Introduction

Blockchain technology has emerged as one of the most transformative and disruptive innovations of the digital age. Originally developed to support cryptocurrencies like Bitcoin, blockchain has rapidly expanded its reach and potential applications across various industries. This decentralized and transparent technology has the potential to revolutionize not only how financial transactions are conducted but also how information and assets are exchanged, managed, and verified.

At its core, blockchain is a distributed ledger system that securely records and verifies transactions across multiple computers, eliminating the need for intermediaries and central authorities. Each transaction, or block, is encrypted and chained to the previous block, forming a chronological and immutable record. This innovative technology offers numerous benefits, including increased transparency, enhanced security, improved efficiency, and reduced costs.

As blockchain continues to evolve, its impact on various sectors is becoming increasingly evident. Financial services, including banking, payments, and remittances, are being profoundly disrupted by blockchain technology. By leveraging blockchain, financial institutions can streamline processes, reduce fraud, enhance security, and enable faster and more cost-effective cross-border transactions.

In addition to finance, supply chain management is another area where blockchain has the potential to revolutionize operations. By providing a transparent and immutable record of the entire supply chain, including the origins, intermediaries, and movement of goods, blockchain can enhance trust, eliminate counterfeit products, and enable real-time tracking and authentication.

The healthcare industry, notorious for its complex data management systems and privacy concerns, can greatly benefit from blockchain technology. By securely storing and sharing patient records, ensuring data integrity, and enabling secure access, blockchain can improve interoperability, streamline processes, and enhance patient outcomes.

Moreover, blockchain has the potential to transform the voting system, guaranteeing accuracy, transparency, and security. By leveraging blockchain’s decentralized nature, it becomes nearly impossible for tampering, ensuring the integrity of the democratic process.

Additionally, blockchain has the potential to revolutionize intellectual property management. By providing a secure and transparent platform for artists, designers, and creators, blockchain can protect and enforce ownership rights, ensuring fair compensation and eliminating copyright infringement.

Last but not least, blockchain presents significant opportunities for enhancing cybersecurity. By decentralizing data storage and providing cryptographic protection, blockchain can mitigate the risk of data breaches, identity theft, and other cyber threats.

While blockchain offers immense potential, it also faces certain challenges and limitations. Scalability, interoperability, regulatory hurdles, and energy consumption are among the key considerations that need to be addressed for widespread adoption and integration. Nonetheless, the future of blockchain looks promising, with a growing number of industries exploring its transformative capabilities.

What is Blockchain?

