmarking performance, and maintaining records, traders can assess the algorithm’s performance, identify weaknesses, and make informed decisions about its deployment. By rigorously testing the algorithm, traders can increase the likelihood of success in algorithmic trading.

Evaluating and Adjusting the Algorithm

Evaluating and adjusting the algorithm is a crucial step in the algorithmic trading process. This iterative process involves continuously monitoring and assessing the algorithm’s performance, identifying areas for improvement, and making necessary adjustments to enhance its effectiveness. In this section, we will explore the importance of evaluating and adjusting the algorithm and the key steps involved in this process.

The first step in evaluating the algorithm is to define the performance metrics that will be used to assess its effectiveness. This could include metrics such as profitability, risk-adjusted returns, maximum drawdown, or any other relevant performance indicators. By establishing clear performance benchmarks, traders can objectively evaluate the algorithm’s performance.

Regular monitoring of the algorithm’s performance is essential to identify any deviations or underperformance. This involves analyzing the performance metrics over time and comparing them to the defined benchmarks. By closely monitoring the algorithm, traders can spot potential issues or weaknesses that may need to be addressed.

When evaluating the algorithm’s performance, it is important to consider the broader market conditions and external factors that may impact its results. This includes assessing the performance in different market environments, such as trending, ranging, or volatile markets. By evaluating the algorithm’s performance in various market conditions, traders can gain insights into its robustness and adaptability.

If the evaluation indicates areas for improvement, it is necessary to make adjustments to the algorithm. This could involve modifying the parameters, rules, or variables used in the algorithm’s calculations. Adjustments may also include fine-tuning risk management techniques or incorporating new market data sources. The goal is to optimize the algorithm’s performance and align it with the desired goals.

When making adjustments to the algorithm, it is crucial to carefully test and evaluate the impact of the changes. This can be done through further backtesting and forward testing to assess how the adjustments affect the algorithm’s performance. Rigorous testing helps traders verify the effectiveness of the adjustments and ensure that they contribute to improved performance.

Additionally, it is important to consider the impact of transaction costs, such as commissions and slippage, when evaluating the algorithm’s performance. These costs can significantly affect profitability and should be factored into the performance analysis. Traders should evaluate the algorithm’s performance net of transaction costs to get a more accurate assessment of its profitability.

Regularly documenting and tracking the adjustments made to the algorithm is essential for future analysis and evaluation. This helps maintain a record of the changes implemented, their impact on the algorithm’s performance, and any lessons learned throughout the process. Documentation provides insights into the evolution of the algorithm and aids in the continuous improvement of its effectiveness.

In summary, evaluating and adjusting the algorithm is a fundamental aspect of algorithmic trading. By monitoring the algorithm’s performance, comparing it to defined benchmarks, making necessary adjustments, and thoroughly testing and evaluating the impact of changes, traders can enhance the algorithm’s effectiveness and adapt it to evolving market conditions. Through a continual process of evaluation and adjustment, traders can maximize the potential profitability and success of their algorithmic trading strategy.

Backtesting and Historical Data Analysis

Backtesting and historical data analysis are integral components of algorithmic trading. Backtesting involves simulating the performance of a trading strategy using historical market data to evaluate its potential profitability and effectiveness. In this section, we will explore the importance of backtesting and historical data analysis and discuss the key steps involved in this process.

The first step in backtesting is to gather reliable historical market data. This includes price data, volume data, and any other relevant data points that are necessary for the trading strategy. The quality and accuracy of the historical data play a significant role in the credibility of the backtesting results.

Once the data is collected, the next step is to define the specific time period to be used for backtesting. Traders should select a sufficiently long period that represents diverse market conditions and includes periods of volatility, trending markets, and range-bound markets. This helps assess the performance of the strategy across different market scenarios.

The historical data is then used to simulate the execution of the trading strategy. This involves applying the strategy’s rules, indicators, and parameters to historical data and generating trading signals and positions as if the strategy were being executed in real-time. The simulated trades are compared with the actual market data during that period to evaluate the strategy’s performance.

During backtesting, it is important to account for transaction costs, such as commissions and slippage. These costs can significantly impact the profitability of a trading strategy and should be factored into the calculations. By incorporating transaction costs into the backtesting process, traders can get a more accurate representation of the strategy’s true performance.

Through historical data analysis, traders can gain insights into the strategy’s profitability, risk, and other performance metrics. It allows for a comprehensive assessment of the strategy’s potential strengths and weaknesses. By analyzing the performance across different time periods and market conditions, traders can identify any patterns or correlations that may help refine the strategy or uncover areas for improvement.

