Introduction

Welcome to the fascinating world of blockchain technology! In today’s digital landscape, blockchain has emerged as a revolutionary concept that is transforming various industries, including finance, supply chain management, healthcare, and more. But what exactly is blockchain? How does it work? And what are its key features and benefits?

Simply put, blockchain is a decentralized and immutable digital ledger that records transactions across multiple computers or nodes. Unlike traditional centralized systems, blockchain operates on a distributed network, where each participant has a copy of the entire ledger. This transparency and consensus-based approach ensure that all transactions are verified and recorded securely.

At its core, blockchain relies on cryptographic hash functions that generate unique identifiers for each block of data added to the chain. These blocks are linked in a sequential order, forming a chronological record of transactions. Once a block is added to the chain, it is virtually impossible to alter or delete the data stored within it, ensuring the integrity and transparency of the system.

Now that we have a basic understanding of what blockchain is, let’s dive deeper into how it works. Each transaction on the blockchain is bundled into a block and verified by network participants, known as miners. These miners utilize computational power to solve complex mathematical puzzles, ultimately validating the authenticity of the transaction.

Once a consensus is reached among the miners, the block is added to the blockchain, and the transaction becomes a permanent part of the ledger. This decentralized consensus mechanism eliminates the need for intermediaries, such as banks or government entities, ensuring faster and cost-effective transactions without compromising security.

Blockchain technology boasts several key features that set it apart from traditional centralized systems. Firstly, it offers transparency and immutability, as all participants have access to the complete history of transactions. Any changes or tampering attempts can be easily identified and rejected by the network.

Furthermore, blockchain is known for its enhanced security. With its decentralized structure and cryptographic algorithms, it is extremely difficult for hackers to manipulate or gain unauthorized access to the data stored on the blockchain. This makes it a trusted platform for holding sensitive and valuable information.

In upcoming sections, we will explore the vast benefits of blockchain technology, including increased efficiency, reduced costs, improved trust and accountability, and more. Additionally, we’ll delve into specific use cases across various industries, as well as the limitations and challenges that blockchain faces.

Definition of Blockchain

Blockchain is a distributed ledger technology that enables the secure and transparent storage and management of digital transactions. It is a decentralized and immutable database that records and verifies transactions across multiple computers or nodes.

At its core, blockchain consists of blocks of data that are linked together in a chronological order, forming a chain. Each block contains a unique identifier, called a cryptographic hash, which ensures the integrity and security of the data stored within it. Once a block is added to the chain, it becomes virtually impossible to alter or delete the data, providing a high level of transparency and accountability.

One of the defining characteristics of blockchain is its decentralized nature. Unlike traditional centralized systems, where a central authority or intermediary controls and verifies transactions, blockchain operates on a network of computers or nodes. Each participant in the network has a copy of the entire blockchain, ensuring that no single entity has control over the data.

The decentralized nature of blockchain also enables a consensus mechanism, where network participants agree on the validity of transactions. This consensus is achieved through a process called mining, where participants use computational power to solve complex mathematical puzzles. Once a consensus is reached, the transactions are added to a new block and appended to the existing blockchain.

Blockchain technology provides numerous benefits, including increased security, transparency, and efficiency. By eliminating the need for intermediaries and central authorities, blockchain reduces the risks of fraud, manipulation, and censorship. The transparency of the blockchain allows for verifiable and auditable transactions, enhancing trust and minimizing disputes.

Moreover, blockchain has the potential to revolutionize various industries by streamlining processes, reducing costs, and creating new business models. Its applications extend beyond financial transactions, with use cases in supply chain management, healthcare, voting systems, intellectual property rights, and more.

Overall, blockchain represents a fundamental shift in how transactions and information are managed in the digital age. With its decentralized and transparent nature, it has the potential to transform industries and create a more secure and efficient world.

How Does Blockchain Work?

Blockchain technology operates on a decentralized network and follows a specific set of rules to ensure the secure and transparent management of transactions. Understanding how blockchain works requires delving into its key components and processes.

