Introduction

Welcome to the world of blockchain smart contracts! In this digital era, where technology is advancing at an unprecedented pace, smart contracts have emerged as a game-changing innovation. They have the potential to revolutionize the way agreements are made and executed in various industries.

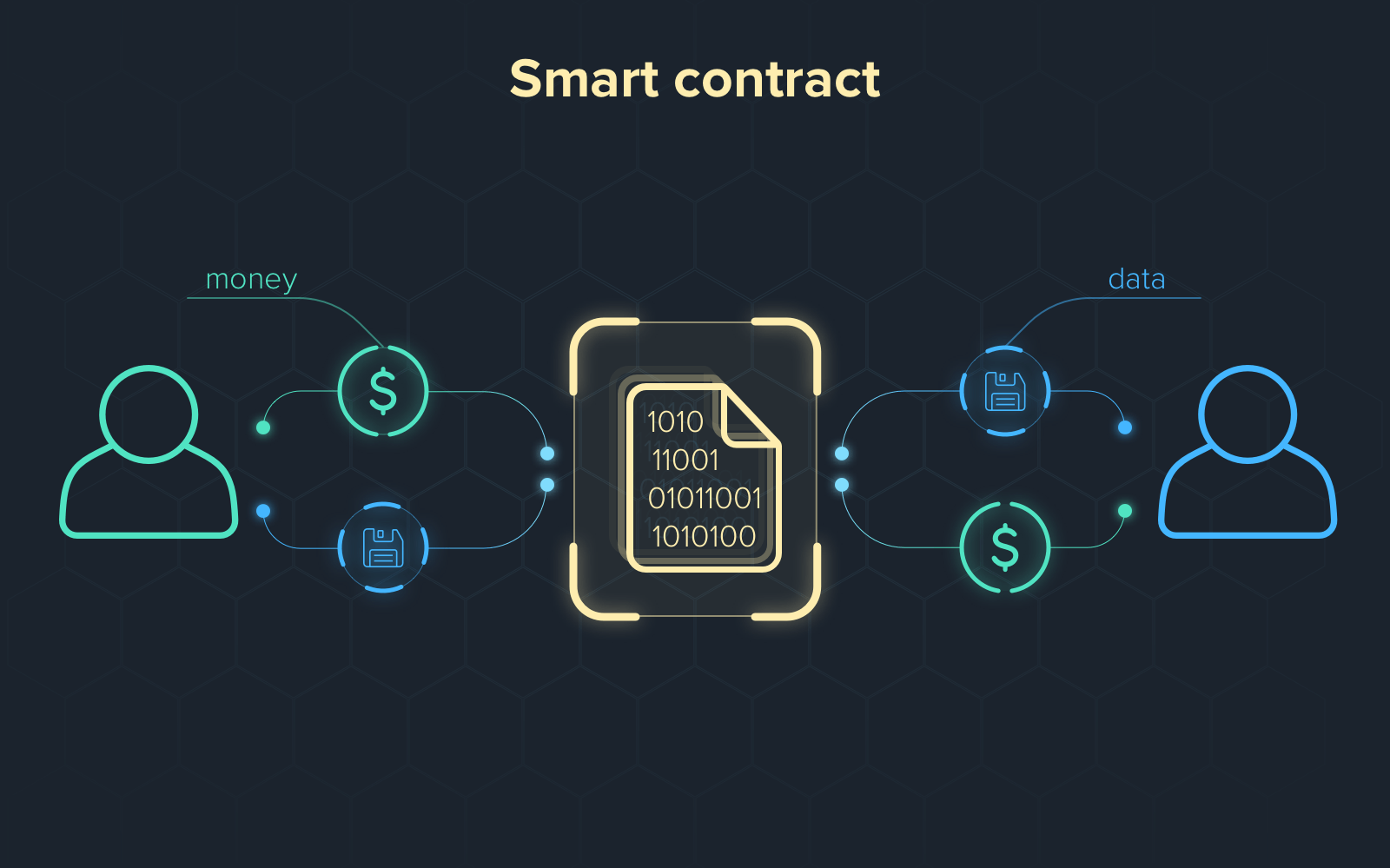

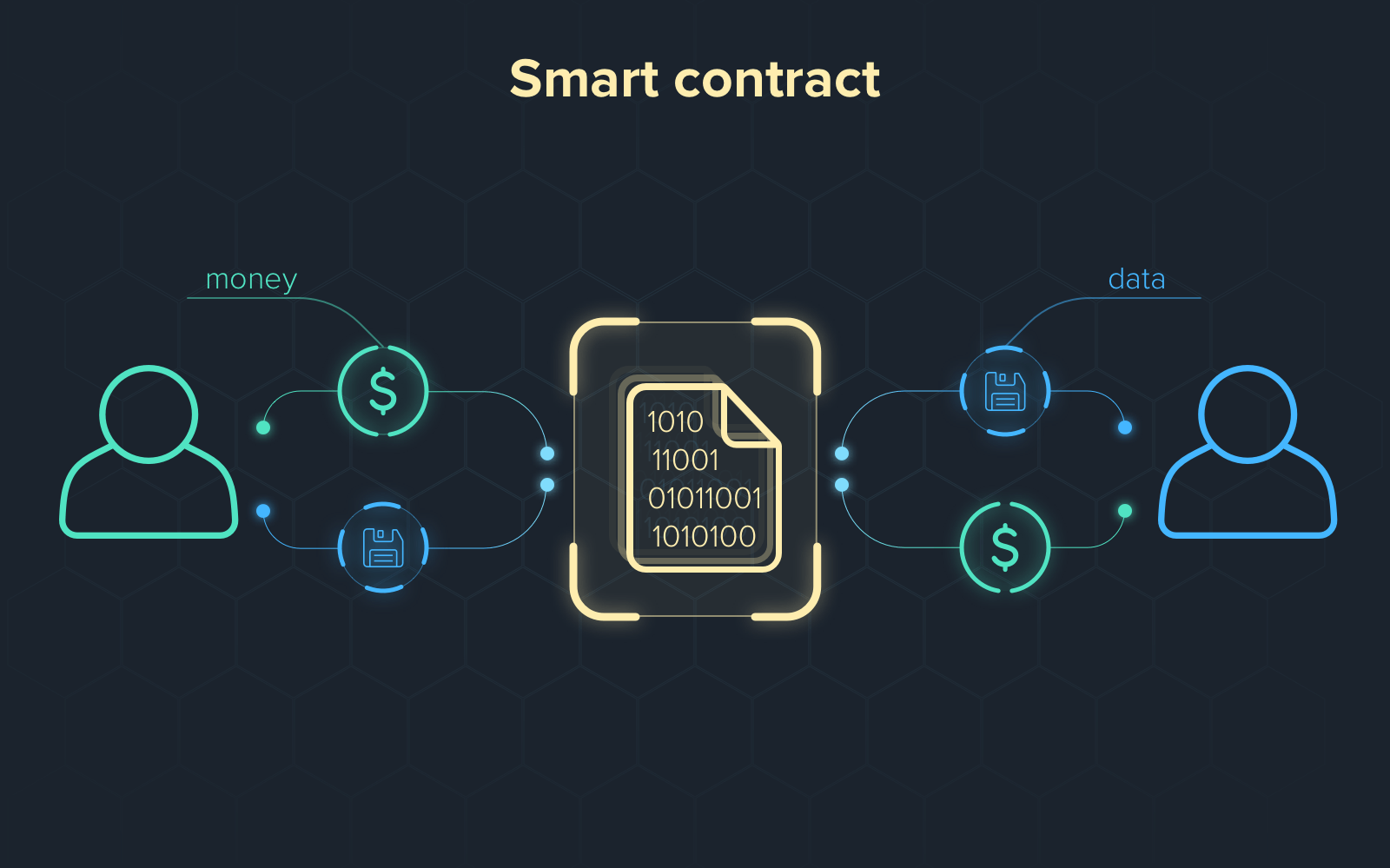

A blockchain smart contract is a self-executing contract with the terms of the agreement directly written into code. It runs on a blockchain network, ensuring transparency and immutability of the contract. Once the conditions specified in the contract are met, the contract is automatically executed without the need for intermediaries.

The benefits of using smart contracts are numerous. They eliminate the need for intermediaries, reduce the chances of fraud, ensure faster and more efficient transactions, and increase security and trust. Smart contracts have applications in a wide range of industries, including finance, supply chain management, healthcare, real estate, and more.

To understand blockchain smart contracts, it is essential to grasp the fundamentals of blockchain technology. Blockchain is a decentralized and distributed ledger technology that records transactions across multiple computers. It provides transparency, security, and immutability, making it an ideal platform for executing smart contracts.