It is important to exercise caution when interpreting the results of backtesting. While backtesting provides valuable insights into the strategy’s historical performance, it does not guarantee future success. Market dynamics and conditions can change over time, and past performance may not necessarily be indicative of future returns. Traders should use backtesting as a tool to understand the strategy’s potential and guide further analysis and adjustments.

Additionally, it is essential to conduct sensitivity analysis during backtesting. This involves testing the strategy’s performance under different parameter settings, market conditions, or data variations. Sensitivity analysis helps assess the robustness and stability of the strategy, as well as identify optimal parameter values that maximize performance.

Lastly, documenting the results of the backtesting process is crucial for future reference and analysis. Traders should maintain a record of the backtesting parameters, assumptions, and results to have a comprehensive historical log of the strategy’s evolution. Documentation aids in understanding the strategy’s performance and facilitates the continuous improvement of the trading system.

In summary, backtesting and historical data analysis provide valuable insights into the potential profitability and effectiveness of a trading strategy. By simulating the strategy’s performance using historical market data, traders can assess its performance metrics, identify areas for improvement, and conduct sensitivity analysis. However, it is important to keep in mind that backtesting results are not a guarantee of future success, and constant monitoring and adjustment are necessary to adapt to evolving market conditions.

Deploying the Algorithm in Real-Time Trading

Deploying the algorithm in real-time trading is a critical step in algorithmic trading. After thorough testing and analysis, traders are ready to put their algorithm into action and execute trades in live market conditions. In this section, we will explore the importance of deploying the algorithm and discuss the key considerations and steps involved in this process.

The first consideration when deploying the algorithm is to choose a reliable trading platform or system that supports the execution of algorithmic trades. The platform should provide robust and fast order execution capabilities, real-time market data feeds, and connectivity to relevant brokers or exchanges.

Before executing trades, it is essential to ensure that the algorithm is properly integrated with the chosen trading platform. This includes setting up the necessary connections, configuring data feeds, and establishing the appropriate interfaces for order submission and trade execution.

During the deployment process, it is crucial to monitor the algorithm carefully and regularly. This involves observing its performance in real-time, monitoring trades executed, and analyzing the results. Real-time monitoring helps identify any issues or unexpected behaviors, allowing for prompt adjustments or modifications if needed.

Risk management is a crucial aspect of deploying the algorithm. Traders should define and implement appropriate risk management measures to protect capital and mitigate potential losses. This may include setting stop-loss orders, position sizing policies, or other risk control mechanisms to limit downside exposure.

To ensure the algorithm’s stability and reliability, ongoing performance evaluation is necessary. Continuous monitoring of performance metrics and comparing them against desired benchmarks helps traders assess the effectiveness of the algorithm and make data-driven decisions to optimize its performance.

Additionally, it is important to remain vigilant and adapt the algorithm in response to changing market conditions. Markets are dynamic and can evolve over time, and strategies that were once successful may become obsolete. Regularly evaluating market trends, adjusting parameters, or exploring new trading opportunities can help enhance the algorithm’s performance and keep it aligned with current market dynamics.

Traders should also consider the potential impact of market liquidity and slippage when deploying the algorithm. Slippage is the difference between the expected execution price and the actual executed price due to market volatility or order book depth. Evaluating and managing slippage is crucial to accurately assess the algorithm’s performance and potential profitability.

Lastly, documenting execution logs and maintaining a record of trades is important for accountability and analysis. This includes documenting trading activities, positions opened and closed, as well as any adjustments or modifications made to the algorithm during live trading. Proper documentation helps create a comprehensive trade history and aids in performance analysis and compliance with regulatory requirements.

In summary, deploying the algorithm in real-time trading requires careful preparation, integration with a reliable trading platform, continuous monitoring and evaluation, risk management implementation, adaptation to changing market conditions, consideration of slippage and liquidity, and diligent documentation of trading activities. By effectively deploying the algorithm, traders can capitalize on market opportunities, execute trades efficiently, and potentially generate profits.

Monitoring and Maintaining the Algorithm

Monitoring and maintaining the algorithm is a crucial aspect of successful algorithmic trading. After deploying the algorithm, it is essential to continuously monitor its performance, ensure its stability and reliability, and make necessary adjustments to optimize its effectiveness. In this section, we will explore the importance of monitoring and maintaining the algorithm and discuss the key considerations and steps involved in this process.

One of the primary considerations in monitoring the algorithm is real-time performance monitoring. Traders should closely monitor the algorithm’s performance metrics, including profitability, risk-adjusted returns, and other relevant indicators. This helps assess whether the algorithm is performing as intended and allows traders to make informed decisions based on its real-time performance.