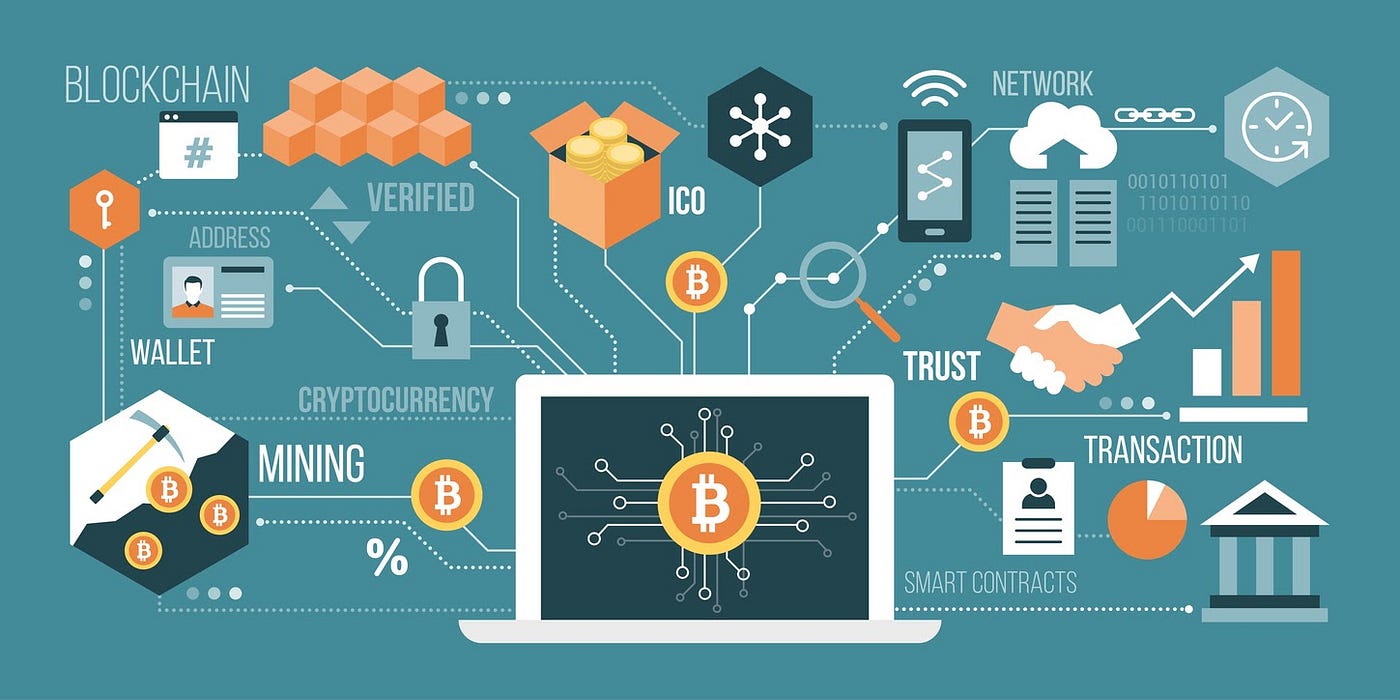

Blockchain is a decentralized and distributed digital ledger technology that securely and transparently records and verifies transactions across multiple computers. It was initially introduced as the underlying technology for Bitcoin, the first and most well-known cryptocurrency. However, blockchain has now evolved into a powerful tool with applications beyond cryptocurrency, revolutionizing various industries.

At its core, a blockchain is a chain of blocks, where each block contains a list of transactions. Each transaction is verified by a network of computers, called nodes, before being added to the blockchain. Once a new block is added to the chain, it becomes part of a permanent and immutable record that cannot be altered or tampered with. This decentralized nature of the blockchain eliminates the need for intermediaries and centralized control, making it highly transparent and trustworthy.

The key features that distinguish blockchain technology are security, transparency, and decentralization. Blockchain achieves security through cryptography, ensuring that transactions are secure and cannot be altered. Transparency is achieved by allowing all participants in the network to have access to the same information, eliminating the need for trust in a single authority. Decentralization ensures that there is no single point of failure and no central authority controlling the system.

Blockchain operates on a peer-to-peer network, where each node maintains a copy of the entire blockchain. This distributed ledger system ensures that no single party can control or manipulate the data. Transactions on the blockchain are verified using consensus mechanisms, such as proof-of-work or proof-of-stake, where participants in the network reach a consensus on the validity of the transaction before it is added to the blockchain.

The applications of blockchain technology are vast and diverse. Beyond cryptocurrencies, blockchain has the potential to transform industries such as finance, supply chain management, healthcare, voting systems, intellectual property, and cybersecurity. Its ability to provide secure, transparent, and tamper-proof records has the potential to revolutionize how transactions, data, and assets are managed and exchanged.

With its decentralized nature and robust security features, blockchain technology holds tremendous promise for various sectors. As organizations recognize the potential of blockchain, they are exploring ways to integrate it into their operations to enhance efficiency, security, and trust in their processes.

How Does Blockchain Work?

Blockchain technology operates on a set of principles and protocols that allow it to securely and transparently record and verify transactions. Understanding how blockchain works requires knowledge of key components, such as blocks, nodes, cryptography, and consensus mechanisms.

A blockchain consists of a chain of blocks, with each block containing a list of transactions. Each transaction contains information about the sender, receiver, and the amount transferred. These blocks are linked together in a chronological order, forming an unalterable and transparent record of all transactions.

Nodes in the blockchain network maintain a copy of the entire blockchain and participate in the verification process. Each node verifies the validity of transactions before adding them to the blockchain. This verification process ensures that only legitimate transactions are recorded, preventing fraud and tampering.

Cryptography plays a vital role in securing the transactions on the blockchain. Each transaction is digitally signed using cryptographic keys, ensuring that only the authorized parties can initiate and validate the transaction. Additionally, the hash function is used to generate a unique identifier, called a hash, for each block. This hash is calculated based on the data within the block and serves as a digital fingerprint, allowing quick verification of the block’s integrity.

Consensus mechanisms are employed to ensure agreement among the nodes in the blockchain network. These mechanisms determine how nodes reach a consensus on the validity of transactions and the order in which the blocks are added to the chain. The two most common consensus mechanisms are proof-of-work (PoW) and proof-of-stake (PoS).