The first crucial element of blockchain is the network of computers or nodes. These nodes work together as a distributed network, each maintaining a copy of the entire blockchain. They actively participate in the validation and verification of transactions.

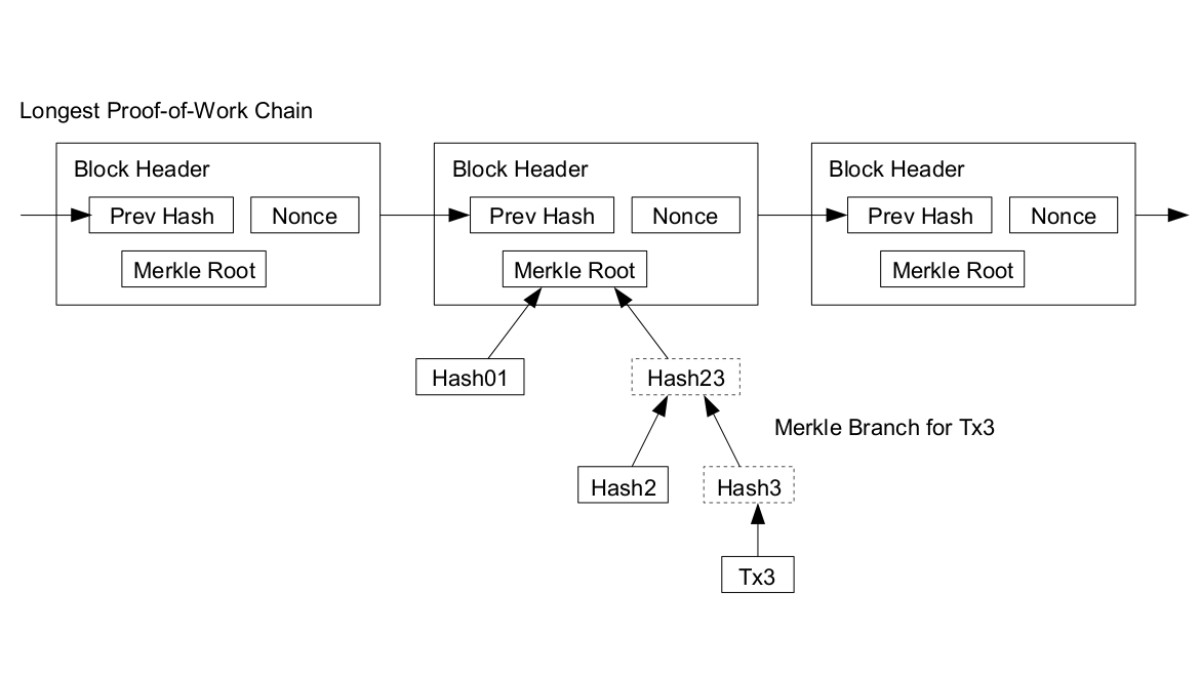

When a transaction is initiated, it is bundled with other transactions into a block. This block contains a unique identifier or hash that represents the data within it. The hash is generated using cryptographic algorithms, making it virtually impossible to manipulate or alter the data stored within the block.

Now comes the consensus mechanism, which plays a vital role in ensuring the integrity of the blockchain. Miners, who are participants in the network, compete to solve complex mathematical puzzles related to the block. This process is known as mining.

Miners utilize computational power to continuously hash different combinations until they find a solution that satisfies the network’s predetermined criteria. The first miner to solve the puzzle broadcasts the solution to the network, allowing other participants to verify and validate it.

Once a consensus is reached, the verified block is added to the existing chain, forming a permanent and unchangeable record of transactions. Each block contains a reference or hash of the previous block, creating a linked chain of blocks.

The decentralized nature of blockchain ensures that all nodes in the network have a complete copy of the blockchain. This distribution and redundancy reduce the risks of data loss or tampering. Any attempt to modify past blocks would require a tremendous amount of computational power, making the blockchain highly secure.