Regular monitoring is also important to detect any issues or anomalies in the algorithm’s behavior. Traders should be vigilant in identifying any potential malfunctions, data discrepancies, or technical issues that may impact the algorithm’s performance. Proactive monitoring allows for quick troubleshooting and rectification, ensuring the algorithm operates smoothly.

Risk management is an ongoing concern when monitoring and maintaining the algorithm. Traders should regularly assess the effectiveness of their risk management measures and consider adjustments based on changes in market conditions or trading patterns. This includes reviewing position sizing, stop-loss levels, and other risk control mechanisms to ensure the algorithm is appropriately managing risk.

Market conditions can change rapidly, and traders must continuously evaluate the algorithm’s suitability in evolving market environments. This involves analyzing the algorithm’s performance under different market scenarios, such as varying levels of volatility or shifts in market trends. The insights gained from this evaluation help determine if any adjustments or modifications are necessary to maintain the algorithm’s profitability.

Maintaining the algorithm also includes regular review and optimization of its parameters and rules. Traders should periodically evaluate the effectiveness of the algorithm’s settings and consider adjustments based on the analysis of historical and real-time performance data. This continuous optimization helps keep the algorithm aligned with changing market dynamics and enhances its performance.

Data quality is another critical aspect to address when monitoring and maintaining the algorithm. Traders should ensure that the market data used by the algorithm remains accurate, complete, and up to date. This may involve periodically reviewing data sources, making adjustments to data feeds, or acquiring additional data as needed to maintain the algorithm’s performance integrity.

Compliance and regulatory considerations should not be overlooked when monitoring and maintaining the algorithm. Traders should stay updated on relevant regulations and ensure that the algorithm and its trading activities comply with legal requirements. This may involve periodic internal audits, documentation of compliance procedures, and staying informed about any regulatory changes that may impact algorithmic trading practices.

Maintaining a comprehensive record of the algorithm’s activities, adjustments, and performance is vital for performance analysis and future optimizations. Traders should maintain trade logs, performance reports, and any other relevant documentation. This historical record helps track the algorithm’s evolution, aids in the assessment of its effectiveness, and facilitates compliance with reporting requirements, if applicable.

In summary, monitoring and maintaining the algorithm is essential for successful algorithmic trading. Continuous monitoring of performance, proactive troubleshooting, risk management evaluation, adaptation to changing market conditions, optimization of parameters and rules, data quality assurance, compliance considerations, and comprehensive documentation are all integral to effectively monitor and maintain the algorithm. By actively monitoring and maintaining the algorithm, traders can optimize its performance, adapt to market conditions, and increase the likelihood of success in algorithmic trading.

Risks and Challenges in Algorithmic Trading

Algorithmic trading offers numerous benefits, but it also comes with its fair share of risks and challenges. Traders must be aware of these potential pitfalls to effectively navigate the world of algorithmic trading. In this section, we will explore the key risks and challenges involved in algorithmic trading.

One of the primary risks in algorithmic trading is the risk of technical failures. The reliance on technology and automation leaves algorithms vulnerable to system crashes, connectivity issues, or data feed disruptions. These technical failures can lead to missed trading opportunities, incorrect order executions, or other undesirable outcomes. To mitigate this risk, traders should employ robust technical infrastructure, redundant systems, and backup resources.

Market risk is another significant concern. Algorithms operate in dynamic and unpredictable markets, and unexpected events can cause market volatility or disruptions that impact trading strategies. Changes in government regulations, geopolitical events, macroeconomic factors, or sudden shifts in investor sentiment can all contribute to increased market risk. Traders must carefully monitor market conditions and adapt their algorithms to changing dynamics to mitigate this risk.

Data quality and accuracy is a critical challenge in algorithmic trading. Algorithms rely on historical and real-time market data to make trading decisions. If the data used is incorrect, incomplete, or outdated, it can lead to erroneous trading signals or incorrect analysis. It is vital for traders to have reliable data sources and robust data validation processes in place to ensure the accuracy of the data used by algorithms.

Operational risk is another significant challenge. This includes risks related to trade execution, order submission, and trade settlement processes. Errors in order placement, trade confirmations, or trade reconciliation can lead to financial losses or compliance issues. Traders must have effective risk management protocols, stringent controls, and thorough monitoring mechanisms to minimize operational risks.