In a proof-of-work system, nodes compete to solve a complex mathematical puzzle. The first node to solve the puzzle is rewarded and gets the right to add the next block to the blockchain. PoW ensures that adding new blocks is computationally expensive, making it difficult to tamper with the existing chain. However, it also requires significant computational power and energy consumption.

In a proof-of-stake system, the right to add a new block is determined by the node’s stake or ownership of a certain amount of cryptocurrency. This mechanism eliminates the need for intensive computational work, reducing energy consumption. However, it may introduce centralization risks if a small group of nodes possess a majority of the cryptocurrency.

Once a block is added to the blockchain, it becomes permanent and cannot be altered without consensus from the majority of nodes. This immutability ensures the integrity and trustworthiness of the blockchain. Additionally, the distributed nature of the blockchain ensures that there is no single point of failure, making it highly resistant to hacking or manipulation.

Overall, the combination of cryptography, consensus mechanisms, and distributed ledger technology enables blockchain to provide secure, transparent, and tamper-proof records of transactions. As a result, blockchain has the potential to revolutionize various industries by enhancing security, transparency, and efficiency in their operations.

Benefits of Blockchain Technology

Blockchain technology offers a wide range of benefits with the potential to transform various industries. From increased transparency and security to improved efficiency and reduced costs, the advantages of blockchain are considerable.

One of the key benefits of blockchain is its transparency. The distributed ledger nature of blockchain ensures that all participants in the network have access to the same information, eliminating the need for trust in a single authority. This transparency not only enhances accountability but also enables real-time auditing, reducing the risk of fraud and corruption.

Another significant advantage of blockchain is its enhanced security. Transactions on the blockchain are encrypted and linked to the previous block, forming a chain that is extremely difficult to tamper with. Additionally, the use of cryptographic keys ensures that only authorized parties can initiate and validate transactions. This robust security feature makes blockchain highly resistant to hacking and manipulation.

Furthermore, blockchain technology brings about increased efficiency in various processes. By eliminating the need for intermediaries and manual record-keeping, blockchain streamlines transactions and reduces administrative burdens. Smart contracts, which are self-executing contracts with terms written directly into the code, automate processes further, enabling faster and more efficient transactions.

Cost reduction is another significant advantage of blockchain. Traditional transactions often involve multiple intermediaries, resulting in additional fees and delays. With blockchain, these intermediaries are eliminated, reducing costs and speeding up transactions. Additionally, the automation and efficiency brought about by smart contracts reduce the need for manual verification and paperwork, further reducing costs.

Blockchain technology also offers increased traceability and accountability. With its immutable and transparent record, blockchain enables the tracking and authentication of assets throughout their lifecycle. This is particularly valuable in supply chain management, where blockchain can provide real-time tracking of goods, ensuring their authenticity and origin.

Additionally, blockchain has the potential to enhance financial inclusion by providing access to financial services for the unbanked and underbanked populations. With blockchain, individuals can securely store and transfer assets without the need for traditional banking systems. This opens up opportunities for financial inclusion and economic empowerment.

Moreover, blockchain technology enables greater control over personal data. Traditional systems often store personal data in centralized databases, making it vulnerable to data breaches and misuse. With blockchain, individuals have greater control over their data and can grant data access on a need-to-know basis, ensuring privacy and security.

Overall, blockchain technology offers a host of benefits, including increased transparency, enhanced security, improved efficiency, reduced costs, traceability, and financial inclusion. As industries continue to explore its potential, blockchain has the potential to revolutionize how transactions and data are managed across various sectors.

Blockchain and Financial Services

The financial services industry is one of the sectors poised to be profoundly disrupted by blockchain technology. Blockchain offers numerous advantages that can transform the way financial transactions are conducted, enhancing transparency, security, efficiency, and cost-effectiveness.

One of the key applications of blockchain in financial services is in the realm of payments and remittances. Traditional cross-border transactions are often slow, expensive, and prone to errors. Blockchain technology, on the other hand, enables near-instantaneous, secure, and low-cost transfers that can bypass the need for intermediaries, such as banks or payment processors. Additionally, the transparency provided by blockchain can enhance the visibility and traceability of funds, reducing the risk of fraud and money laundering.