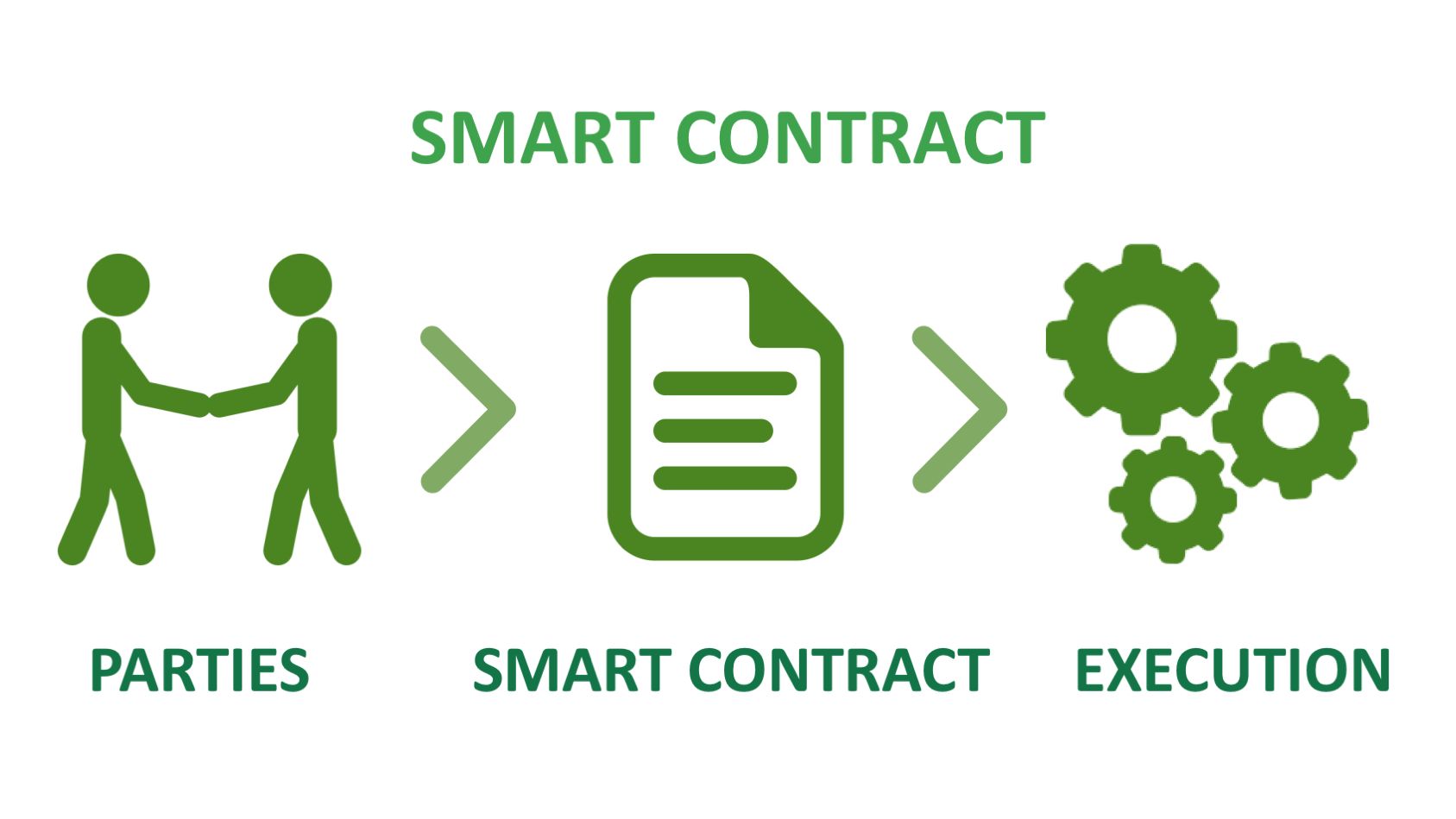

A smart contract typically consists of three main parts: the agreement, the conditions, and the actions. The agreement outlines the terms and conditions of the contract, while the conditions define the trigger events that need to occur for the contract to be executed. The actions specify the tasks to be performed once the conditions are met.

If you are interested in creating your own blockchain smart contract, you’ve come to the right place. In this article, we will guide you through the steps involved in creating a blockchain smart contract, from defining the contract logic to deploying and interacting with the contract.

Are you ready to dive into the fascinating world of blockchain smart contracts? Let’s get started!

What is a Blockchain Smart Contract?

A blockchain smart contract is a self-executing digital contract that is stored on a blockchain network. It is an agreement between two or more parties that is written in code and automatically executes itself when the predefined conditions are met. Unlike traditional contracts that require intermediaries, such as lawyers or banks, to ensure trust and enforceability, smart contracts use the decentralized nature of blockchain technology to achieve these goals.

Smart contracts are built using programming languages specifically designed for the blockchain, such as Solidity for Ethereum. These programming languages allow developers to define the logic and rules of the contract in a machine-readable format. The code is then deployed onto a blockchain network, where it runs and executes automatically without the need for human intervention.

The key concept behind smart contracts is the idea of “if-then” statements. The contract contains a set of conditions that specify what needs to happen for the contract to be executed. For example, in a real estate smart contract, the conditions could be the successful transfer of funds and the verification of property ownership. Once these conditions are met, the contract is executed, and the ownership of the property is transferred to the buyer.

One of the unique features of smart contracts is their transparency. Since they run on a blockchain network, all transactions and changes to the contract are recorded and visible to all participants. This transparency ensures accountability and prevents any party from tampering with the contract or denying its existence.

Another significant advantage of smart contracts is their ability to automate complex processes and eliminate the need for intermediaries. In traditional contracts, intermediaries play a crucial role in verifying the terms of the contract and enforcing compliance. With smart contracts, all these tasks are automated, reducing costs, improving efficiency, and minimizing the chances of human error or fraud.

The applications of smart contracts are vast and extend beyond just financial transactions. They can be used in supply chain management to track the movement of goods, in healthcare to ensure the privacy and security of patient data, and in the legal industry to streamline processes and reduce paperwork. The versatility of smart contracts makes them a powerful tool for transforming various industries and business processes.

In the next sections, we will take a closer look at the technical aspects of smart contracts and guide you through the process of creating your own blockchain smart contract.

Benefits of Using Smart Contracts

Smart contracts offer a wide range of benefits that make them an attractive solution for businesses and individuals. Let’s explore some of the key advantages of using smart contracts:

1. Increased Efficiency: Smart contracts automate manual processes, reducing the need for intermediaries and paperwork. This streamlined approach results in faster execution of agreements, saving time and resources for all parties involved.