Furthermore, blockchain adheres to the principle of immutability. Once a block is added to the chain, it cannot be deleted or altered. This provides a transparent and auditable transaction history, which brings an unprecedented level of trust and accountability to various industries.

In summary, blockchain technology works by leveraging a decentralized network of computers or nodes to validate and verify transactions. Through consensus mechanisms and cryptographic algorithms, it ensures the integrity and immutability of the data stored within blocks. This transparent and secure approach has the potential to revolutionize industries and reshape the way we conduct transactions in the digital age.

Key Features of Blockchain

Blockchain technology encompasses several key features that differentiate it from traditional centralized systems. These features contribute to the transparency, security, and efficiency that blockchain offers. Let’s delve into the key features of blockchain:

Decentralization: Blockchain operates on a decentralized network of computers or nodes. This means that no single entity or central authority has control over the entire blockchain. The data is distributed across multiple nodes, ensuring that no single point of failure exists. Decentralization eliminates the need for intermediaries and provides increased security and transparency.

Immutability: Once data is recorded on the blockchain, it cannot be changed or tampered with. Each block in the blockchain contains a unique cryptographic hash, which represents the data stored within it. Any modification to the data would result in a change of the hash, making it instantly detectable. Immutability ensures the integrity and authenticity of the recorded transactions.

Transparency: Blockchain provides transparency by giving all participants access to the complete transaction history. Every transaction recorded on the blockchain is visible to all nodes in the network. With transparent transactions, there is a higher level of trust and accountability, reducing the risk of fraud and manipulation.

Security: Blockchain employs cryptographic algorithms to ensure the security of the data stored within the blockchain. Each block is linked to the previous block through a hash, forming an encrypted chain. The use of encryption provides protection against unauthorized access and ensures the privacy of sensitive information.

Consensus Mechanism: Blockchain relies on a consensus mechanism to validate and verify transactions. In most blockchain networks, this is achieved through mining, where participants compete to solve complex mathematical puzzles. The first participant to solve the puzzle broadcasts the solution, which is then verified by other nodes in the network. Consensus mechanisms ensure that only valid transactions are added to the blockchain.