Smart contracts, which are self-executing contracts with the terms written directly into the code, eliminate the need for intermediaries in financial agreements. With smart contracts, parties can automate the execution of complex agreements, such as loans and insurance policies, without relying on traditional intermediaries. This reduces costs and removes the need for trust in a third party, as the terms of the contract are enforced by the blockchain’s consensus mechanism.

The decentralized nature of blockchain also has the potential to democratize access to financial services. With blockchain-based systems, individuals who are unbanked or underbanked can securely store and transfer assets without the need for traditional financial institutions. This opens up opportunities for financial inclusion, allowing individuals to participate in the global economy and access essential services, such as loans and insurance, that were previously out of reach.

Furthermore, blockchain technology can revolutionize the process of fundraising through crowdfunding and Initial Coin Offerings (ICOs). By leveraging blockchain, companies can issue digital tokens that represent ownership or utility in a project. These tokens can be bought, sold, and traded globally, enabling a more efficient and accessible means of raising capital. Investors can directly participate in projects, eliminating the need for intermediaries and reducing barriers to entry.

Blockchain also offers opportunities for greater transparency and accountability in the management of assets. Through tokenization, physical assets such as real estate or art can be represented on the blockchain, enabling fractional ownership and efficient transferability. This provides increased liquidity and reduces the barriers to investing in traditionally illiquid assets.

While there are significant opportunities for blockchain in financial services, there are also challenges that need to be addressed. Scalability, regulatory frameworks, and interoperability with existing systems are among the key considerations for widespread implementation. Nonetheless, as the technology continues to mature, blockchain has the potential to revolutionize financial services, making transactions more secure, transparent, efficient, and inclusive.

Blockchain and Supply Chain Management

Supply chain management is a complex process involving the movement, storage, and tracking of goods from their point of origin to the end consumer. Blockchain technology has the potential to revolutionize supply chain management by providing enhanced transparency, traceability, and trust throughout the entire supply chain.

One of the key advantages of blockchain in supply chain management is the ability to create a transparent and immutable record of each step in the supply chain. Traditionally, supply chain data is siloed and controlled by multiple parties, making it difficult to track and verify the movement of goods. With blockchain, each transaction and movement is recorded on the distributed ledger, creating a single, transparent, and auditable source of truth.

Blockchain enables real-time tracking and authentication, allowing stakeholders to quickly and accurately verify the origin, location, and authenticity of goods. This level of transparency improves trust among participants in the supply chain, reduces the risk of counterfeit or tampered products, and ensures compliance with regulations and standards.

The use of blockchain technology also facilitates greater collaboration and coordination among supply chain partners. Different stakeholders, such as manufacturers, suppliers, distributors, and retailers, can securely access and share relevant data on the blockchain, eliminating the need for intermediaries and reducing paperwork and administrative burdens.

Additionally, blockchain can streamline the process of managing inventory and reducing inefficiencies. Through smart contracts and automated processes, blockchain can enable real-time inventory tracking, automated reordering, and efficient supply chain management. This helps to reduce stockouts, optimize inventory levels, and improve overall efficiency in the supply chain.

Blockchain technology can also play a crucial role in ensuring sustainability and ethical sourcing in supply chains. With blockchain, companies can transparently track the movement of raw materials and validate their origin, ensuring compliance with environmental and labor standards. This can help foster responsible sourcing practices and provide assurances to consumers about the ethical nature of the products they purchase.

Furthermore, blockchain can enhance supply chain financing and trade finance by facilitating secure and transparent transactions. Smart contracts can automate the execution of payment terms, reducing the risk of disputes and delays. This, in turn, can unlock working capital for suppliers and provide greater visibility and security to financial institutions.

While blockchain holds immense potential for supply chain management, there are challenges that need to be considered. Interoperability between different blockchain systems, integration with existing legacy systems, and scalability are among the key considerations that need to be addressed for widespread adoption. Nonetheless, blockchain has the potential to transform supply chain management by improving transparency, traceability, collaboration, and efficiency across industries.

Blockchain and Healthcare

The healthcare industry faces numerous challenges in managing and securing patient data, ensuring interoperability between different systems, and safeguarding privacy. Blockchain technology has the potential to address these challenges and revolutionize healthcare by providing secure, transparent, and interoperable solutions.

One of the key applications of blockchain in healthcare is the secure and efficient management of electronic health records (EHRs). With blockchain, patient records can be securely stored and shared across different healthcare providers, ensuring data integrity, portability, and accessibility. This enables seamless information exchange, reduces duplication of tests, and improves patient care coordination.