2. Cost Savings: By eliminating intermediaries and reducing the administrative overhead associated with traditional contracts, smart contracts help businesses cut costs. Smart contracts also remove the need for expensive dispute resolution mechanisms, as they are self-executing and enforceable.

3. Enhanced Security: Blockchain technology provides a high level of security and immutability. Smart contracts leverage these features, offering robust protection against fraud, tampering, and unauthorized access to the contract’s contents.

4. Trust and Transparency: Smart contracts run on distributed blockchain networks, where every transaction and change is recorded and visible to all participants. This transparency builds trust among parties, as it ensures that no one can alter the terms of the contract without the knowledge of others.

5. Accuracy and Elimination of Errors: Smart contracts are executed according to predefined code, eliminating the possibility of human error in interpreting or executing the contract terms. This accuracy reduces the risk of mistakes and discrepancies that may occur in traditional contracts.

6. Immutable Record Keeping: Every action and transaction related to a smart contract is permanently recorded on the blockchain. This immutable record provides an auditable trail that can be used for compliance and record-keeping purposes.

7. Global Accessibility: Smart contracts can be accessed and executed by anyone with an internet connection, regardless of geographical location or time zone. This global accessibility opens up new opportunities for businesses to collaborate and transact with partners all over the world.

8. Improved Efficiency in Complex Processes: Smart contracts can automate complex processes that involve multiple parties and conditional actions. This automation reduces the need for manual coordination and significantly improves the efficiency of such processes.

9. Environmental Impact: By digitizing contracts and reducing paperwork, smart contracts contribute to a more sustainable and environmentally friendly way of doing business. This reduction in paper usage helps conserve natural resources and reduce carbon emissions.

In summary, smart contracts bring numerous benefits to various industries, including increased efficiency, cost savings, enhanced security, trust and transparency, accuracy, immutable record-keeping, global accessibility, improved efficiency in complex processes, and a positive environmental impact. By leveraging the power of blockchain technology, smart contracts have the potential to transform the way agreements are made and executed, revolutionizing business processes and fostering innovation.

Understanding Blockchain Technology

Before diving deeper into smart contracts, it’s crucial to understand the underlying technology that powers them: blockchain. Blockchain is a decentralized and distributed ledger technology that ensures the transparency, security, and immutability of data.

At its core, a blockchain is a digital ledger that records transactions or any form of data across multiple computers or nodes in a network. These computers work collaboratively to verify and validate each transaction, ensuring that all copies of the ledger are identical.

The blockchain network consists of blocks, where each block contains a list of transactions. Once a block is completed and added to the blockchain, it is cryptographically linked to the previous block, forming a chain of blocks – hence the name, blockchain.

One of the key features of blockchain technology is its decentralized nature. Rather than relying on a single centralized authority, such as a bank or government, blockchain is maintained by a network of participants who collectively validate and verify transactions. This decentralization ensures that no single entity has complete control over the network, enhancing security and trust.

Another notable characteristic of blockchain is its transparency. The data recorded on the blockchain is visible to all participants, creating a transparent ecosystem where everyone has access to the same information. This transparency helps prevent fraud and manipulation, as any tampering with the data would be immediately noticeable to the network.

Security is a paramount aspect of blockchain technology. The structure of the blockchain, combined with advanced cryptographic algorithms, makes it extremely difficult for hackers to manipulate or forge transactions. Each transaction recorded on the blockchain is encrypted and linked to the previous transactions, creating a secure and tamper-proof environment.

Immutability is another significant feature of blockchain. Once a transaction is added to the blockchain, it cannot be altered or deleted. This immutability ensures the integrity of the data and provides an auditable and verifiable trail of all transactions that have ever taken place.

Blockchain technology has gained significant attention and adoption across various industries beyond cryptocurrencies. It has applications in supply chain management, healthcare, finance, voting systems, and more. This disruptive technology has the potential to revolutionize traditional processes by increasing efficiency, enhancing security, and reducing costs.

Now that we have a basic understanding of blockchain technology, let’s explore how this technology intersects with smart contracts and how they work together to create a powerful and innovative solution.

Parts of a Smart Contract

A smart contract consists of several components that work together to define the terms, conditions, and actions of the contract. Understanding these components is essential for creating and interacting with smart contracts effectively.

1. Agreement: The agreement is the first part of a smart contract and defines the terms and conditions that the participants agree upon. It typically includes details such as the parties involved, the assets involved, and the desired outcome.

2. Conditions: The conditions part of a smart contract specifies the trigger events that need to occur for the contract to be executed. These conditions can be time-based, event-based, or dependent on specific data inputs. For example, a condition in a supply chain smart contract could be the successful delivery of goods.

3. Actions: The actions part of a smart contract outlines the tasks that will be performed once the conditions are met. These actions are usually automated and do not require human intervention. Examples of actions could include transferring ownership of an asset, releasing funds, or updating a database.

4. Variables: Variables are used to store and manipulate data within a smart contract. They can hold information such as addresses, values, timestamps, and more. Variables play a crucial role in executing the conditions and actions specified in the contract.