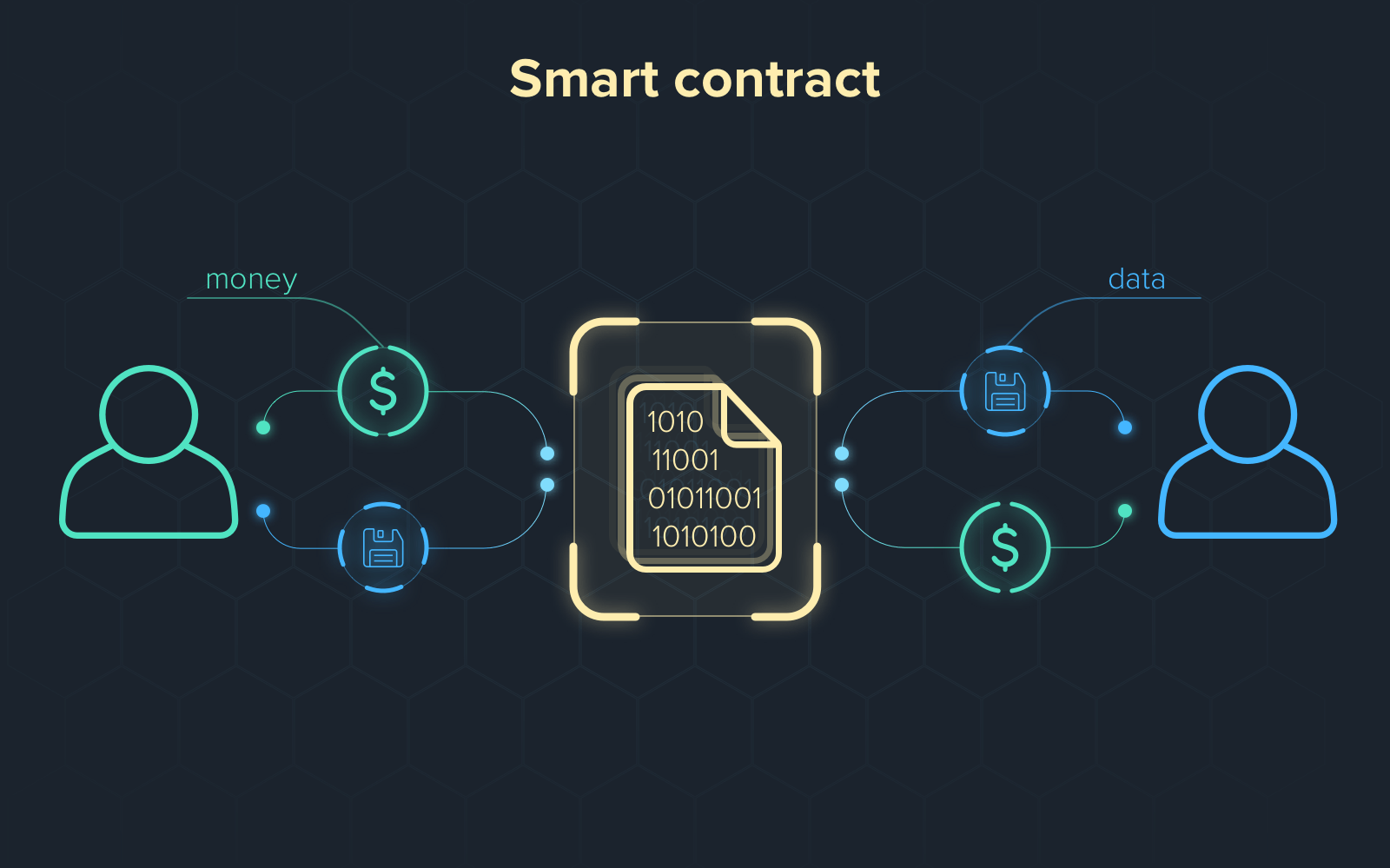

Smart Contracts: Smart contracts are self-executing contracts with predefined rules written into code. They are stored and executed on the blockchain, ensuring transparent and automated transactions. Smart contracts eliminate the need for intermediaries and facilitate direct peer-to-peer interactions, streamlining processes and reducing costs.

Interoperability: Blockchain technology has the potential to enable interoperability between different systems and platforms. Through standardization and protocols, blockchain networks can communicate and exchange information seamlessly, creating a unified and interconnected ecosystem.

These key features of blockchain contribute to its widespread adoption across various industries. From finance to supply chain management, healthcare to voting systems, blockchain offers a secure and transparent foundation for transforming traditional processes and creating innovative solutions.

Benefits of Blockchain Technology

Blockchain technology offers numerous benefits that have the potential to revolutionize various industries. Let’s explore the key advantages of using blockchain:

Enhanced Security: Blockchain employs advanced cryptographic algorithms to secure transactions and data. The decentralized nature of blockchain, coupled with its immutability, makes it highly resistant to tampering and fraud. By eliminating the need for intermediaries and central authorities, blockchain reduces the risks of data breaches and unauthorized access.

Transparency and Traceability: Blockchain provides a transparent and auditable transaction history. All participants in the network can view and verify transactions, ensuring accountability and reducing the chances of fraud or manipulation. This traceability is particularly valuable in industries such as supply chain management, where it enables greater visibility and ensures the authenticity and quality of products.

Improved Efficiency: By eliminating manual processes and intermediaries, blockchain streamlines transactions and reduces operational inefficiencies. For example, in financial services, blockchain can facilitate faster cross-border transactions, automated settlements, and real-time auditing. The use of smart contracts further enhances efficiency by automating contract execution and reducing paperwork.

Cost Savings: With blockchain, businesses can significantly reduce costs associated with intermediaries, paperwork, and manual processes. By removing the need for third-party verification, blockchain minimizes transaction fees and administrative expenses. Additionally, smart contracts enable automated and error-free transactions, leading to cost savings in contract enforcement and compliance.