The decentralized nature of blockchain ensures that patient data is not stored in a single location, making it less vulnerable to data breaches and unauthorized access. Cryptographic algorithms and keys provide an additional layer of security, protecting patient data from unauthorized modifications or tampering.

Moreover, blockchain can enhance patient privacy by providing individuals with greater control over their own health data. With blockchain, patients can grant and revoke access to their health records on a need-to-know basis, ensuring privacy and consent. This empowers patients to have more control over their personal health information.

Medical research can also benefit from blockchain technology. With blockchain, researchers can securely and efficiently access and share anonymized patient data for research purposes. This streamlined access to data can facilitate breakthroughs in medical research and accelerate the development of innovative treatments and therapies.

Another area where blockchain can revolutionize healthcare is in the tracking and authentication of pharmaceuticals and medical devices. Counterfeit drugs pose a significant risk to patient safety and public health. With blockchain, the entire supply chain of drugs can be tracked and verified, preventing counterfeit products from entering the market. This improves patient safety and reduces the risk of fraud in the pharmaceutical industry.

Furthermore, blockchain enables greater transparency and trust in clinical trials and healthcare claims processing. By recording the entire history of clinical trials on the blockchain, researchers and regulators can ensure the integrity of the data and provide greater transparency to the public. Similarly, in claims processing, blockchain-based systems can automate processes, reduce administrative burdens, and prevent fraudulent claims.

While there are significant opportunities for blockchain in healthcare, challenges such as regulatory frameworks, data standardization, and interoperability need to be addressed for widespread adoption. Additionally, concerns about the scalability and performance of blockchain in handling large-scale healthcare data should be considered.

Nevertheless, blockchain technology holds tremendous promise for transforming healthcare by enhancing data security, interoperability, patient privacy, medical research, and supply chain management. As the technology continues to evolve and mature, blockchain has the potential to revolutionize how healthcare data is managed, leading to improved patient care outcomes.

Blockchain and Voting

Secure and transparent elections are the cornerstone of democratic societies. Blockchain technology offers the potential to revolutionize the voting process by providing greater transparency, security, trust, and accessibility.

One of the key advantages of implementing blockchain in voting systems is the enhanced security it provides. Traditional voting systems are vulnerable to various threats, including tampering, hacking, and voter fraud. With blockchain, each vote is securely recorded on a decentralized and immutable ledger, making it nearly impossible to alter or manipulate the results. This ensures the integrity of the voting process and builds trust in the outcome.

Transparency is another crucial aspect of blockchain-based voting. Blockchain enables all participants to have access to the same information, eliminating the need to rely on a single authority for vote counting and verification. Each voter can independently verify their vote, ensuring that it is accurately recorded and counted. This level of transparency enhances trust and ensures the legitimacy of the election.

The decentralized nature of blockchain also provides increased resistance to censorship and manipulation. Since there is no central authority controlling the blockchain, attempts to manipulate the voting process become more challenging. This ensures that every vote is treated equally and gives individuals the confidence that their voice will be heard.

Moreover, blockchain can enhance the accessibility and inclusivity of voting. With traditional voting methods, individuals who are unable to physically go to polling stations face difficulties in casting their votes. Blockchain-based voting systems can enable remote and online voting, allowing individuals to participate in the democratic process from anywhere. This can empower individuals who are geographically distant, physically disabled, or serving abroad to exercise their right to vote.

Additionally, blockchain can facilitate faster and more efficient vote counting. Since votes are recorded on a digital ledger in real-time, the manual process of counting paper ballots is eliminated. This reduces the time it takes to announce election results, enabling more rapid decision-making processes.

While blockchain-based voting systems offer significant advantages, challenges need to be addressed for widespread adoption. These challenges include ensuring voter privacy, protecting against identity theft, and addressing potential vulnerabilities in the technical infrastructure. Additionally, concerns about digital literacy and access to technology need to be considered to ensure that all individuals can participate in blockchain-based voting.

Despite these challenges, blockchain offers a promising solution to address the shortcomings of traditional voting systems. By leveraging the technology’s transparency, security, and decentralization, blockchain has the potential to revolutionize the voting process, ensuring fair, transparent, and inclusive elections.