5. Functions: Functions are blocks of code that perform specific tasks within a smart contract. They can be called by the contract itself or by external entities interacting with the contract. Functions are used to define the logic and behavior of the contract, allowing it to respond to various events and external requests.

6. Events: Events are notifications that are emitted by a smart contract to indicate a specific occurrence or state change. They can be subscribed to by external applications or user interfaces, allowing them to react and display relevant information to users. Events help in providing real-time updates and transparency to contract participants.

7. Wallets and Signatures: Wallets and signatures play a vital role in ensuring the authenticity and security of smart contracts. Each participant in a contract needs a digital wallet, which contains a unique cryptographic key pair. When a participant wants to interact with the contract, they sign their transactions using their private key, providing proof of their identity and giving consent for the transaction to be executed.

By understanding these components, you can effectively analyze, create, and interact with smart contracts. Each part plays a critical role in shaping the behavior and execution of the contract, allowing for transparent, automated, and secure agreements.

How to Create a Blockchain Smart Contract

Creating a blockchain smart contract involves several steps, from defining the contract logic to deploying and interacting with the contract. Here is a step-by-step guide on how to create a blockchain smart contract:

Step 1: Define the Contract Logic: Start by clearly defining the purpose and requirements of your smart contract. Identify the agreement, conditions, and actions that need to be coded into the contract.

Step 2: Choose a Blockchain Platform: Select a suitable blockchain platform that supports smart contract development. Ethereum is currently the most popular platform for creating smart contracts, but other options such as Hyperledger Fabric, EOS, and Tron also offer smart contract capabilities.

Step 3: Install and Set Up the Required Tools: Install the necessary tools and software development kits (SDKs) for your chosen blockchain platform. This may include a smart contract development framework, a code editor, and a blockchain client.

Step 4: Write the Smart Contract Code: Use a programming language supported by the blockchain platform, such as Solidity for Ethereum, to write the code for your smart contract. Define the functions, variables, and events according to the logic and requirements you defined in Step 1.

Step 5: Compile and Deploy the Contract: Compile your smart contract code into bytecode and deploy it onto the blockchain network. This step requires interacting with the blockchain client or using development tools provided by the chosen platform.

Step 6: Interact with the Smart Contract: Once the smart contract is deployed, you can interact with it by sending transactions to it. This can be done using a web-based user interface, a command-line interface, or by interacting with the contract programmatically.

Keep in mind that creating a blockchain smart contract requires a solid understanding of programming, blockchain technology, and the specific development tools and platforms you are using. It is recommended to experiment with sample contracts, seek guidance from developer communities, and conduct thorough testing before deploying your contract for real-world use.

Always consider security best practices and perform code audits to ensure that your smart contract is secure from vulnerabilities and exploits.

By following these steps and continuously improving your skills and understanding of smart contract development, you can create robust and reliable blockchain smart contracts that bring trust, automation, and efficiency to your agreements and transactions.

Step 1: Define the Contract Logic

When creating a blockchain smart contract, it is crucial to begin by clearly defining the contract logic. This step involves understanding the purpose of the contract and identifying the agreement, conditions, and actions that need to be coded into the contract.

The first aspect to consider is the agreement itself. Determine what the contract aims to achieve, the parties involved, and the assets or services being exchanged. Creating a well-defined agreement ensures that all parties have a clear understanding of their roles and responsibilities.

Next, define the conditions that need to be met for the contract to execute. These conditions can be time-based, event-based, or data-dependent. For instance, in a crowdfunding smart contract, the condition for executing the contract could be reaching a specified funding goal within a defined timeframe.

It is important to consider different scenarios and account for potential exceptions or variations in the contract logic. Anticipate possible edge cases and define how the contract will handle them. By thoroughly defining the conditions, you can ensure that the contract behaves as intended in various scenarios.

The actions that need to be performed when the conditions are met should also be clearly defined. These actions can include transferring ownership, releasing funds, updating a database, or triggering other processes within the contract or external systems. Specify the desired outcomes and the steps required to achieve them.

During this step, it is crucial to accurately define the inputs, outputs, and expected behavior of the contract. Consider the potential risks and include appropriate safeguards to handle potential errors or disputes. Strive for simplicity and clarity in the contract logic to minimize ambiguity and misunderstandings.

Additionally, documentation plays a vital role in this step. Document the contract logic, including the agreement, conditions, and actions, in a clear and comprehensible manner. This documentation acts as a reference for developers, auditors, and participants, ensuring a common understanding of the contract’s purpose and functionality.

Remember that defining the contract logic lays the foundation for the successful creation and implementation of a blockchain smart contract. Taking the time to thoroughly analyze and define the logic upfront will save effort and time in the later stages of development.

Stay tuned for the next steps, where we will explore how to choose a blockchain platform and the necessary tools for creating smart contracts.

Step 2: Choose a Blockchain Platform

Choosing the right blockchain platform is a crucial step when creating a blockchain smart contract. The platform you select will determine the development tools, programming languages, and ecosystem available for building and deploying your smart contract. Here are some factors to consider when choosing a blockchain platform:

1. Suitability for your Use Case: Evaluate which blockchain platform aligns best with your specific use case. Consider factors such as scalability, network consensus mechanism, privacy features, and the ability to handle smart contracts.