Limited market liquidity presents challenges for algorithmic trading. In certain market conditions, the availability of buyers and sellers may be restricted, leading to difficulties in executing trades at desired prices or volumes. Traders need to assess liquidity risk and consider strategies that account for potential liquidity constraints, especially when dealing with illiquid markets or during periods of heightened market volatility.

Another challenge is the risk of over-optimization or curve fitting. Algorithms may be overly parameterized or specifically tailored to historical data, which can result in poor performance in real-world trading scenarios. Over-optimization can lead to strategies that are not robust and are unable to adapt to evolving market conditions. It is crucial to strike a balance between optimization and robustness to avoid the risk of overfitting the algorithm to past data.

Regulatory and compliance risks are also important considerations in algorithmic trading. Traders must adhere to applicable regulations governing algorithmic trading practices, including risk management requirements, reporting obligations, and market abuse regulations. Non-compliance with regulations can result in legal consequences, financial penalties, or reputational damage. It is necessary to stay informed about regulatory developments and ensure that algorithms and trading activities comply with the relevant rules and guidelines.

In summary, algorithmic trading is not without its risks and challenges. Traders must be aware of the potential pitfalls, including technical failures, market risk, data quality, operational risk, limited liquidity, over-optimization, and regulatory compliance. By understanding and actively managing these risks, traders can navigate the challenges and increase the odds of success in algorithmic trading.

Guidelines for Successful Algorithmic Trading

Algorithmic trading can be a powerful tool for traders to capitalize on market opportunities and generate profits. However, success in algorithmic trading requires careful planning, diligent execution, and continuous adaptation. In this section, we will discuss key guidelines that can contribute to successful algorithmic trading.

1. Define Clear and Measurable Goals: Clearly define your trading goals and objectives before developing an algorithmic trading strategy. Determine what you aim to achieve in terms of profitability, risk tolerance, and investment horizon. Having well-defined goals provides a foundation for building a successful trading strategy.

2. Invest in Comprehensive Research and Analysis: Thoroughly research and analyze different markets, asset classes, and trading strategies to identify opportunities that align with your goals. Conduct historical analysis, statistical modeling, and backtesting to evaluate potential strategies and their performance under various market conditions.

3. Develop a Robust and Customized Trading Strategy: Build a well-defined and customized trading strategy that aligns with your goals, risk appetite, and trading style. Tailor the strategy to specific market conditions and adapt it as market dynamics change. Consider incorporating risk management techniques and diversification to mitigate potential losses.

4. Implement a Solid Risk Management Framework: Establish strict risk management protocols and adhere to them consistently. Determine risk tolerance levels, set appropriate stop-loss orders, and calculate position sizes based on your risk appetite and account equity. Effective risk management is essential for long-term success.

5. Continuously Monitor and Evaluate Performance: Regularly monitor and assess the performance of your algorithmic trading strategy. Analyze key performance metrics, such as profitability, risk-adjusted returns, and drawdowns. Use the insights gained from monitoring to make informed adjustments and optimize the strategy’s performance.

6. Adapt and Refine Strategy as Market Conditions Change: Stay vigilant and adapt your strategy as market conditions evolve. Periodically reassess the strategy’s effectiveness, analyze changing trends, and consider modifying parameters or incorporating new techniques. Remaining flexible allows you to capitalize on emerging opportunities and minimize risks.

7. Stay Informed and Engage in Continuous Learning: Stay updated on market news, economic events, and technological advancements affecting algorithmic trading. Engage in continuous learning through books, seminars, online courses, and interactions with industry professionals. Enhancing your knowledge and skills will help refine your trading strategies and keep you at the forefront of the field.

8. Maintain Discipline and Emotional Control: Emotions can often hinder sound decision-making. Maintain discipline and stick to your trading strategy, avoiding impulsive reactions to short-term market fluctuations. Emotional control prevents irrational behavior that can lead to poor trading outcomes.

9. Regularly Review and Document Trading Activities: Keep detailed records of your trading activities, including executed trades, adjustments made to the strategy, and lessons learned. Regularly review performance reports and analyze trading patterns to identify strengths, weaknesses, and areas for improvement. Documentation helps refine your strategy and assists in compliance with regulatory requirements.

10. Seek Professional Advice and Collaboration: Consider seeking professional guidance or collaborating with experienced traders or consulting firms specializing in algorithmic trading. Their expertise can provide valuable insights, guide strategy development, and assist in navigating complex market dynamics.

In summary, successful algorithmic trading requires strategic planning, diligent research, robust risk management, continuous monitoring and adaptation, continuous learning, emotional control, discipline, documentation, and seeking professional advice. By adhering to these guidelines, traders can increase the likelihood of achieving success in algorithmic trading.