Blockchain and Intellectual Property

Intellectual property (IP) plays a vital role in today’s digital economy, but its protection and enforcement can be challenging. Blockchain technology offers a promising solution to address the issues surrounding IP management by providing enhanced security, transparency, and enforcement.

One of the key advantages of using blockchain for IP management is the ability to establish proof of ownership and authenticity. With blockchain, creators can securely register their works, including copyrights, patents, trademarks, and digital assets. Each registration is recorded on the blockchain, creating an immutable, timestamped record that serves as undeniable proof of ownership and creation.

By leveraging blockchain, creators can protect their IP rights against infringement and unauthorized use. Smart contracts can be employed to automate licensing agreements, ensuring that royalties are properly distributed and that only authorized parties can access and use the content. Blockchain’s transparency and decentralized nature provide a secure platform for transactions, reducing the risk of fraud and copyright disputes.

Blockchain’s ability to establish an immutable record of IP ownership can also streamline the IP registration and enforcement process. Currently, IP registration and enforcement rely on centralized authorities, which can be slow and costly. With blockchain, the registration process can be streamlined, eliminating administrative burdens and reducing costs. Additionally, the transparent and tamper-proof nature of blockchain records can simplify IP enforcement, enabling prompt and efficient resolution of disputes.

Furthermore, blockchain can address the issue of plagiarism and copyright infringement, which are rampant in the digital age. By creating a transparent and auditable record of each creation, blockchain can help identify and track instances of unauthorized copying or use. This makes it easier for creators to enforce their rights and protect their works from infringement.

The use of blockchain also enables the creation of decentralized and transparent marketplaces for IP assets. Creators can tokenize their IP assets on the blockchain and trade them directly with interested parties. This decentralized marketplace eliminates the need for intermediaries and reduces transaction costs, enabling a more efficient and accessible IP economy.

While blockchain shows great potential for IP management, there are challenges that need to be addressed. These challenges include addressing legal frameworks, ensuring privacy of sensitive IP information, and promoting the adoption and use of blockchain in the IP industry.

Despite these challenges, blockchain offers an exciting opportunity to transform how intellectual property is managed, protected, and monetized. With its enhanced security, transparency, and enforcement capabilities, blockchain has the potential to revolutionize the IP ecosystem, empowering creators and safeguarding their rights in the digital age.

Blockchain and Cybersecurity

Cybersecurity is a growing concern in today’s digital landscape, with organizations and individuals facing increasing threats from data breaches, hacking, and identity theft. Blockchain technology offers a promising solution to enhance cybersecurity by providing improved data protection, identity management, and secure transactions.

One of the primary advantages of blockchain in cybersecurity is its robust data protection capabilities. Traditional databases are vulnerable to attacks, as they often store information in a centralized location, making it an attractive target for hackers. In contrast, blockchain distributes data across multiple nodes, making it much more difficult for hackers to compromise the data. Additionally, blockchain uses cryptographic algorithms to secure transactions, ensuring that sensitive information remains tamper-proof.

Blockchain technology also enables secure identity management. Identity theft is a prevalent issue, with personal information being stolen and misused. By leveraging blockchain, individuals can have more control over their personal data. Blockchain’s decentralized nature allows individuals to securely manage and control their digital identities, granting access only to trusted parties on a need-to-know basis. This enhances security and reduces the risk of identity theft.

In addition to data protection and identity management, blockchain technology can facilitate secure and transparent transactions. When making online transactions, individuals and organizations face the risk of fraudulent activities. Blockchain’s decentralized and transparent nature ensures that all transactions are recorded and verified, preventing unauthorized and fraudulent transactions. This can be particularly beneficial in areas such as financial transactions, supply chain management, and digital asset exchanges.

Blockchain can also enhance cybersecurity through the use of smart contracts. Smart contracts are self-executing contracts with predefined terms and conditions stored on the blockchain. They automatically execute actions when predetermined conditions are met, eliminating the need for intermediaries and reducing the risk of human error or manipulation. Smart contracts can be used to enforce security measures, such as multi-factor authentication, access controls, and secure data sharing, improving overall cybersecurity.

However, it is crucial to note that while blockchain can enhance cybersecurity, it is not without its challenges. Key considerations include ensuring the security of private keys, addressing vulnerabilities in smart contracts and blockchain implementations, and ensuring regulatory compliance when dealing with sensitive data.