2. Programming Language Support: Different blockchain platforms support different programming languages for smart contract development. For example, Ethereum primarily uses Solidity, while Hyperledger Fabric supports popular languages like JavaScript and Go. Choose a platform that supports a programming language you are comfortable with or are willing to learn.

3. Community Support and Developer Resources: Consider the size and activity of the community surrounding the platform. A vibrant community provides access to resources, tutorials, forums, and developer support, making it easier to learn and troubleshoot during the development process.

4. Interoperability and Integration: Determine whether the platform can seamlessly integrate with existing systems or other blockchain networks if required. Interoperability can be essential when you intend to connect your smart contract with external data sources or other blockchains.

5. Consensus Mechanism: Understand the consensus mechanism used by the platform. Different consensus algorithms have different attributes such as scalability, energy efficiency, and decentralization. Select a platform with a consensus mechanism suitable for your project’s requirements.

6. Security Considerations: Take into account the security features and protocols provided by the platform. Look for platforms that emphasize security best practices, offer auditability, and have a track record of mitigating vulnerabilities and attacks.

7. Governance and Upgradability: Assess the governance structure and upgradability options of the platform. Consider whether it supports on-chain governance models or community-driven decision-making. Additionally, look for platforms that offer easy upgradability without compromising the security and integrity of the smart contract.

8. Network Scalability: Evaluate the scalability of the platform and its ability to handle the expected transaction volume of your smart contract. Consider whether the platform employs sharding, sidechains, or other means to enhance scalability and performance.

It is essential to thoroughly research and compare different blockchain platforms before making a decision. Consider consulting with experts or seeking advice from the platform’s community. Once you have selected a suitable platform, you can proceed to the next step of installing and setting up the necessary tools for smart contract development.

Stay tuned for the upcoming steps, where we will guide you through installing and setting up the required tools for creating your blockchain smart contract.

Step 3: Install and Set Up the Required Tools

After choosing a suitable blockchain platform, the next step in creating a blockchain smart contract is to install and set up the necessary tools for development. These tools will enable you to write, compile, and deploy your smart contract code. Here are the key steps involved in this process:

1. Development Framework: Depending on the chosen blockchain platform, you may need to install a development framework specific to that platform. For example, if you are using Ethereum, you can install the Truffle or Hardhat framework, which provide a set of tools, libraries, and functionalities for smart contract development.

2. Code Editor: Choose a code editor or an integrated development environment (IDE) that suits your preferences. Popular options include Visual Studio Code, Atom, or Remix IDE (for web-based development on Ethereum). These editors provide syntax highlighting, code completion, and other helpful features for smart contract development.

3. Blockchain Client: Set up a blockchain client to interact with the chosen blockchain platform. This client allows you to connect to the blockchain network, deploy your smart contract, and interact with other contracts and services. Ethereum, for example, has clients like Geth or Ganache that you can install and configure.

4. Smart Contract Development Tools and Libraries: Install any additional tools or libraries required for smart contract development. For instance, Ethereum provides tools like Solc (Solidity Compiler) for compiling Solidity code, Web3.js or Ethers.js for interacting with the Ethereum network, and Ganache CLI or Truffle Develop for local testing and development.

5. Testing Framework: Consider setting up a testing framework for your smart contract. This helps you write automated tests to ensure the functionality and correctness of your contract. Tools like Mocha and Chai are commonly used for testing smart contracts on various blockchain platforms.

6. Documentation and Resources: Take advantage of the documentation and resources provided by the blockchain platform and the development tools you are using. These resources include official documentation, tutorials, code samples, and community forums. Leveraging these resources can help accelerate your learning and problem-solving during the development process.

Ensure that you follow the installation instructions and follow best practices recommended by the platform and the development tools. Pay attention to version compatibility, security considerations, and any additional dependencies required by the tools.

Once you have successfully installed and set up the required tools, you are ready to move on to the next step: writing the code for your smart contract.

Stay tuned for the following sections, where we will guide you through writing the smart contract code, compiling and deploying the contract, and interacting with it.

Step 4: Write the Smart Contract Code

With the necessary tools and development environment set up, it’s time to start writing the code for your blockchain smart contract. This step involves defining the functions, variables, and events that make up the logic and behavior of your contract. Here’s a breakdown of the key elements involved:

1. Functions: Functions are the building blocks of a smart contract. They define the actions or tasks that the contract can perform. You will write functions to handle various operations, such as transferring assets, updating data, or executing specific actions based on predefined conditions.

2. Variables: Variables are used to store and manipulate data within the contract. They can hold values such as addresses, integers, strings, or arrays. Consider the data types that best suit your requirements and define variables accordingly. Variables are essential for maintaining the contract state and performing calculations or comparisons.

3. Events: Events enable your contract to communicate and notify external systems or user interfaces about specific occurrences. You can define events within your contract and emit them whenever certain conditions are met. Events can be subscribed to by external applications, allowing them to react and display relevant information to users in real-time.

4. Modifiers: Modifiers are used to change the behavior of functions within your contract. They allow you to enforce certain conditions or permissions before a function is executed. For example, you can define a modifier to restrict access to a function only to the contract owner or to check if a certain condition is met before proceeding with the function execution.