Increased Trust and Accountability: Blockchain creates a high level of trust among participants due to its transparent and immutable nature. It eliminates the need to rely solely on trust in centralized authorities or intermediaries. Instead, trust is established through mathematical algorithms and consensus mechanisms. This increased trust and accountability can improve relationships, facilitate collaboration, and attract new business opportunities.

Data Integrity: The immutability and cryptographic security of blockchain ensure the integrity of data stored within the system. This feature is essential in industries that deal with sensitive information, such as healthcare and intellectual property. Blockchain can help prevent data breaches, unauthorized modifications, and intellectual property theft, providing a secure platform for storing and sharing valuable data.

Decentralization and Resilience: The decentralized nature of blockchain ensures that there is no single point of failure. The data is distributed across multiple nodes, making it resilient to attacks and system failures. If one node fails or becomes compromised, the rest of the network remains operational, ensuring the continuity of transactions and data availability.

Overall, blockchain technology offers a wide range of benefits, including enhanced security, transparency, efficiency, cost savings, trust, data integrity, and decentralization. These advantages have the potential to transform industries and drive innovation, creating a more secure, efficient, and interconnected world.

Blockchain Use Cases

Blockchain technology has the potential to disrupt and transform various industries by providing secure, transparent, and efficient solutions. Let’s explore some of the key use cases of blockchain:

Finance and Payments: Blockchain has gained significant traction in the finance industry. It can facilitate faster, more secure, and cheaper cross-border transactions by removing the need for intermediaries and traditional banking systems. Blockchain-based cryptocurrencies, such as Bitcoin and Ethereum, have also emerged as alternative forms of digital currency, providing individuals with more control over their finances.

Supply Chain Management: Blockchain offers transparency and traceability in supply chain management. By recording and verifying every transaction along the supply chain, blockchain ensures the authenticity and quality of products. It enables stakeholders to track and trace the movement of goods, from raw materials to the end consumer, thereby reducing the risk of counterfeiting, improving efficiency, and enhancing consumer trust.

Healthcare: Blockchain can streamline healthcare systems by securely storing and sharing patient records, medical histories, and other sensitive information. It ensures data privacy, prevents unauthorized access, and enables seamless sharing of information among healthcare providers. Blockchain can also facilitate the tracking and verification of pharmaceuticals, preventing counterfeit drugs from entering the supply chain.

Identity Management: Blockchain has the potential to revolutionize identity management by providing secure and decentralized solutions. Instead of relying on centralized databases vulnerable to data breaches, blockchain offers a tamper-proof and verifiable record of identities. This can eliminate the need for multiple documentation processes and allow individuals to have more control over their personal information.

Intellectual Property: Blockchain can transform the way intellectual property is managed and shared. By utilizing blockchain’s immutable and timestamping capabilities, artists, inventors, and creators can securely register and protect their intellectual property rights. This enhances transparency, reduces infringement disputes, and allows for fair compensation and royalties to be distributed automatically.

Voting Systems: Blockchain-based voting systems can enhance the security and integrity of elections. By recording votes on a tamper-proof and transparent blockchain, it becomes nearly impossible to manipulate or tamper with the results. This increases voter trust, reduces the risk of fraud, and ensures accurate and auditable election outcomes.

Real Estate: Blockchain can simplify and streamline real estate transactions, reducing the need for intermediaries and paperwork. It can enable secure and transparent property ownership transfers, track property histories, and facilitate faster and more efficient property transactions. This can potentially reduce costs, fraud, and disputes in the real estate industry.

These are just a few examples of how blockchain technology is being applied across various industries. The potential use cases for blockchain continue to expand as organizations explore its capabilities and leverage its benefits for secure, transparent, and efficient solutions.

Limitations and Challenges of Blockchain

While blockchain technology offers numerous advantages, it also faces certain limitations and challenges that need to be addressed for widespread adoption. Let’s explore some of the key limitations and challenges of blockchain:

Scalability: One of the major challenges of blockchain technology is scalability. As more transactions are added to the blockchain, the size of the blockchain grows, leading to increased storage and processing requirements. This can result in slower transaction speeds and higher costs. Scaling solutions, such as off-chain transactions and sharding, are being explored to address this challenge.