In summary, blockchain technology offers significant potential in enhancing cybersecurity. By providing robust data protection, secure identity management, and transparent transactions, blockchain can help address the ever-growing cybersecurity threats faced by organizations and individuals. As the technology continues to evolve, its widespread adoption has the potential to transform how we secure and protect our digital assets.

Challenges and Limitations of Blockchain

While blockchain technology holds immense potential in transforming various industries, it is important to acknowledge the challenges and limitations that come with its implementation and widespread adoption. These challenges include scalability, interoperability, regulatory hurdles, energy consumption, and technological limitations.

Scalability is one of the primary challenges faced by blockchain technology. As the number of transactions on a blockchain network grows, the processing time and resource requirements increase significantly. This can lead to slower transaction times and higher costs, hindering the widespread adoption of blockchain in high-volume industries such as finance and supply chain management. Efforts are underway to address scalability issues through scaling solutions like sharding, off-chain solutions, and layer two protocols.

Interoperability is another challenge associated with blockchain technology. As multiple blockchain platforms emerge, each with its own protocols and consensus mechanisms, the interoperability between these different platforms becomes complex. The lack of seamless communication and interoperability limits the ability to transfer data and assets across different blockchain networks. Efforts are being made to develop standardized protocols and frameworks to facilitate interoperability between different blockchain platforms.

Regulatory hurdles present another significant challenge for blockchain adoption. Due to the decentralized nature of blockchain, it can be challenging to fit within existing regulatory frameworks governing financial transactions, data privacy, and intellectual property rights. Clarifying and adapting regulatory frameworks to accommodate blockchain technology while ensuring consumer protection and regulatory compliance is an ongoing challenge that requires collaboration between governments, industry, and regulatory bodies.

Energy consumption is another concern associated with blockchain technology, particularly in the case of proof-of-work consensus mechanisms, such as those used in Bitcoin. The computational requirements of mining and validating transactions on a blockchain can result in significant energy consumption. Efforts are being made to develop more energy-efficient consensus mechanisms, such as proof-of-stake, and to explore sustainable energy sources to power blockchain networks.

Technological limitations also pose challenges to blockchain adoption. Although blockchain technology has made significant advancements, it still faces limitations in terms of scalability, privacy, and the ability to handle large-scale data transactions. Additionally, blockchain networks are vulnerable to attacks, such as 51% attacks, where a single entity or group gains control over the majority of network resources, potentially compromising the network’s security and integrity.

While these challenges and limitations exist, ongoing research, development, and collaboration within the blockchain community are focused on finding solutions and advancing the technology. Efforts are being made to improve scalability, develop interoperability standards, address regulatory concerns, enhance energy efficiency, and strengthen security measures. As blockchain technology continues to mature, these challenges can be overcome, unlocking the full potential of blockchain in revolutionizing various industries.

Conclusion

Blockchain technology has emerged as a transformative force, revolutionizing industries such as finance, supply chain management, healthcare, voting systems, intellectual property, and cybersecurity. Its decentralized and transparent nature enables secure and efficient transactions, enhanced data protection, improved trust, and increased collaboration.

By leveraging blockchain, financial services can be streamlined, reducing costs, eliminating intermediaries, and facilitating faster cross-border transactions. Supply chain management can benefit from blockchain’s transparency, traceability, and real-time tracking, improving efficiency, trust, and authenticity. In healthcare, blockchain can enhance the secure management and sharing of patient records, streamline processes, and improve interoperability. Blockchain technology also presents opportunities for secure and transparent voting systems, protecting the integrity of elections and enhancing citizen participation.

Intellectual property management can be transformed with blockchain, establishing proof of ownership, preventing infringement, and facilitating secure transactions. Furthermore, blockchain’s robust security features and transparency offer promising solutions in bolstering cybersecurity, protecting data, and ensuring secure transactions and identity management.

However, challenges such as scalability, interoperability, regulatory frameworks, energy consumption, and technological limitations must be addressed for the widespread adoption of blockchain. Efforts are underway to tackle these challenges through innovations in scaling solutions, interoperability protocols, regulatory frameworks, energy-efficient consensus mechanisms, and advancements in security measures.

As blockchain technology continues to evolve and mature, its potential in transforming industries becomes increasingly evident. Collaboration between governments, industries, and regulatory bodies is crucial to create a supportive environment that fosters the integration and adoption of blockchain solutions. With continued research, development, and collaboration, blockchain has the power to revolutionize industries, improve efficiency, transparency, and trust, and empower individuals and organizations in the digital age.