5. Inheritance: Inheritance enables you to reuse code and inherit properties and functions from other contracts. By employing inheritance, you can create modular and maintainable contract code. This is especially useful when you have common functionalities that multiple contracts share.

6. Libraries: Libraries are reusable pieces of code that can be deployed separately from your contract. They can encapsulate complex functionalities or utility functions that your contract may require. By using libraries, you can keep your contract code clean and modular while leveraging functionality already implemented by others.

Remember to follow coding best practices, such as using meaningful variable and function names, writing modular and reusable code, and ensuring proper error handling. Adhere to the coding style guide recommended by the chosen blockchain platform and maintain readability and consistency in your code.

During the code-writing process, refer to the documentation and resources for your chosen blockchain platform and development tools. Additionally, consider seeking guidance from the community or consulting with experienced developers for guidance and code review.

Once you have completed writing the smart contract code, the next step is to compile and deploy the contract onto the blockchain network. Stay tuned for the next section, where we will guide you through the compilation and deployment process.

Step 5: Compile and Deploy the Contract

After writing the code for your smart contract, the next step is to compile and deploy it onto the blockchain network. This process involves converting your contract code into a format that the blockchain can understand, followed by deploying it to make it available for interaction. Here’s an overview of the key steps involved:

1. Compilation: The first step is to compile your smart contract code into bytecode that can be executed on the blockchain. Each blockchain platform has its own compiler or compiler options, which you can use to generate the bytecode. The compilation process validates the syntax and semantics of your code, ensuring it is free of errors.

2. Bytecode Deployment: Once you have successfully compiled your smart contract code, it’s time to deploy it onto the blockchain network. Deploying a contract typically involves sending a transaction, which includes the bytecode and any necessary deployment parameters, to the blockchain. This transaction is processed by the network and results in the creation of a contract instance on the blockchain.

3. Contract Address: When the contract is deployed, it is assigned a unique address on the blockchain network. The contract address serves as the identifier for your contract and is used to interact with it. Make sure to record the contract address, as it will be needed to access and interact with the deployed contract later on.

4. Gas and Transaction Fee: Some blockchain platforms, such as Ethereum, require transactions to consume a certain amount of gas. Gas is a unit that measures the amount of computational effort required to execute a transaction. Gas costs are associated with each operation performed in your contract. To deploy a contract, you need to specify an appropriate gas limit and provide enough Ether (or the respective cryptocurrency) to cover the transaction fee.

5. Confirmation and Block Mining: After sending the deployment transaction, it needs to be confirmed and included in a block on the blockchain. Confirmation time can vary depending on network congestion and the consensus mechanism used by the blockchain. Once confirmed, your contract is deployed and ready for interaction.

6. Contract Upgradability: It’s worth considering contract upgradability during the deployment phase. Some blockchain platforms provide mechanisms to upgrade smart contracts without disrupting the existing contract state or losing data. These upgradeable contract patterns enable you to make improvements or fix bugs in your contract logic while preserving its functionality and data.

Ensure that you carefully follow the deployment instructions specific to the blockchain platform and development tools you are using. Pay attention to transaction status and monitor the blockchain network to confirm the successful deployment of your contract.

Once the smart contract is deployed, you can start interacting with it by calling its functions, subscribing to events, and retrieving contract data. Stay tuned for the next step, where we will guide you through the process of interacting with your deployed smart contract.

Step 6: Interact with the Smart Contract

After successfully deploying your smart contract onto the blockchain network, the next step is to interact with it. Interacting with a smart contract allows you to perform actions, retrieve data, and trigger events within the contract. Here’s an overview of the key aspects involved in this step:

1. Function Calls: Smart contracts expose functions that you can call to perform specific actions or retrieve data. You can initiate function calls to execute tasks defined in the contract, such as transferring assets, updating contract state, or executing specific operations. To call a function, you need to specify the function name and provide any required parameters.

2. Transaction Execution: Interacting with a smart contract typically involves sending transactions to the blockchain network. Transactions are composed of a function call, any necessary input data, the address of the contract, and the transaction sender’s digital signature. These transactions are added to the blockchain, ensuring that the contract state is updated accordingly.

3. Block Confirmation: After sending a transaction to interact with the smart contract, it needs to be confirmed and included in a block on the blockchain. Confirmation time may vary depending on network congestion and the consensus mechanism employed by the blockchain. Once a transaction is included in a block, the changes made by the transaction will reflect in the contract state.

4. Event Listening: Smart contracts can emit events that indicate specific occurrences or state changes. You can listen for these events and react accordingly. By subscribing to events emitted by the contract, you can receive real-time notifications about contract activities and take appropriate actions based on the event data.

5. Contract State Retrieval: Smart contracts usually maintain a state, which can include variables, data structures, and contract-specific information. You can retrieve the contract state by calling specific functions that provide access to the desired data. This allows you to retrieve information stored and managed by the contract on the blockchain.

6. Gas and Transaction Costs: Interacting with a smart contract often incurs gas costs, similar to the deployment phase. Each function call or transaction execution requires a certain amount of gas that covers the computational effort expended by the network. Ensure that you specify a sufficient gas limit and have the necessary cryptocurrency balance to cover the transaction fees.