Energy Consumption: Blockchain mining, particularly in proof-of-work consensus mechanisms like Bitcoin, requires significant computational power and energy consumption. The energy consumption associated with blockchain mining has raised concerns about its environmental impact. Research and development of more energy-efficient consensus mechanisms, such as proof-of-stake, are underway to mitigate this challenge.

Regulatory and Legal Challenges: Blockchain operates across borders, leading to jurisdictional challenges and conflicts with existing regulations. The lack of clarity around legal frameworks and regulations for blockchain technology poses a challenge for its implementation in various industries. Developing regulatory guidelines and fostering collaboration between regulators and blockchain stakeholders is essential to overcome these challenges.

Privacy Concerns: While blockchain offers transparency, privacy concerns arise when dealing with sensitive and personal data. Public blockchains, by design, make all transactions transparent and visible to every participant in the network. Implementing privacy-enhancing technologies, such as zero-knowledge proofs or private blockchains, can help address these concerns.

Interoperability: Blockchain networks often operate in silos, making it challenging for different networks to communicate and share information seamlessly. Achieving interoperability between different blockchain platforms is crucial to unlock the full potential of blockchain technology. Initiatives, such as cross-chain protocols and standards, are being developed to address this challenge.

Economics and Incentives: Designing economic incentives that align the interests of participants within blockchain networks can be complex. In some cases, incentive structures may not align with long-term sustainability or decentralized decision-making. Developing robust token economics and incentive mechanisms is critical to ensure the stability and longevity of blockchain networks.

Education and Adoption: Blockchain technology is still relatively new and unfamiliar to many individuals and organizations. Widespread education and awareness are necessary for broader adoption. This includes educating stakeholders about the benefits, use cases, and potential risks associated with blockchain, as well as providing user-friendly tools and interfaces that facilitate ease of use.

Legacy Systems Integration: Integrating blockchain technology with existing legacy systems can be challenging. Many organizations face hurdles in migrating from centralized systems to decentralized blockchain networks. Addressing these challenges involves developing tools and protocols that enable seamless integration and interoperability between legacy systems and blockchain technology.

Despite these limitations and challenges, advancements are being made to overcome these barriers and maximize the potential of blockchain technology. Through continued research, collaboration, and innovation, blockchain can evolve to become a robust and scalable solution for various industries.

Conclusion

Blockchain technology has emerged as a groundbreaking innovation that has the potential to transform various industries. Its decentralized and transparent nature offers enhanced security, efficiency, and trust in digital transactions. By eliminating the need for intermediaries and central authorities, blockchain provides a secure and efficient platform for recording, verifying, and managing transactions.

Throughout this article, we have explored the definition and workings of blockchain, discussed its key features and benefits, and examined its use cases across different sectors. From finance and supply chain management to healthcare and voting systems, blockchain offers solutions that can streamline processes, reduce costs, and enhance trust and accountability.

However, it is important to acknowledge the limitations and challenges that blockchain faces. Scalability, energy consumption, regulatory frameworks, privacy concerns, interoperability, and integration with legacy systems are among the hurdles that need to be overcome for wider adoption of blockchain technology.

Nonetheless, the potential of blockchain technology cannot be underestimated. With ongoing research, development, and collaboration, these challenges can be addressed to unlock the full potential of blockchain. Continued education, awareness, and user-friendly interfaces will also play a crucial role in driving adoption and democratizing the benefits of blockchain technology.

Ultimately, blockchain has the capacity to redefine how transactions and information are managed in a secure, transparent, and decentralized manner. As industries increasingly recognize the value of blockchain, we can expect to witness further advancements, innovations, and real-world implementations.

In the coming years, we can anticipate blockchain revolutionizing various sectors, facilitating seamless peer-to-peer interactions, enhancing data security and privacy, and fostering trust and transparency. The journey towards a blockchain-enabled future is just beginning, and the possibilities are immense.