When interacting with a smart contract, it’s vital to carefully craft your function calls, handle transaction statuses, and properly interpret the data returned by the contract. Additionally, consider implementing error handling and appropriate security measures to protect your interactions and ensure the integrity of the contract execution.

Using development tools and libraries provided by the blockchain platform can ease the process of interacting with smart contracts. These tools often offer API documentation, code examples, and resources to guide you in leveraging the functionalities and capabilities provided by the platform.

By effectively interacting with your smart contract, you can perform actions, retrieve data, and respond to events, unlocking the full potential of your decentralized application or solution.

Congratulations on reaching this milestone! In the final section, we will discuss some best practices for creating smart contracts to ensure robustness, security, and efficiency.

Best Practices for Creating Smart Contracts

Creating robust, secure, and efficient smart contracts is of paramount importance to ensure the success and integrity of your blockchain application. Here are some best practices to consider when developing smart contracts:

1. Thoroughly Understand Requirements: Before writing code, ensure you have a clear understanding of the requirements and objectives of the smart contract. Analyze potential edge cases and consider how the contract will handle them. A solid understanding of the requirements will help you design a contract that meets the intended functionality.

2. Follow Secure Development Standards: Adhere to secure coding practices and standards to minimize the risk of vulnerabilities. Be aware of common security pitfalls, such as integer overflow or reentrancy attacks, and take necessary precautions to mitigate them.

3. Implement Access Control: Clearly define roles and permissions within your smart contract to regulate access and actions. Implement access control mechanisms to ensure that only authorized individuals or entities can execute certain functions or modify specific data within the contract.

4. Use Safe Math Libraries: When dealing with numeric operations, consider using safe math libraries provided by the blockchain platform or third-party libraries to prevent vulnerabilities related to integer overflow and underflow.

5. Avoid Excessive Complexity: Strive to keep your smart contract code simple and readable. Complex logic can introduce more potential issues and make your contract harder to understand and maintain. Break down complex functions and logic into smaller, reusable components.

6. Test Rigorously: Thoroughly test your smart contract code to identify and rectify any bugs or vulnerabilities. Write comprehensive unit tests and integration tests to ensure the correctness and functionality of your contract. Consider using testing frameworks and tools specific to the blockchain platform you are using.

7. Plan for Contract Upgradability: Consider the possibility of needing to upgrade your smart contract in the future. Implement upgradability patterns that allow you to make changes or improvements to the contract logic without disrupting the existing contract’s state or requiring users to migrate to a new contract entirely.

8. Document Extensively: Document your smart contract code thoroughly, including the purpose of each function, the expected behavior, input parameters, and return values. Good documentation allows other developers to understand and interact with your contract more easily.

9. Consider Gas Efficiency: Optimize your smart contract to ensure it uses gas efficiently. Reduce unnecessary computational processes, avoid excessive storage operations, and minimize unnecessary on-chain interactions to reduce transaction costs and improve scalability.

10. Stay Updated: Stay informed about the latest security practices, platform updates, and best practices for smart contract development. Follow relevant coding standards and guidelines provided by the blockchain platform and regularly update dependencies to address security vulnerabilities.

By following these best practices, you can create smart contracts that are resilient, secure, and performant. Regularly review and audit your smart contract code, seek feedback from experts, and stay engaged with the blockchain community to learn from others and improve your skills.

Remember, creating smart contracts is an ongoing process. Keep refining and enhancing your contracts based on feedback, real-world usage, and evolving industry practices.

With these best practices in mind, you are well-equipped to develop reliable and efficient smart contracts that provide value in the world of blockchain technology.

Conclusion

Congratulations on completing this journey to learn how to create blockchain smart contracts! Throughout this guide, we covered essential steps and best practices for creating robust and secure smart contracts.

We began by understanding the concept of blockchain smart contracts, which are self-executing agreements written in code and executed on a blockchain network. We explored the numerous benefits they offer, including increased efficiency, cost savings, enhanced security, trust and transparency, accuracy, immutable record-keeping, global accessibility, improved efficiency in complex processes, and environmental impact.

Next, we delved into the technical aspects of smart contracts, understanding the different components that make up a smart contract, such as agreement, conditions, actions, variables, functions, events, and wallets. By defining the contract logic and selecting the appropriate blockchain platform, you laid the foundation for successful smart contract development.

After setting up the required tools and writing the smart contract code, you learned how to compile and deploy the contract onto the blockchain network. The ability to interact with the contract through function calls, transactions, and event listening brought your contract to life.

Finally, we discussed crucial best practices for creating smart contracts, emphasizing the importance of understanding requirements, following secure development standards, implementing access control, and thorough testing. We also highlighted the significance of contract upgradability, extensive documentation, gas efficiency, and staying updated with the latest practices and updates.

Remember, smart contract development is a continuous learning process. As the blockchain landscape evolves, it is crucial to stay updated with technological advancements, security practices, and community developments.

By applying the knowledge and best practices acquired in this guide, you can create smart contracts that bring transparency, efficiency, and trust to a wide range of industries. So, go ahead, explore, and unleash the full potential of blockchain smart contracts!